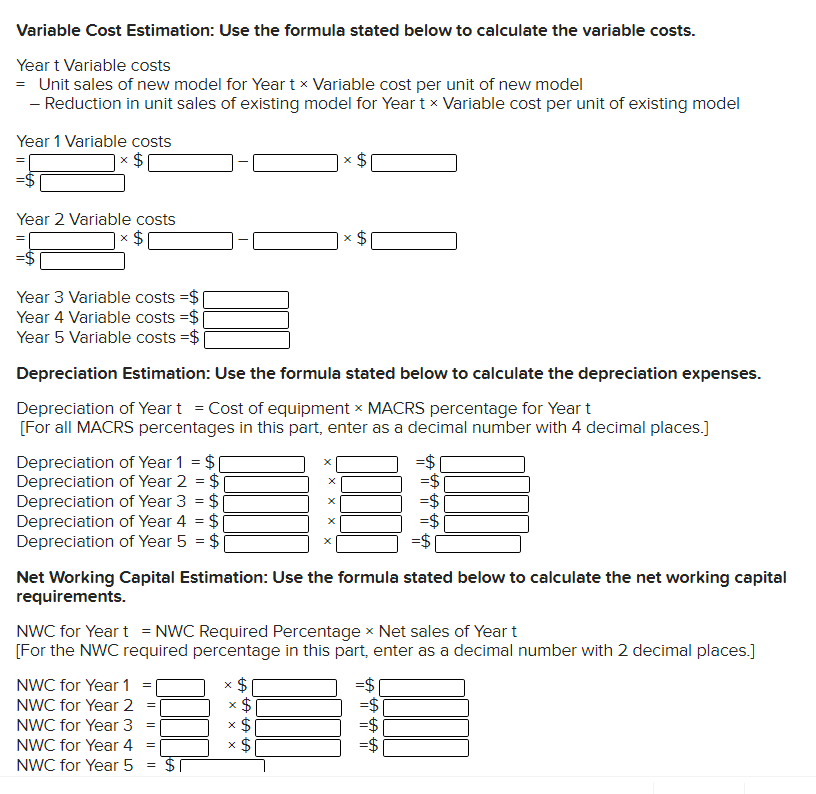

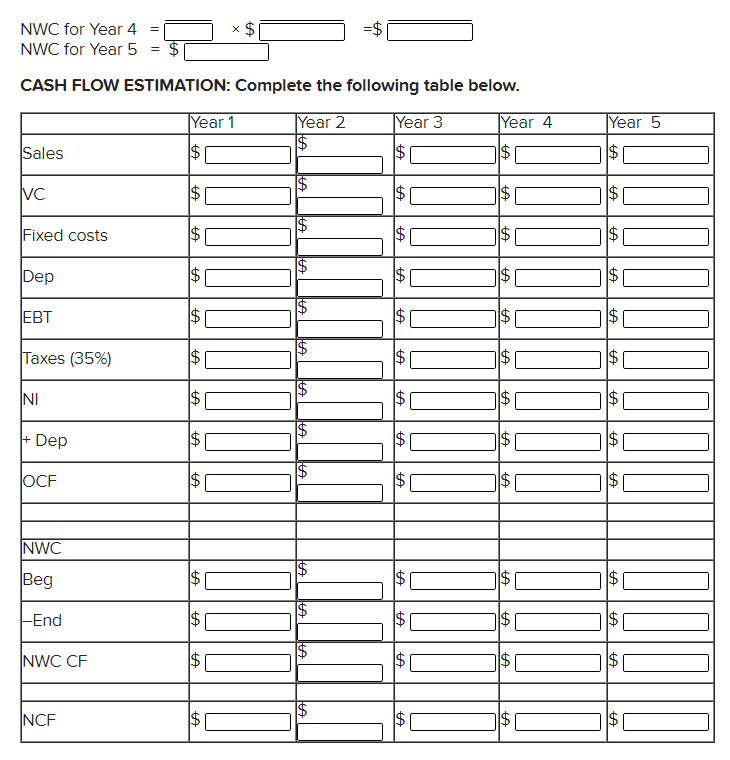

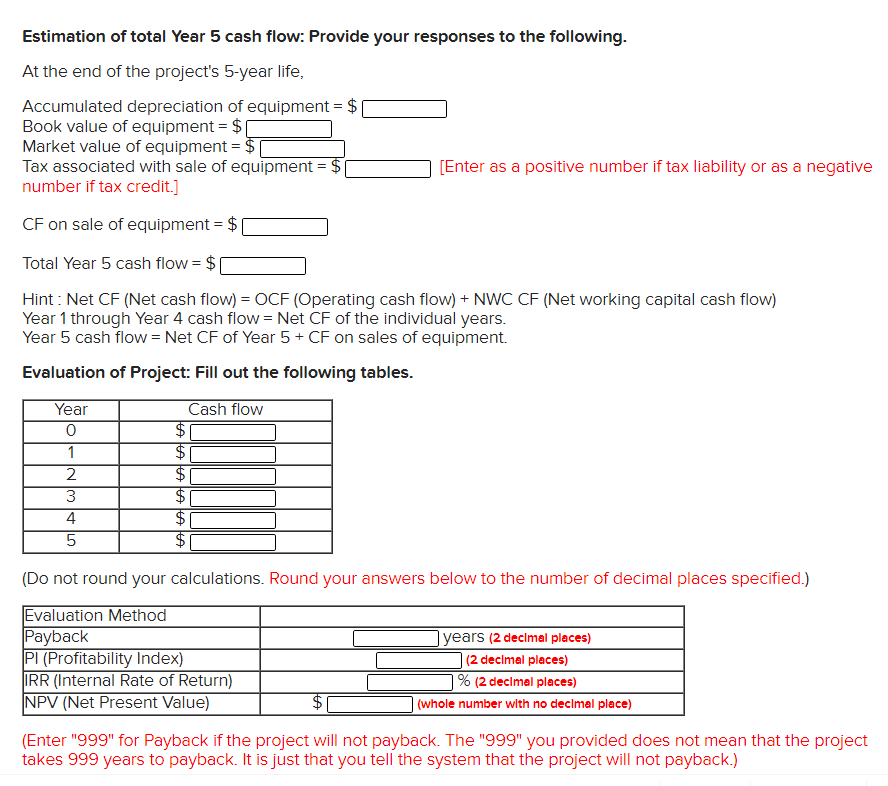

Elite Motor, Inc. is a producer of mountain bikes. Its current line of non-folding mountain bikes are selling excellently. However, in order to cope with the foreseeable competition with other similar bikes, Elite Motor spent $6,000,000 to develop a new line of folding mountain bikes (new model development cost). The added convenience of portability of this new streamline 25 speed 26" frame bike model enables users a great ride anywhere, not just on mountain trails. It is easy to install and great for students, office workers, urban environments, or any convenient commuting. Elite Motor will adjust the shifting and braking for this bike model and make its disc brakes automatically adaptable. Users can easily asjust the tension of the brake cable of the disc brake if they find the brakes not tight enough for themselves. Its frame is made of high carbon steel, with seat distance between 30 inches and 34 inches from the ground and handle 37 inches also from the ground. The model works well for men and women of height between 5'3"- 6'2" and weight of 220 lb max. The company had also spent a further $1,200,000 to study the marketability of this new line of folding mountain bikes (marketability studying cost). Elite Motor is able to produce the new mountain bikes at a variable cost of $70 each. The total fixed costs for the operation are expected to be $9,000,000 per year. Elite Motor expects to sell 3,200,000 bikes, 3,600,000 bikes, 2,600,000 bikes, 1,800,000 bikes and 1,000,000 bikes of the new model per year over the next five years respectively. The new bikes will be selling at a price of $140 each. To launch this new line of production, Elite Motor needs to invest $32,000,000 in equipment which will be depreciated on a seven-year MACRS schedule. The value of the used equipment is expected to be worth $4,000,000 as at the end of the 5 year project life. Elite Motor is planning to stop producing the existing mountain bikes entirely in two years. Should Elite Motor not introduce the new folding mountain bikes, sales per year of the existing non-folding mountain bikes will be 1,600,000 bikes and 1,250,000 bikes for the next two years respectively. The existing model can be produced at variable costs of $60 each and total fixed costs of $7,500,000 per year. The existing mountain bikes are selling for $110 each. If Elite Motor produces the new model, sales of existing model will be eroded y 960,000 bikes for next year and 1,062,500 bikes for the year after next. In addition, to promote sales of the existing model alongside with the new model, Elite Motor has to reduce the price of the existing model to $80 each. Net working capital for this new folding mountain bike project will be 15 percent of sales and will vary with the occurrence of the cash flows. As such, there will be no initial NWC required. The first change in NWC is expected to occur in year 1 according to the sales of the year. Elite Motor is currently in the tax bracket of 35 percent and it requires a 18 percent returns on all of its projects. The firm also requires a payback of 3 years for all projects. You have just been hired by EliteBike as a financial consultant to advise them on this new folding mountain bike project. You are expected to provide answers to the following questions to their management by their next meeting which is scheduled sometime next Jmonth What is/are the sunk cost(s) for this new folding mountain bike project? Briefly explain. You have to tell what sunk cost is and the amount of the total sunk cost(s). In addition, you have to advise Elite Motor on how to handle such cost(s). What are the cash flows of the project for each year? What is the payback period of the project? What is the Pl (profitability index) of the project? What is the IRR (internal rate of return) of the project? What is the NPV (net present value) of the project? Should the project be accepted based on Payback, PI, IRR and NPV? Briefly explain. ***** When you have read the above case background information and what you are asked to do (as a financial consultant, not as a student) about the case study, you need to go to Canvas to complete Part 1 (Summary Writing) of this case study. Please write your summary before you complete Part 2 below. Part 2 (Calculation) Capital Budgeting Analysis Before working on the calculations below, please study well the Example Case Study for Chapter 10: Rainbow's New Premium Truck Camper and its solution (already posted to both 11 Things to Study under the Week Eleven [Week of March 29) module and the Case Study (Part 2: Calculations) and Case Study (Part 3: Essay/Analysis) on Canvas. Your Name: those that you use on Canvas.) (First Name then Last Name, need to be exactly the same as The following steps will walk you through on how you should do your calculations for this case study. You follow the instructions and provide your responses accordingly. Please enter ALL the dollar amounts (including cash flows) below in whole numbers. Estimation of sunk costs Provide below the amounts of the sunk costs you identified from the case description above. 1st sunk cost: $ being cost (Use exactly the same wording as in the case background information.) being cost (Use exactly the same wording as in the case 2nd sunk cost: $ background information.) Total sunk costs = $ Net Sales Estimation: Use the formula stated below to calculate the net sales. Yeart Net Sales =Unit sales of new model for Year t x Price of new model - Reduction in unit sales of existing model for Year tx Current price of existing model [(Unit sales of existing model for Yeart if new model project is not launched Reduction in unit sales of existing model if new model project is launched) * (Current price of existing model Reduced price of existing model)] Year 1 Net Sales x $ = $ Year 2 Net Sales = x $ $ $ Year 3 Net Sales = $ Year 4 Net Sales = $ Old Year 5 Net Sales = $ Variable Cost Estimation: Use the formula stated below to calculate the variable costs. Yeart Variable costs = Unit sales of new model for Year 1 x Variable cost per unit of new model - Reduction in unit sales of existing model for Yeart Variable cost per unit of existing model Year 1 Variable costs Year 2 Variable costs $ Year 3 Variable costs =$ Year 4 Variable costs =$1 Year 5 Variable costs =$| Depreciation Estimation: Use the formula stated below to calculate the depreciation expenses. Depreciation of Yeart = Cost of equipment * MACRS percentage for Yeart [For all MACRS percentages in this part, enter as a decimal number with 4 decimal places.] Depreciation of Year 1 = $ Depreciation of Year 2 = $ Depreciation of Year 3 = $ Depreciation of Year 4 = $ Depreciation of Year 5 = $ Net Working Capital Estimation: Use the formula stated below to calculate the net working capital requirements. NWC for Yeart = NWC Required Percentage * Net sales of Yeart [For the NWC required percentage in this part, enter as a decimal number with 2 decimal places.] NWC for Year 1 = 1 NWC for Year 2 x $ NWC for Year 3 * $ NWC for Year 4 $ NWC for Year 5 ST AA TATA Variable Cost Estimation: Use the formula stated below to calculate the variable costs. Yeart Variable costs = Unit sales of new model for Year 1 x Variable cost per unit of new model - Reduction in unit sales of existing model for Yeart Variable cost per unit of existing model Year 1 Variable costs Year 2 Variable costs $ Year 3 Variable costs =$ Year 4 Variable costs =$1 Year 5 Variable costs =$| Depreciation Estimation: Use the formula stated below to calculate the depreciation expenses. Depreciation of Yeart = Cost of equipment * MACRS percentage for Yeart [For all MACRS percentages in this part, enter as a decimal number with 4 decimal places.] Depreciation of Year 1 = $ Depreciation of Year 2 = $ Depreciation of Year 3 = $ Depreciation of Year 4 = $ Depreciation of Year 5 = $ Net Working Capital Estimation: Use the formula stated below to calculate the net working capital requirements. NWC for Yeart = NWC Required Percentage * Net sales of Yeart [For the NWC required percentage in this part, enter as a decimal number with 2 decimal places.] NWC for Year 1 = 1 NWC for Year 2 x $ NWC for Year 3 * $ NWC for Year 4 $ NWC for Year 5 ST AA TATA = x4 NWC for Year 4 NWC for Year 5 CASH FLOW ESTIMATION: Complete the following table below. Year 1 Year 3 IYear 4 Year 5 Year 2 $ LA Sales $ $ $ HA VC $ $ $ HA Fixed costs $ $ $ A Dep $ LA IEBT $ $ $ Taxes (35%) $1 LA INI || $1 1 $ F Dep $ A 0 A HA OCF $ $1 LA $ INWC Beg A $1 LA $ HA -End $ $ $ || HA INWC CF $ $0 A HA INCF A $1 LA Estimation of total Year 5 cash flow: Provide your responses to the following. At the end of the project's 5-year life, Accumulated depreciation of equipment = $ Book value of equipment = $( Market value of equipment = $ [ Tax associated with sale of equipment = $ [Enter as a positive number if tax liability or as a negative number if tax credit.] CF on sale of equipment = $ Total Year 5 cash flow = $ Hint: Net CF (Net cash flow) = OCF (Operating cash flow) + NWC CF (Net working capital cash flow) Year 1 through Year 4 cash flow = Net CF of the individual years. Year 5 cash flow = Net CF of Year 5 +CF on sales of equipment. Evaluation of Project: Fill out the following tables. Year Cash flow 0 $ 1 HAJAJAJA 4 5 (Do not round your calculations. Round your answers below to the number of decimal places specified.) Evaluation Method Payback Pl(Profitability Index) IRR (Internal Rate of Return) NPV (Net Present Value) years (2 decimal places) (2 decimal places) % (2 decimal places) (whole number with no decimal place) (Enter "999" for Payback if the project will not payback. The "999" you provided does not mean that the project takes 999 years to payback. It is just that you tell the system that the project will not payback.) Elite Motor, Inc. is a producer of mountain bikes. Its current line of non-folding mountain bikes are selling excellently. However, in order to cope with the foreseeable competition with other similar bikes, Elite Motor spent $6,000,000 to develop a new line of folding mountain bikes (new model development cost). The added convenience of portability of this new streamline 25 speed 26" frame bike model enables users a great ride anywhere, not just on mountain trails. It is easy to install and great for students, office workers, urban environments, or any convenient commuting. Elite Motor will adjust the shifting and braking for this bike model and make its disc brakes automatically adaptable. Users can easily asjust the tension of the brake cable of the disc brake if they find the brakes not tight enough for themselves. Its frame is made of high carbon steel, with seat distance between 30 inches and 34 inches from the ground and handle 37 inches also from the ground. The model works well for men and women of height between 5'3"- 6'2" and weight of 220 lb max. The company had also spent a further $1,200,000 to study the marketability of this new line of folding mountain bikes (marketability studying cost). Elite Motor is able to produce the new mountain bikes at a variable cost of $70 each. The total fixed costs for the operation are expected to be $9,000,000 per year. Elite Motor expects to sell 3,200,000 bikes, 3,600,000 bikes, 2,600,000 bikes, 1,800,000 bikes and 1,000,000 bikes of the new model per year over the next five years respectively. The new bikes will be selling at a price of $140 each. To launch this new line of production, Elite Motor needs to invest $32,000,000 in equipment which will be depreciated on a seven-year MACRS schedule. The value of the used equipment is expected to be worth $4,000,000 as at the end of the 5 year project life. Elite Motor is planning to stop producing the existing mountain bikes entirely in two years. Should Elite Motor not introduce the new folding mountain bikes, sales per year of the existing non-folding mountain bikes will be 1,600,000 bikes and 1,250,000 bikes for the next two years respectively. The existing model can be produced at variable costs of $60 each and total fixed costs of $7,500,000 per year. The existing mountain bikes are selling for $110 each. If Elite Motor produces the new model, sales of existing model will be eroded y 960,000 bikes for next year and 1,062,500 bikes for the year after next. In addition, to promote sales of the existing model alongside with the new model, Elite Motor has to reduce the price of the existing model to $80 each. Net working capital for this new folding mountain bike project will be 15 percent of sales and will vary with the occurrence of the cash flows. As such, there will be no initial NWC required. The first change in NWC is expected to occur in year 1 according to the sales of the year. Elite Motor is currently in the tax bracket of 35 percent and it requires a 18 percent returns on all of its projects. The firm also requires a payback of 3 years for all projects. You have just been hired by EliteBike as a financial consultant to advise them on this new folding mountain bike project. You are expected to provide answers to the following questions to their management by their next meeting which is scheduled sometime next Jmonth What is/are the sunk cost(s) for this new folding mountain bike project? Briefly explain. You have to tell what sunk cost is and the amount of the total sunk cost(s). In addition, you have to advise Elite Motor on how to handle such cost(s). What are the cash flows of the project for each year? What is the payback period of the project? What is the Pl (profitability index) of the project? What is the IRR (internal rate of return) of the project? What is the NPV (net present value) of the project? Should the project be accepted based on Payback, PI, IRR and NPV? Briefly explain. ***** When you have read the above case background information and what you are asked to do (as a financial consultant, not as a student) about the case study, you need to go to Canvas to complete Part 1 (Summary Writing) of this case study. Please write your summary before you complete Part 2 below. Part 2 (Calculation) Capital Budgeting Analysis Before working on the calculations below, please study well the Example Case Study for Chapter 10: Rainbow's New Premium Truck Camper and its solution (already posted to both 11 Things to Study under the Week Eleven [Week of March 29) module and the Case Study (Part 2: Calculations) and Case Study (Part 3: Essay/Analysis) on Canvas. Your Name: those that you use on Canvas.) (First Name then Last Name, need to be exactly the same as The following steps will walk you through on how you should do your calculations for this case study. You follow the instructions and provide your responses accordingly. Please enter ALL the dollar amounts (including cash flows) below in whole numbers. Estimation of sunk costs Provide below the amounts of the sunk costs you identified from the case description above. 1st sunk cost: $ being cost (Use exactly the same wording as in the case background information.) being cost (Use exactly the same wording as in the case 2nd sunk cost: $ background information.) Total sunk costs = $ Net Sales Estimation: Use the formula stated below to calculate the net sales. Yeart Net Sales =Unit sales of new model for Year t x Price of new model - Reduction in unit sales of existing model for Year tx Current price of existing model [(Unit sales of existing model for Yeart if new model project is not launched Reduction in unit sales of existing model if new model project is launched) * (Current price of existing model Reduced price of existing model)] Year 1 Net Sales x $ = $ Year 2 Net Sales = x $ $ $ Year 3 Net Sales = $ Year 4 Net Sales = $ Old Year 5 Net Sales = $ Variable Cost Estimation: Use the formula stated below to calculate the variable costs. Yeart Variable costs = Unit sales of new model for Year 1 x Variable cost per unit of new model - Reduction in unit sales of existing model for Yeart Variable cost per unit of existing model Year 1 Variable costs Year 2 Variable costs $ Year 3 Variable costs =$ Year 4 Variable costs =$1 Year 5 Variable costs =$| Depreciation Estimation: Use the formula stated below to calculate the depreciation expenses. Depreciation of Yeart = Cost of equipment * MACRS percentage for Yeart [For all MACRS percentages in this part, enter as a decimal number with 4 decimal places.] Depreciation of Year 1 = $ Depreciation of Year 2 = $ Depreciation of Year 3 = $ Depreciation of Year 4 = $ Depreciation of Year 5 = $ Net Working Capital Estimation: Use the formula stated below to calculate the net working capital requirements. NWC for Yeart = NWC Required Percentage * Net sales of Yeart [For the NWC required percentage in this part, enter as a decimal number with 2 decimal places.] NWC for Year 1 = 1 NWC for Year 2 x $ NWC for Year 3 * $ NWC for Year 4 $ NWC for Year 5 ST AA TATA Variable Cost Estimation: Use the formula stated below to calculate the variable costs. Yeart Variable costs = Unit sales of new model for Year 1 x Variable cost per unit of new model - Reduction in unit sales of existing model for Yeart Variable cost per unit of existing model Year 1 Variable costs Year 2 Variable costs $ Year 3 Variable costs =$ Year 4 Variable costs =$1 Year 5 Variable costs =$| Depreciation Estimation: Use the formula stated below to calculate the depreciation expenses. Depreciation of Yeart = Cost of equipment * MACRS percentage for Yeart [For all MACRS percentages in this part, enter as a decimal number with 4 decimal places.] Depreciation of Year 1 = $ Depreciation of Year 2 = $ Depreciation of Year 3 = $ Depreciation of Year 4 = $ Depreciation of Year 5 = $ Net Working Capital Estimation: Use the formula stated below to calculate the net working capital requirements. NWC for Yeart = NWC Required Percentage * Net sales of Yeart [For the NWC required percentage in this part, enter as a decimal number with 2 decimal places.] NWC for Year 1 = 1 NWC for Year 2 x $ NWC for Year 3 * $ NWC for Year 4 $ NWC for Year 5 ST AA TATA = x4 NWC for Year 4 NWC for Year 5 CASH FLOW ESTIMATION: Complete the following table below. Year 1 Year 3 IYear 4 Year 5 Year 2 $ LA Sales $ $ $ HA VC $ $ $ HA Fixed costs $ $ $ A Dep $ LA IEBT $ $ $ Taxes (35%) $1 LA INI || $1 1 $ F Dep $ A 0 A HA OCF $ $1 LA $ INWC Beg A $1 LA $ HA -End $ $ $ || HA INWC CF $ $0 A HA INCF A $1 LA Estimation of total Year 5 cash flow: Provide your responses to the following. At the end of the project's 5-year life, Accumulated depreciation of equipment = $ Book value of equipment = $( Market value of equipment = $ [ Tax associated with sale of equipment = $ [Enter as a positive number if tax liability or as a negative number if tax credit.] CF on sale of equipment = $ Total Year 5 cash flow = $ Hint: Net CF (Net cash flow) = OCF (Operating cash flow) + NWC CF (Net working capital cash flow) Year 1 through Year 4 cash flow = Net CF of the individual years. Year 5 cash flow = Net CF of Year 5 +CF on sales of equipment. Evaluation of Project: Fill out the following tables. Year Cash flow 0 $ 1 HAJAJAJA 4 5 (Do not round your calculations. Round your answers below to the number of decimal places specified.) Evaluation Method Payback Pl(Profitability Index) IRR (Internal Rate of Return) NPV (Net Present Value) years (2 decimal places) (2 decimal places) % (2 decimal places) (whole number with no decimal place) (Enter "999" for Payback if the project will not payback. The "999" you provided does not mean that the project takes 999 years to payback. It is just that you tell the system that the project will not payback.)