Answered step by step

Verified Expert Solution

Question

1 Approved Answer

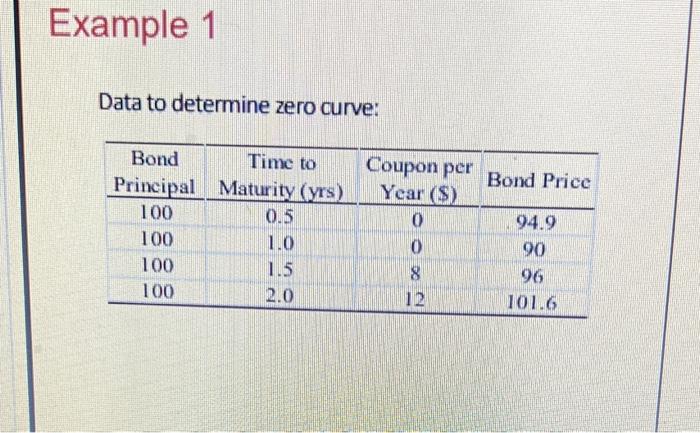

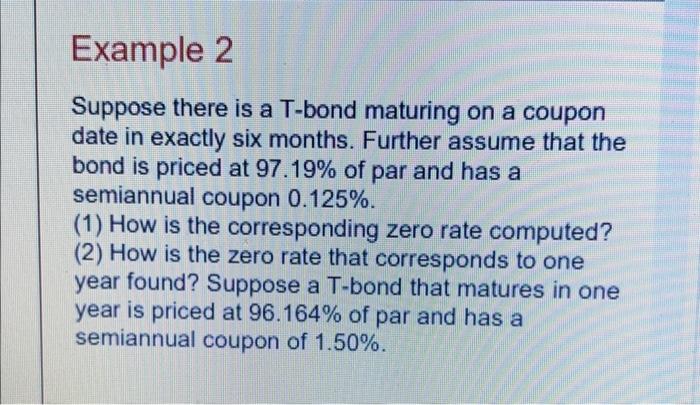

example 1: asking for: determining zero rates ( bootstrapping zero rates) Data to determine zero curve: Suppose there is a T-bond maturing on a coupon

example 1: asking for: determining zero rates ( bootstrapping zero rates)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Unlocking The Door To Real Estate Success Achieving Passive Income

Authors: Benjamin Stone

1st Edition

979-8856252278