Answered step by step

Verified Expert Solution

Question

1 Approved Answer

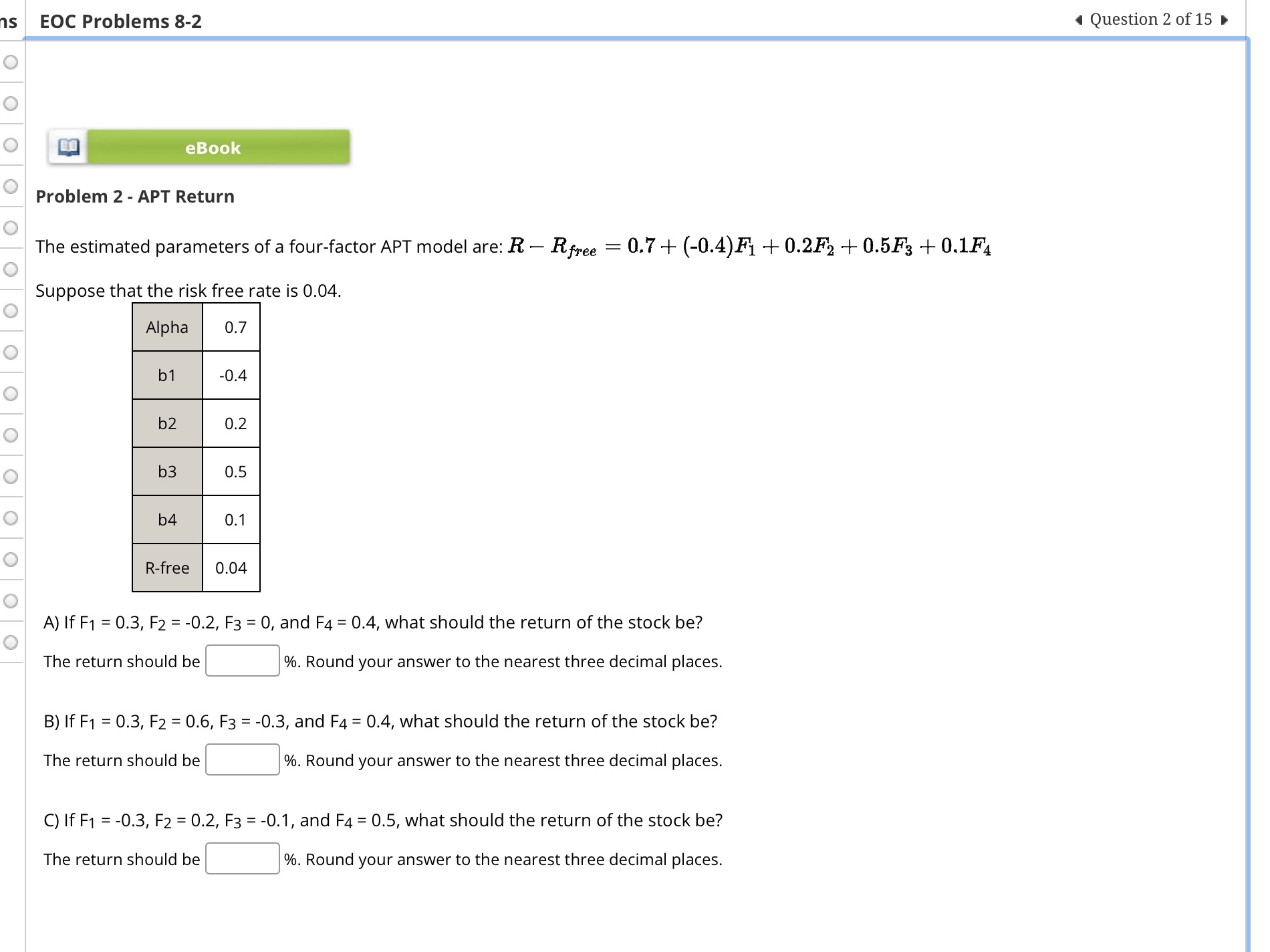

EOC Problems 8 - 2 Question 2 of 1 5 eBook Problem 2 - APT Return The estimated parameters of a four - factor APT

EOC Problems Question of eBook Problem APT Return The estimated parameters of a fourfactor APT model are: Suppose that the risk free rate is tableAlphabbbbRfree, A If and what should the return of the stock be The return should be Round your answer to the nearest three decimal places. B If and what should the return of the stock be The return should be Round your answer to the nearest three decimal places. C If and what should the return of the stock be The return should be Round your answer to the nearest three decimal places.

EOC Problems

Question of

eBook

Problem APT Return

The estimated parameters of a fourfactor APT model are: Suppose that the risk free rate is

tableAlphabbbbRfree,

A If and what should the return of the stock be

The return should be

Round your answer to the nearest three decimal places.

B If and what should the return of the stock be

The return should be

Round your answer to the nearest three decimal places.

C If and what should the return of the stock be

The return should be

Round your answer to the nearest three decimal places.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Of Synthetic Finance Three Essays Of Speculative Materialism

Authors: Benjamin Lozano

1st Edition

1138790842, 978-1138790841