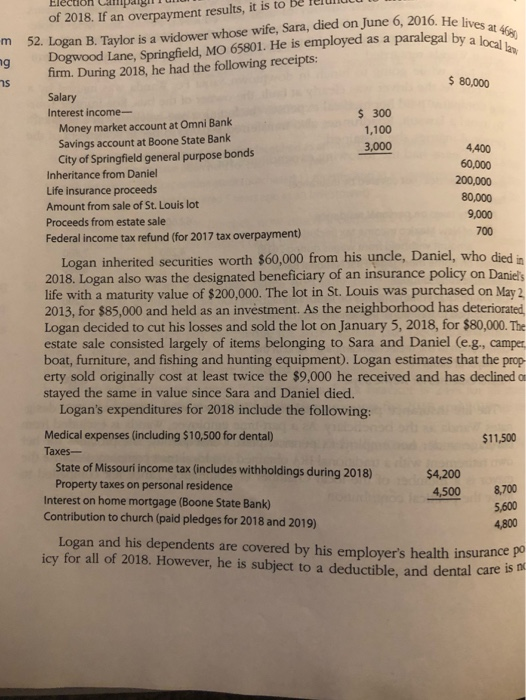

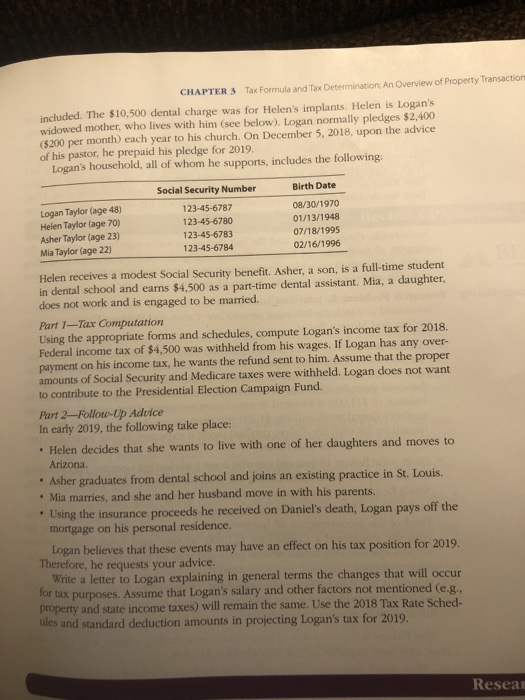

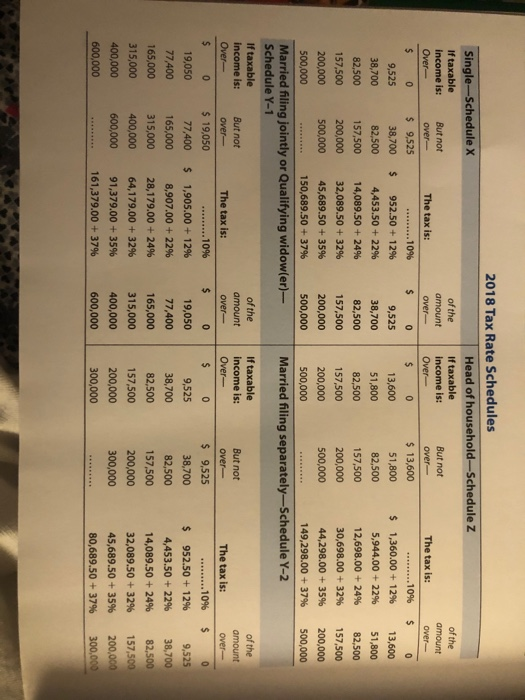

Election Campaign He lives at 466 by a local law E of 2018. If an overpayment results, it is to be relun to 52. Logan B. Taylor is a widower whose wife, Sara, died on June 6, 2016. He liv Dogwood Lane, Springfield, MO 65801. He is employed as a paralegal by a firm. During 2018, he had the following receipts: $ 80,000 Salary Interest income- $ 300 Money market account at Omni Bank 1,100 Savings account at Boone State Bank 3,000 4,400 City of Springfield general purpose bonds 60,000 Inheritance from Daniel Life insurance proceeds 200,000 Amount from sale of St. Louis lot 80,000 Proceeds from estate sale 9,000 Federal income tax refund (for 2017 tax overpayment) 700 Logan inherited securities worth $60,000 from his uncle, Daniel, who died in 2018. Logan also was the designated beneficiary of an insurance policy on Daniel's life with a maturity value of $200,000. The lot in St. Louis was purchased on May 2 2013, for $85,000 and held as an investment. As the neighborhood has deteriorated Logan decided to cut his losses and sold the lot on January 5, 2018, for $80,000. The estate sale consisted largely of items belonging to Sara and Daniel (e.g., camper boat, furniture, and fishing and hunting equipment). Logan estimates that the prop erty sold originally cost at least twice the $9,000 he received and has declined a stayed the same in value since Sara and Daniel died. Logan's expenditures for 2018 include the following: $11,500 Medical expenses (including $10,500 for dental) Taxes- State of Missouri income tax (includes withholdings during 2018) Property taxes on personal residence Interest on home mortgage (Boone State Bank) Contribution to church (paid pledges for 2018 and 2019) $4,200 4,500 8,700 5,600 4,800 Logan and his dependents are covered by his employer's health insurance po icy for all of 2018. However, he is subject to a deductible, and dental care CHAPTER 3 Tax Formula and Tax Determination An Overview of Property Transactie included. The $10,500 dental charge was for Helen's implants. Helen is Logan's widowed mother, who lives with him (see below). Logan normally pledges $2,400 ($200 per month) each year to his church On December 5, 2018, upon the advice of his pastor, he prepaid his pledge for 2019. Logan's household, all of whom he supports, includes the following: Logan Taylor (age 48) Helen Taylor (age 70) Asher Taylor (age 23) Mia Taylor (age 22) Social Security Number 123-45-6787 123-45-6780 123-45-6783 123-45-6784 Birth Date 08/30/1970 01/13/1948 07/18/1995 02/16/1996 Helen receives a modest Social Security benefit. Asher, a son, is a full-time student in dental school and earns $4,500 as a part-time dental assistant Mia, a daughter, does not work and is engaged to be married. Part 1Tax Computation Using the appropriate forms and schedules, compute Logan's income tax for 2018. Federal income tax of $4,500 was withheld from his wages. If Logan has any over- payment on his income tax, he wants the refund sent to him. Assume that the proper amounts of Social Security and Medicare taxes were withheld. Logan does not want to contribute to the Presidential Election Campaign Fund. Part 2-Follow-Up Advice In early 2019, the following take place: Helen decides that she wants to live with one of her daughters and moves to Arizona Asher graduates from dental school and joins an existing practice in St. Louis, Mia marries, and she and her husband move in with his parents. . Using the insurance proceeds he received on Daniel's death, Logan pays off the mortgage on his personal residence. Logan believes that these events may have an effect on his tax position for 2019. Therefore, he requests your advice. Write a letter to Logan explaining in general terms the changes that will occur for tax purposes. Assume that Logan's salary and other factors not mentioned (e.g.. property and state income taxes) will remain the same. Use the 2018 Tax Rate Sched- ules and standard deduction amounts in projecting Logan's tax for 2019. Reseal of the amount Over $ 0 13,600 51,800 82,500 157,500 200,000 500,000 2018 Tax Rate Schedules Single-Schedule X Head of household-Schedule z If taxable of the If taxable Income is: But not amount income is: But not Over over- The tax is: over- Over- over- The tax is: $ 0 $ 9,525 .......10% $ 0 $ 0 $ 13,600 .........10% 9,525 38,700 $ 952.50 +12% 9,525 13,600 51,800 $ 1,360.00 + 12% 38,700 82,500 4,453.50 +22% 38,700 51,800 82,500 5,944.00 + 22% 82,500 157,500 14,089.50 +24% 82,500 82,500 157,500 12,698.00 + 24% 157,500 200,000 32,089.50 + 32% 157,500 157,500 200,000 30,698.00 + 32% 200,000 500,000 45,689.50 + 35% 200,000 200,000 500,000 44,298.00 + 35% 500,000 150,689.50 + 37% 500,000 500,000 149,298.00 + 37% Married filing jointly or Qualifying widow(er) Married filing separately-Schedule Y-2 Schedule Y-1 If taxable of the If taxable income is: But not amount income is: But not Over over- The tax is: over- Over- over- The tax is: $ 0 $ 19,050 $ 0 $ 0 $ 9,525 .... 10% 19,050 77,400 $ 1,905.00 + 12% 19,050 9,525 38,700 $ 952.50 +12% 77,400 165,000 8,907.00 + 22% 77,400 38,700 82,500 4,453.50 + 22% 165,000 315,000 28,179.00 +24% 165,000 82,500 157,500 14,089.50 + 24% 315,000 400,000 64,179.00 + 32% 315,000 157,500 200,000 32,089.50 + 32% 400,000 600,000 91,379.00 + 35% 400,000 200,000 300,000 45,689.50 + 35% 600,000 161,379.00 + 37% 600,000 300,000 80,689.50 + 37% ........ 10% of the amount over- $ 0 9,525 38,700 82,500 157,500 200,000 300,000 Election Campaign He lives at 466 by a local law E of 2018. If an overpayment results, it is to be relun to 52. Logan B. Taylor is a widower whose wife, Sara, died on June 6, 2016. He liv Dogwood Lane, Springfield, MO 65801. He is employed as a paralegal by a firm. During 2018, he had the following receipts: $ 80,000 Salary Interest income- $ 300 Money market account at Omni Bank 1,100 Savings account at Boone State Bank 3,000 4,400 City of Springfield general purpose bonds 60,000 Inheritance from Daniel Life insurance proceeds 200,000 Amount from sale of St. Louis lot 80,000 Proceeds from estate sale 9,000 Federal income tax refund (for 2017 tax overpayment) 700 Logan inherited securities worth $60,000 from his uncle, Daniel, who died in 2018. Logan also was the designated beneficiary of an insurance policy on Daniel's life with a maturity value of $200,000. The lot in St. Louis was purchased on May 2 2013, for $85,000 and held as an investment. As the neighborhood has deteriorated Logan decided to cut his losses and sold the lot on January 5, 2018, for $80,000. The estate sale consisted largely of items belonging to Sara and Daniel (e.g., camper boat, furniture, and fishing and hunting equipment). Logan estimates that the prop erty sold originally cost at least twice the $9,000 he received and has declined a stayed the same in value since Sara and Daniel died. Logan's expenditures for 2018 include the following: $11,500 Medical expenses (including $10,500 for dental) Taxes- State of Missouri income tax (includes withholdings during 2018) Property taxes on personal residence Interest on home mortgage (Boone State Bank) Contribution to church (paid pledges for 2018 and 2019) $4,200 4,500 8,700 5,600 4,800 Logan and his dependents are covered by his employer's health insurance po icy for all of 2018. However, he is subject to a deductible, and dental care CHAPTER 3 Tax Formula and Tax Determination An Overview of Property Transactie included. The $10,500 dental charge was for Helen's implants. Helen is Logan's widowed mother, who lives with him (see below). Logan normally pledges $2,400 ($200 per month) each year to his church On December 5, 2018, upon the advice of his pastor, he prepaid his pledge for 2019. Logan's household, all of whom he supports, includes the following: Logan Taylor (age 48) Helen Taylor (age 70) Asher Taylor (age 23) Mia Taylor (age 22) Social Security Number 123-45-6787 123-45-6780 123-45-6783 123-45-6784 Birth Date 08/30/1970 01/13/1948 07/18/1995 02/16/1996 Helen receives a modest Social Security benefit. Asher, a son, is a full-time student in dental school and earns $4,500 as a part-time dental assistant Mia, a daughter, does not work and is engaged to be married. Part 1Tax Computation Using the appropriate forms and schedules, compute Logan's income tax for 2018. Federal income tax of $4,500 was withheld from his wages. If Logan has any over- payment on his income tax, he wants the refund sent to him. Assume that the proper amounts of Social Security and Medicare taxes were withheld. Logan does not want to contribute to the Presidential Election Campaign Fund. Part 2-Follow-Up Advice In early 2019, the following take place: Helen decides that she wants to live with one of her daughters and moves to Arizona Asher graduates from dental school and joins an existing practice in St. Louis, Mia marries, and she and her husband move in with his parents. . Using the insurance proceeds he received on Daniel's death, Logan pays off the mortgage on his personal residence. Logan believes that these events may have an effect on his tax position for 2019. Therefore, he requests your advice. Write a letter to Logan explaining in general terms the changes that will occur for tax purposes. Assume that Logan's salary and other factors not mentioned (e.g.. property and state income taxes) will remain the same. Use the 2018 Tax Rate Sched- ules and standard deduction amounts in projecting Logan's tax for 2019. Reseal of the amount Over $ 0 13,600 51,800 82,500 157,500 200,000 500,000 2018 Tax Rate Schedules Single-Schedule X Head of household-Schedule z If taxable of the If taxable Income is: But not amount income is: But not Over over- The tax is: over- Over- over- The tax is: $ 0 $ 9,525 .......10% $ 0 $ 0 $ 13,600 .........10% 9,525 38,700 $ 952.50 +12% 9,525 13,600 51,800 $ 1,360.00 + 12% 38,700 82,500 4,453.50 +22% 38,700 51,800 82,500 5,944.00 + 22% 82,500 157,500 14,089.50 +24% 82,500 82,500 157,500 12,698.00 + 24% 157,500 200,000 32,089.50 + 32% 157,500 157,500 200,000 30,698.00 + 32% 200,000 500,000 45,689.50 + 35% 200,000 200,000 500,000 44,298.00 + 35% 500,000 150,689.50 + 37% 500,000 500,000 149,298.00 + 37% Married filing jointly or Qualifying widow(er) Married filing separately-Schedule Y-2 Schedule Y-1 If taxable of the If taxable income is: But not amount income is: But not Over over- The tax is: over- Over- over- The tax is: $ 0 $ 19,050 $ 0 $ 0 $ 9,525 .... 10% 19,050 77,400 $ 1,905.00 + 12% 19,050 9,525 38,700 $ 952.50 +12% 77,400 165,000 8,907.00 + 22% 77,400 38,700 82,500 4,453.50 + 22% 165,000 315,000 28,179.00 +24% 165,000 82,500 157,500 14,089.50 + 24% 315,000 400,000 64,179.00 + 32% 315,000 157,500 200,000 32,089.50 + 32% 400,000 600,000 91,379.00 + 35% 400,000 200,000 300,000 45,689.50 + 35% 600,000 161,379.00 + 37% 600,000 300,000 80,689.50 + 37% ........ 10% of the amount over- $ 0 9,525 38,700 82,500 157,500 200,000 300,000