Answered step by step

Verified Expert Solution

Question

1 Approved Answer

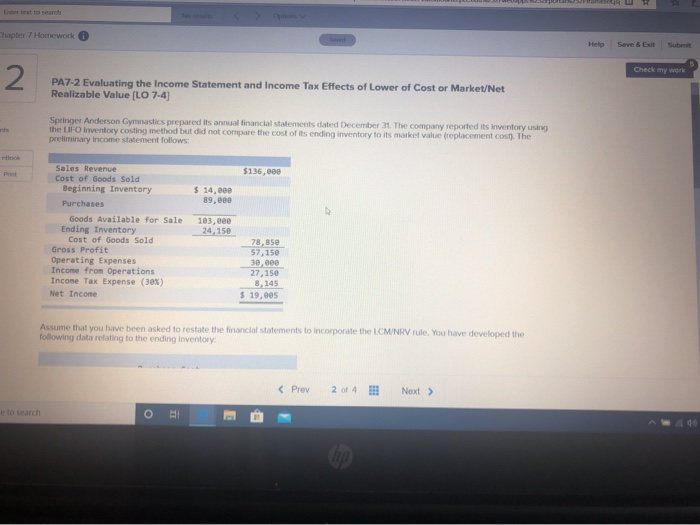

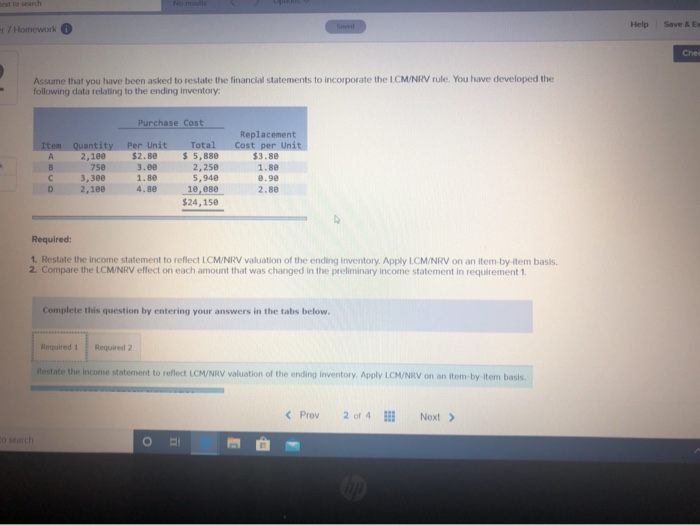

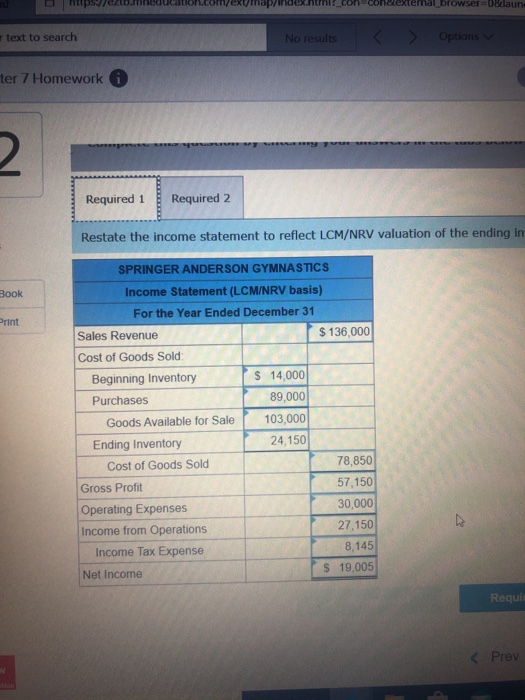

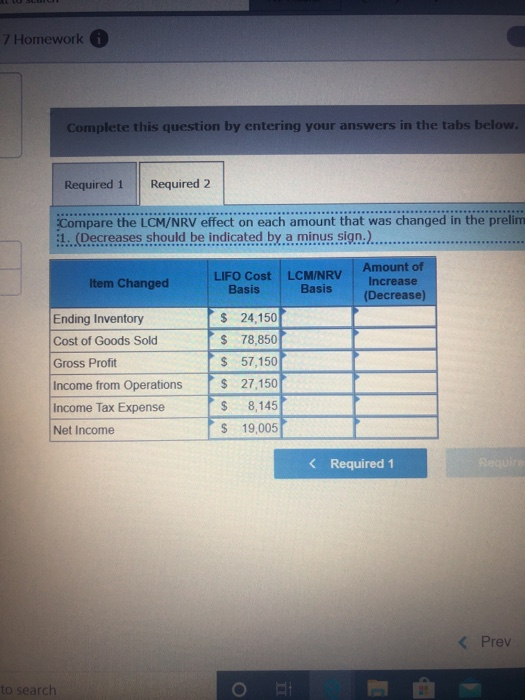

Erter text to search Chapter 7 Homework Help Save & Exit Check my work 2. PA7-2 Evaluating the Income Statement and Income Tax Effects of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Behind Closed Doors What Company Audit Is Really About

Authors: V. Beattie, R. Brandt, S. Fearnley

2001 Edition

0333747844, 978-0333747841