Question

Excel Activity: Evaluating Risk and Return Start with the partial model in the file Ch02 P15 Build a Model.xlsx. The file contains data for this

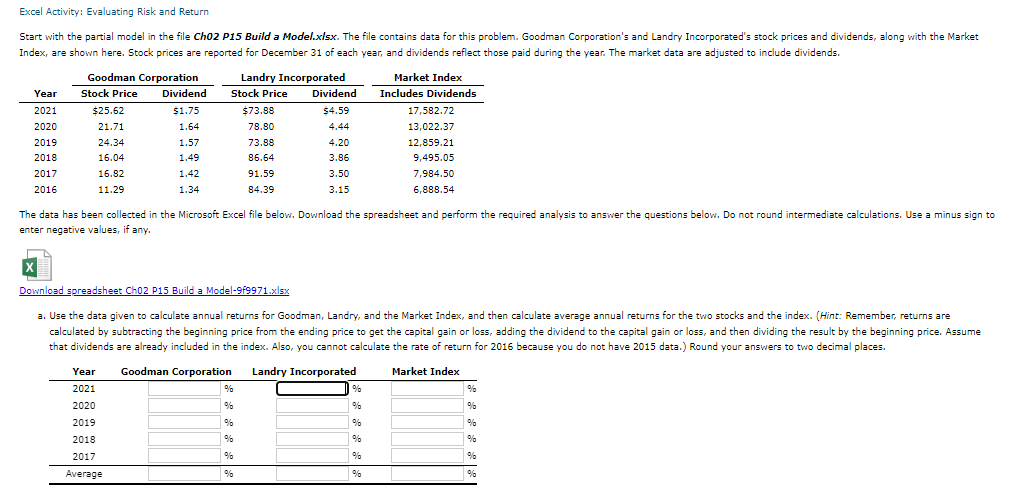

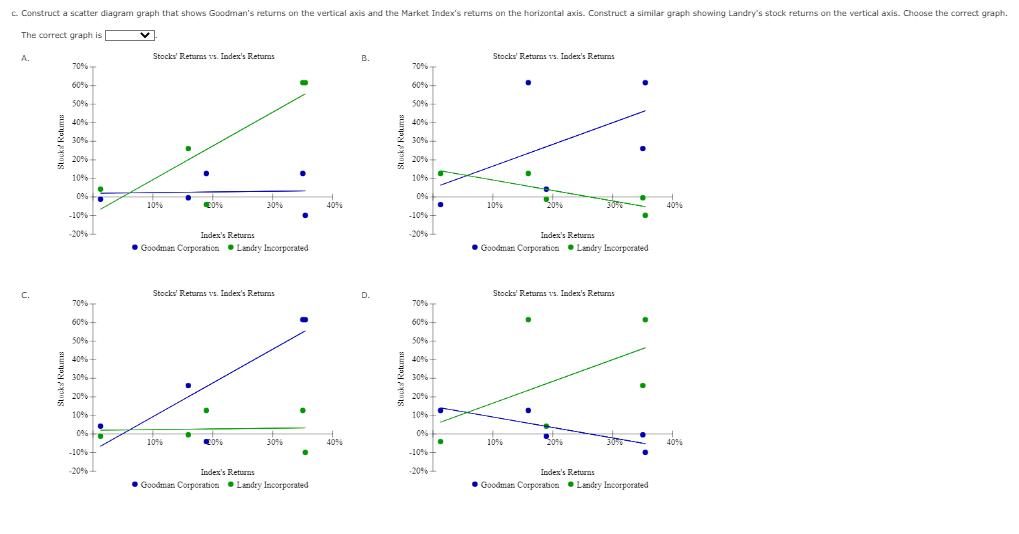

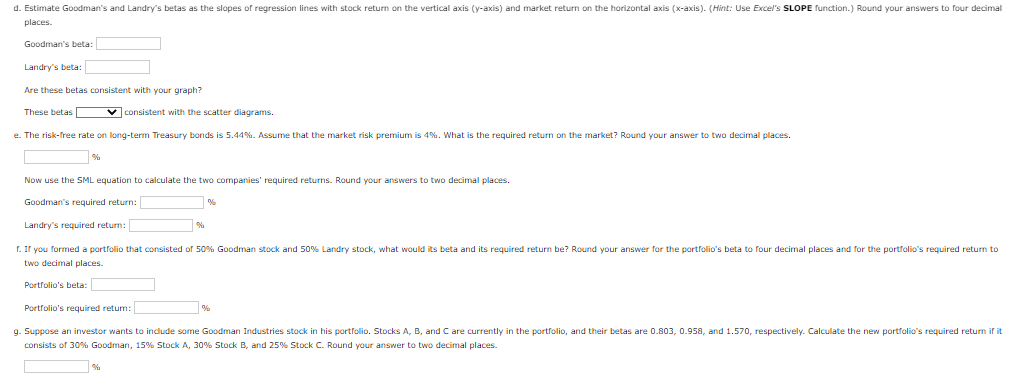

Excel Activity: Evaluating Risk and Return Start with the partial model in the file Ch02 P15 Build a Model.xlsx. The file contains data for this problem. Goodman Corporation's and Landry Incorporated's stock prices and dividends, along with the Market Index, are shown here. Stock prices are reported for December 31 of each year, and dividends reflect those paid during the year. The market data are adjusted to include dividends.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Sm Auditing Integrated Appr Review Copy

Authors: ARENS LO, EBBECKE

7th Edition

0135914396, 978-0135914397