Answered step by step

Verified Expert Solution

Question

1 Approved Answer

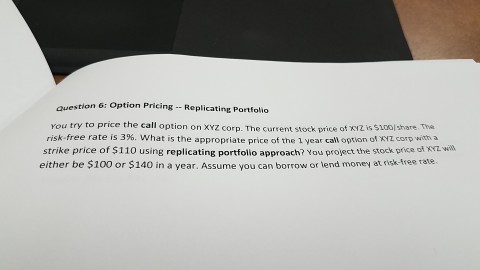

estion 6: Option Pricing Replicating Portfolio You try to price the call option on XYZ corp. The current stock price of Yerzissioolshare The risk-free rate

estion 6: Option Pricing Replicating Portfolio You try to price the call option on XYZ corp. The current stock price of Yerzissioolshare The risk-free rate is 3%. What is the appropriate price of the 1 year cal opwon of KHLcovwoh a strike price of $110 using replicating portfolio approach? You proyectthe stock prvee of either be $100 or S140 in a year. Assume you can borrow or lend money at risk-Asee Tales

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of Loan Syndications And Trading

Authors: Marsh, Lee Shaiman, Bridget Marsh

2nd Edition

1264258526, 978-1264258529