Answered step by step

Verified Expert Solution

Question

1 Approved Answer

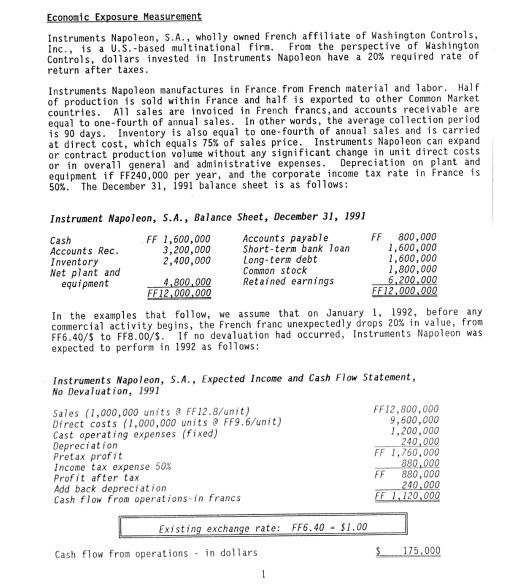

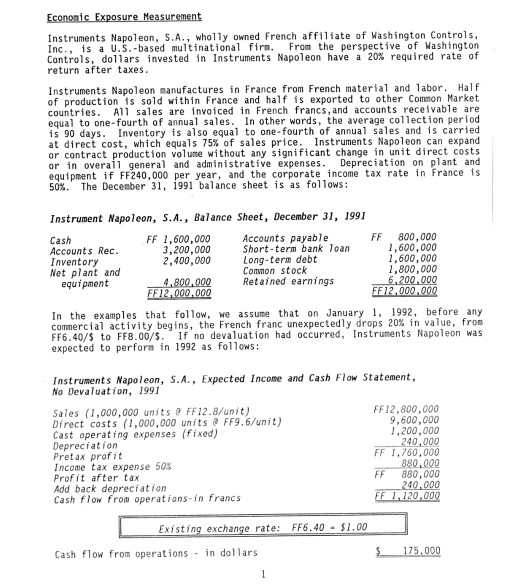

Economic Exposure Measurement Instruments Napoleon, S.A., wholly owned French affiliate of Washington Controls, Inc. is a U.S.-based multinational firm. From the perspective of Washington Controls,

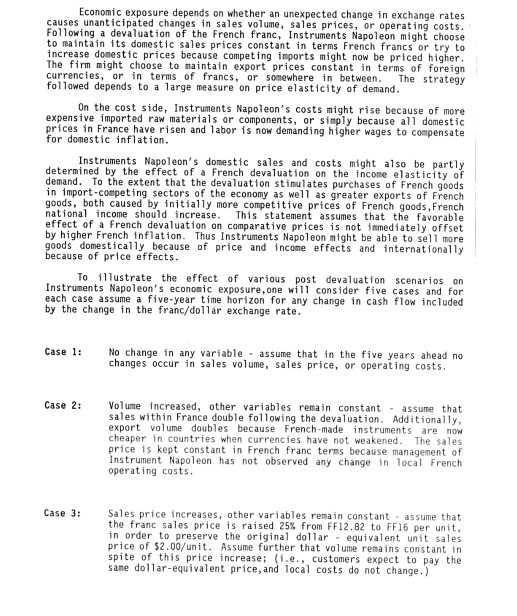

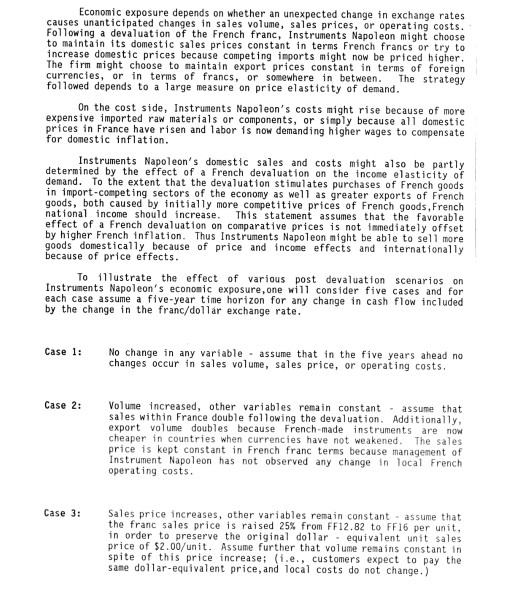

Economic Exposure Measurement Instruments Napoleon, S.A., wholly owned French affiliate of Washington Controls, Inc. is a U.S.-based multinational firm. From the perspective of Washington Controls, dollars invested in Instruments Napoleon have a 20% required rate of return after taxes. Instruments Napoleon manufactures in France from French material and labor. Half of production is sold within France and half is exported to other Common Market countries. All sales are invoiced in French francs, and accounts receivable are equal to one-fourth of annual sales. In other words, the average collection period is 90 days. Inventory is also equal to one-fourth of annual sales and is carried at direct cost, which equals 75% of sales price. Instruments Napoleon can expand or contract production volume without any significant change in unit direct costs or in overall general and administrative expenses. Depreciation on plant and equipment if FF240,000 per year, and the corporate income tax rate in France is 50%. The December 31, 1991 balance sheet is as follows: Instrument Napoleon, S.A., Balance Sheet, December 31, 1991 Cash FF 1,600,000 Accounts payable FF 800,000 Accounts Rec. 3,200,000 Short-term bank loan 1,600,000 Inventory 2,400,000 Long-term debt 1,600,000 Net plant and Common stock 1,800,000 equipment 4.800,000 Retained earnings 6.200.000 FF 12.000.000 FF 12,000,000 In the examples that follow, we assume that on January 1, 1992, before any commercial activity begins, the French franc unexpectedly drops 20% in value, from FF6.40/$ to FF8.00/$. If no devaluation had occurred, Instruments Napoleon was expected to perform in 1992 as follows: Instruments Napoleon, S.A., Expected Income and Cash Flow Statement, No Devaluation, 1991 Sales (1,000,000 units FF12.8/unit) FF12,800,000 Direct costs (1,000,000 units FF9.6/unit) 9,600,000 Cast operating expenses (fixed) 1.200,000 Depreciation 240,000 Pretax profit FF 1,760,000 Income tax expense 50% 880.000 Profit after tax FF 880,000 Add back depreciation 240.000 Cash flow from operations in francs Ef 1,120.000 Existing exchange rate: FF6.40 . 51.00 Cash flow from operations - in dollars 175,000 Economic exposure depends on whether an unexpected change in exchange rates causes unanticipated changes in sales volume, sales prices, or operating costs. Following a devaluation of the French franc, Instruments Napoleon might choose to maintain its domestic sales prices constant in terms French francs or try to increase domestic prices because competing imports might now be priced higher. The firm might choose to maintain export prices constant in terms of foreign currencies, or in terms of francs, or somewhere in between. The strategy followed depends to a large measure on price elasticity of demand. On the cost side, Instruments Napoleon's costs might rise because of more expensive imported raw materials or components, or simply because all domestic prices in France have risen and labor is now demanding higher wages to compensate for domestic inflation. sed by ectors of the aluation su Instruments Napoleon's domestic sales and costs might also be partly determined by the effect of a French devaluation on the income elasticity of demand. To the extent that the devaluation stimulates purchases of French goods in import-competing sectors of the economy as well as greater exports of French goods, both caused by initially more competitive prices of French goods, French national income should increase. This statement assumes that the favorable effect of a French devaluation on comparative prices is not immediately offset by higher French inflation. Thus Instruments Napoleon night be able to sell more goods domestically because of price and income effects and internationally because of price effects. To illustrate the effect of various post devaluation scenarios on Instruments Napoleon's economic exposure, one will consider five cases and for each case assume a five-year time horizon for any change in cash flow included by the change in the franc/dollar exchange rate. Case 1: No change in any variable - assume that in the five years ahead no changes occur in sales volume, sales price, or operating costs. Case 2: Volume increased, other variables remain constant . assume that sales within France double following the devaluation. Additionally. export volume doubles because French-made instruments are now cheaper in countries when currencies have not weakened. The sales price is kept constant in French franc terms because management of Instrument Napoleon has not observed any change in local French operating costs. Case 3: Sales price increases, other variables remain constant - assume that the franc sales price is raised 25% from FF12.82 to FF16 per unit, in order to preserve the original dollar - equivalent unit sales price of $2.00/unit. Assume further that volume remains constant in spite of this price increase; (1.e., customers expect to pay the same dollar-equivalent price, and local costs do not change. ) Economic exposure depends on whether an unexpected change in exchange rates causes unanticipated changes in sales volume, sales prices, or operating costs. Following a devaluation of the French franc, Instruments Napoleon might choose to maintain its domestic sales prices constant in terms French francs or try to increase domestic prices because competing imports might now be priced higher. currencies, or in terms of francs, or somewhere in between. The strategy followed depends to a large measure on price elasticity of demand. On the cost side, Instruments Napoleon's costs might rise because of more expensive imported raw materials or components, or simply because all domestic prices in France have risen and labor is now demanding higher wages to compensate for domestic inflation. sed by ectors of the aluation su Instruments Napoleon's domestic sales and costs might also be partly determined by the effect of a French devaluation on the income elasticity of demand. To the extent that the devaluation stimulates purchases of French goods in import-competing sectors of the economy as well as greater exports of French goods, both caused by initially more competitive prices of French goods, French national income should increase. This statement assumes that the favorable effect of a French devaluation on comparative prices is not immediately offset by higher French inflation. Thus Instruments Napoleon night be able to sell more goods domestically because of price and income effects and internationally because of price effects. To illustrate the effect of various post devaluation scenarios on Instruments Napoleon's economic exposure, one will consider five cases and for each case assume a five-year time horizon for any change in cash flow included by the change in the franc/dollar exchange rate. Case 1: No change in any variable - assume that in the five years ahead no changes occur in sales volume, sales price, or operating costs. Case 2: Volume increased, other variables remain constant . assume that sales within France double following the devaluation. Additionally. export volume doubles because French-made instruments are now cheaper in countries when currencies have not weakened. The sales price is kept constant in French franc terms because management of Instrument Napoleon has not observed any change in local French operating costs. Case 3: Sales price increases, other variables remain constant - assume that the franc sales price is raised 25% from FF12.82 to FF16 per unit, in order to preserve the original dollar - equivalent unit sales price of $2.00/unit. Assume further that volume remains constant in spite of this price increase; (1.e., customers expect to pay the same dollar-equivalent price, and local costs do not change. ) Economic Exposure Measurement Instruments Napoleon, S.A., wholly owned French affiliate of Washington Controls, Inc. is a U.S.-based multinational firm. From the perspective of Washington Controls, dollars invested in Instruments Napoleon have a 20% required rate of return after taxes. Instruments Napoleon manufactures in France from French material and labor. Half of production is sold within France and half is exported to other Common Market countries. All sales are invoiced in French francs, and accounts receivable are equal to one-fourth of annual sales. In other words, the average collection period is 90 days. Inventory is also equal to one-fourth of annual sales and is carried at direct cost, which equals 75% of sales price. Instruments Napoleon can expand or contract production volume without any significant change in unit direct costs or in overall general and administrative expenses. Depreciation on plant and equipment if FF240,000 per year, and the corporate income tax rate in France is 50%. The December 31, 1991 balance sheet is as follows: Instrument Napoleon, S.A., Balance Sheet, December 31, 1991 Cash FF 1,600,000 Accounts payable FF 800,000 Accounts Rec. 3,200,000 Short-term bank loan 1,600,000 Inventory 2,400,000 Long-term debt 1,600,000 Net plant and Common stock 1,800,000 equipment 4.800,000 Retained earnings 6.200.000 FF 12.000.000 FF 12,000,000 In the examples that follow, we assume that on January 1, 1992, before any commercial activity begins, the French franc unexpectedly drops 20% in value, from FF6.40/$ to FF8.00/$. If no devaluation had occurred, Instruments Napoleon was expected to perform in 1992 as follows: Instruments Napoleon, S.A., Expected Income and Cash Flow Statement, No Devaluation, 1991 Sales (1,000,000 units FF12.8/unit) FF12,800,000 Direct costs (1,000,000 units FF9.6/unit) 9,600,000 Cast operating expenses (fixed) 1.200,000 Depreciation 240,000 Pretax profit FF 1,760,000 Income tax expense 50% 880.000 Profit after tax FF 880,000 Add back depreciation 240.000 Cash flow from operations in francs Ef 1,120.000 Existing exchange rate: FF6.40 . 51.00 Cash flow from operations - in dollars 175,000 Economic exposure depends on whether an unexpected change in exchange rates causes unanticipated changes in sales volume, sales prices, or operating costs. Following a devaluation of the French franc, Instruments Napoleon might choose to maintain its domestic sales prices constant in terms French francs or try to increase domestic prices because competing imports might now be priced higher. The firm might choose to maintain export prices constant in terms of foreign currencies, or in terms of francs, or somewhere in between. The strategy followed depends to a large measure on price elasticity of demand. On the cost side, Instruments Napoleon's costs might rise because of more expensive imported raw materials or components, or simply because all domestic prices in France have risen and labor is now demanding higher wages to compensate for domestic inflation. sed by ectors of the aluation su Instruments Napoleon's domestic sales and costs might also be partly determined by the effect of a French devaluation on the income elasticity of demand. To the extent that the devaluation stimulates purchases of French goods in import-competing sectors of the economy as well as greater exports of French goods, both caused by initially more competitive prices of French goods, French national income should increase. This statement assumes that the favorable effect of a French devaluation on comparative prices is not immediately offset by higher French inflation. Thus Instruments Napoleon night be able to sell more goods domestically because of price and income effects and internationally because of price effects. To illustrate the effect of various post devaluation scenarios on Instruments Napoleon's economic exposure, one will consider five cases and for each case assume a five-year time horizon for any change in cash flow included by the change in the franc/dollar exchange rate. Case 1: No change in any variable - assume that in the five years ahead no changes occur in sales volume, sales price, or operating costs. Case 2: Volume increased, other variables remain constant . assume that sales within France double following the devaluation. Additionally. export volume doubles because French-made instruments are now cheaper in countries when currencies have not weakened. The sales price is kept constant in French franc terms because management of Instrument Napoleon has not observed any change in local French operating costs. Case 3: Sales price increases, other variables remain constant - assume that the franc sales price is raised 25% from FF12.82 to FF16 per unit, in order to preserve the original dollar - equivalent unit sales price of $2.00/unit. Assume further that volume remains constant in spite of this price increase; (1.e., customers expect to pay the same dollar-equivalent price, and local costs do not change. ) Economic exposure depends on whether an unexpected change in exchange rates causes unanticipated changes in sales volume, sales prices, or operating costs. Following a devaluation of the French franc, Instruments Napoleon might choose to maintain its domestic sales prices constant in terms French francs or try to increase domestic prices because competing imports might now be priced higher. currencies, or in terms of francs, or somewhere in between. The strategy followed depends to a large measure on price elasticity of demand. On the cost side, Instruments Napoleon's costs might rise because of more expensive imported raw materials or components, or simply because all domestic prices in France have risen and labor is now demanding higher wages to compensate for domestic inflation. sed by ectors of the aluation su Instruments Napoleon's domestic sales and costs might also be partly determined by the effect of a French devaluation on the income elasticity of demand. To the extent that the devaluation stimulates purchases of French goods in import-competing sectors of the economy as well as greater exports of French goods, both caused by initially more competitive prices of French goods, French national income should increase. This statement assumes that the favorable effect of a French devaluation on comparative prices is not immediately offset by higher French inflation. Thus Instruments Napoleon night be able to sell more goods domestically because of price and income effects and internationally because of price effects. To illustrate the effect of various post devaluation scenarios on Instruments Napoleon's economic exposure, one will consider five cases and for each case assume a five-year time horizon for any change in cash flow included by the change in the franc/dollar exchange rate. Case 1: No change in any variable - assume that in the five years ahead no changes occur in sales volume, sales price, or operating costs. Case 2: Volume increased, other variables remain constant . assume that sales within France double following the devaluation. Additionally. export volume doubles because French-made instruments are now cheaper in countries when currencies have not weakened. The sales price is kept constant in French franc terms because management of Instrument Napoleon has not observed any change in local French operating costs. Case 3: Sales price increases, other variables remain constant - assume that the franc sales price is raised 25% from FF12.82 to FF16 per unit, in order to preserve the original dollar - equivalent unit sales price of $2.00/unit. Assume further that volume remains constant in spite of this price increase; (1.e., customers expect to pay the same dollar-equivalent price, and local costs do not change. )

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Ultimate Guide O Futures Rading

Authors: Josh Luberisse

1st Edition

979-8374817393