Answered step by step

Verified Expert Solution

Question

1 Approved Answer

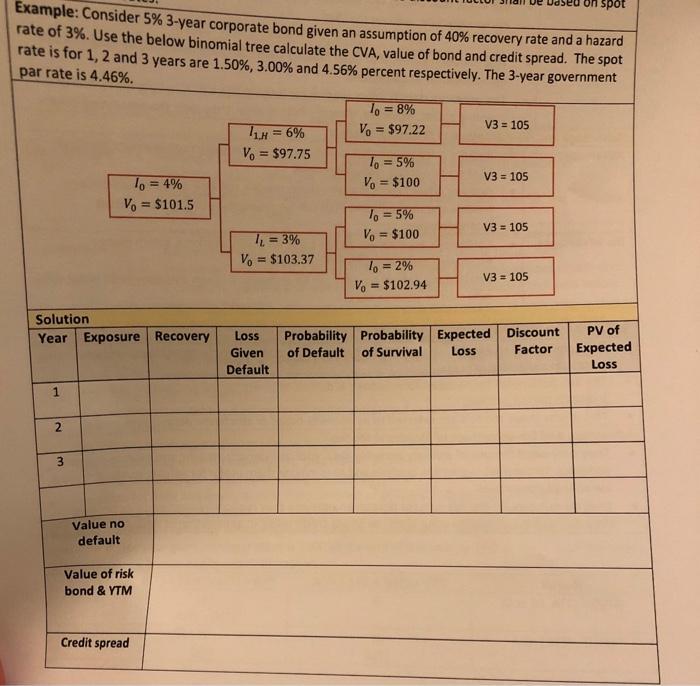

Example: Consider 5% 3-year corporate bond given an assumption of 40% recovery rate and a hazard rate of 3%. Use the below binomial tree

Example: Consider 5% 3-year corporate bond given an assumption of 40% recovery rate and a hazard rate of 3%. Use the below binomial tree calculate the CVA, value of bond and credit spread. The spot rate is for 1, 2 and 3 years are 1.50%, 3.00% and 4.56% percent respectively. The 3-year government par rate is 4.46%. Solution Year Exposure Recovery 1 2 lo = 4% Vo = $101.5 3 Value no default Value of risk bond & YTM Credit spread 11H = 6% Vo = $97.75 1 = 3% Vo = $103.37 Loss Given Default Probability of Default 10 = 8% Vo = $97.22 lo = 5% Vo = $100 10 = 5% Vo = $100 Vo 10 = 2% = $102.94 Probability of Survival V3 = 105 V3 = 105 V3 = 105 V3 = 105 Expected Loss on spot Discount Factor PV of Expected Loss

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fixed Income Securities Valuation Risk and Risk Management

Authors: Pietro Veronesi

1st edition

0470109106, 978-0470109106