Answered step by step

Verified Expert Solution

Question

1 Approved Answer

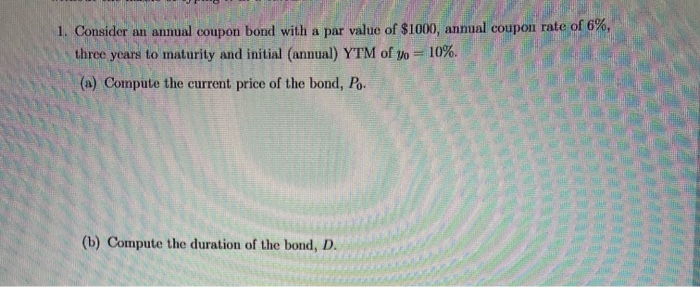

EFGH . . . 1. Consider an annual coupon bond with a par value of $1000, annual coupon rate of 6%, three years to maturity

EFGH

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Dropshipping Road To $10 000 Per Month Of Passive Income Doesn T Have To Be Difficult Learn More About Social Media Advertising Facebook Advertising Shopify Ecommerce And Ebay

Authors: Mark Graham

1st Edition

0648678830, 978-0648678830