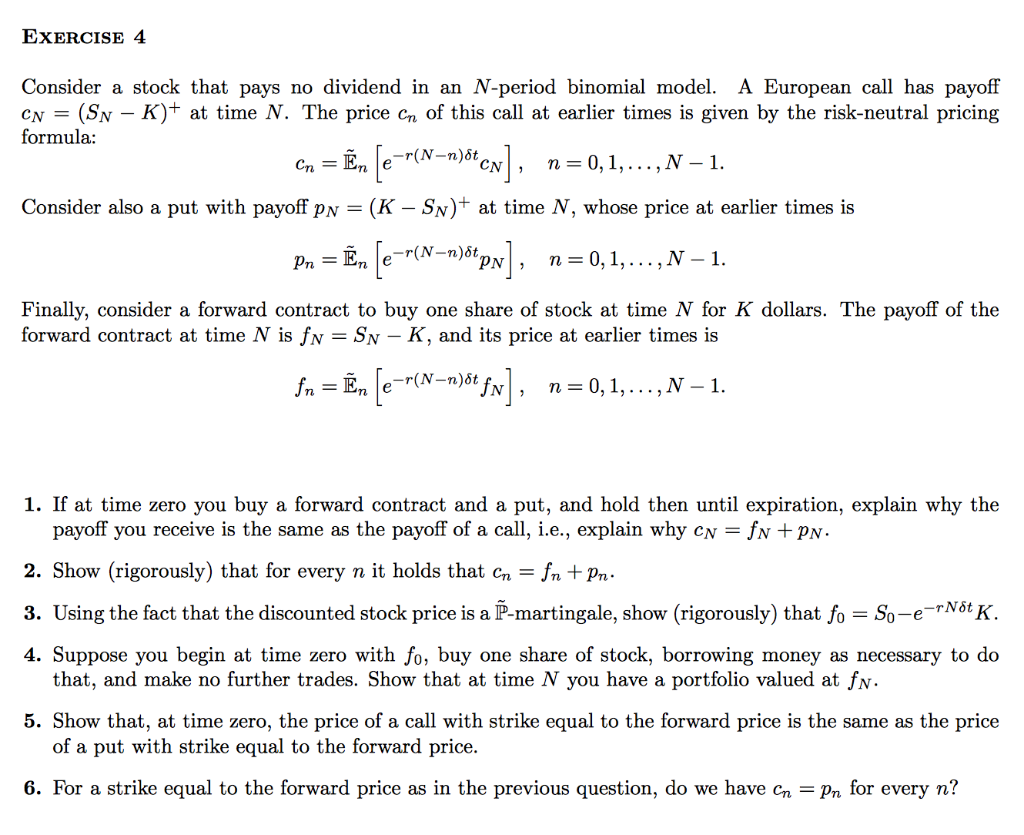

EXERCISE 4 Consider a stock that pays no dividend in an N-period binomial model. A European call has payoff CN = (SN - K)+ at time N. The price Cn of this call at earlier times is given by the risk-neutral pricing formula: en = n [e=r(N=n)sten], n=0,1,..., N 1. Consider also a put with payoff pn = (K Sp)+ at time N, whose price at earlier times is Pn = r [e=(N=n)tpn], n= 0, 1,...,N 1. Finally, consider a forward contract to buy one share of stock at time N for K dollars. The payoff of the forward contract at time N is fn = Sn - K, and its price at earlier times is fn = n le="(N=n)dt fu], n= 0,1, ..., N - 1. 1. If at time zero you buy a forward contract and a put, and hold then until expiration, explain why the payoff you receive is the same as the payoff of a call, i.e., explain why cn = fn + pn. 2. Show (rigorously) that for every n it holds that cn = fn + Pr. 3. Using the fact that the discounted stock price is a P-martingale, show (rigorously) that fo = So-e-rN8tK. 4. Suppose you begin at time zero with fo, buy one share of stock, borrowing money as necessary to do that, and make no further trades. Show that at time N you have a portfolio valued at fn. 5. Show that, at time zero, the price of a call with strike equal to the forward price is the same as the price of a put with strike equal to the forward price. 6. For a strike equal to the forward price as in the previous question, do we have cn = Pn for every n? EXERCISE 4 Consider a stock that pays no dividend in an N-period binomial model. A European call has payoff CN = (SN - K)+ at time N. The price Cn of this call at earlier times is given by the risk-neutral pricing formula: en = n [e=r(N=n)sten], n=0,1,..., N 1. Consider also a put with payoff pn = (K Sp)+ at time N, whose price at earlier times is Pn = r [e=(N=n)tpn], n= 0, 1,...,N 1. Finally, consider a forward contract to buy one share of stock at time N for K dollars. The payoff of the forward contract at time N is fn = Sn - K, and its price at earlier times is fn = n le="(N=n)dt fu], n= 0,1, ..., N - 1. 1. If at time zero you buy a forward contract and a put, and hold then until expiration, explain why the payoff you receive is the same as the payoff of a call, i.e., explain why cn = fn + pn. 2. Show (rigorously) that for every n it holds that cn = fn + Pr. 3. Using the fact that the discounted stock price is a P-martingale, show (rigorously) that fo = So-e-rN8tK. 4. Suppose you begin at time zero with fo, buy one share of stock, borrowing money as necessary to do that, and make no further trades. Show that at time N you have a portfolio valued at fn. 5. Show that, at time zero, the price of a call with strike equal to the forward price is the same as the price of a put with strike equal to the forward price. 6. For a strike equal to the forward price as in the previous question, do we have cn = Pn for every n