Answered step by step

Verified Expert Solution

Question

1 Approved Answer

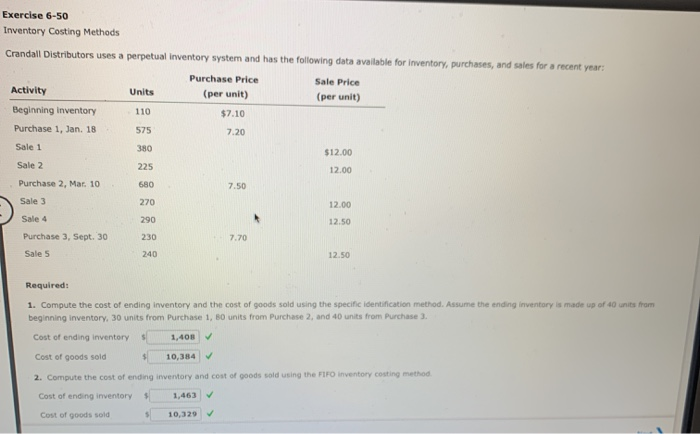

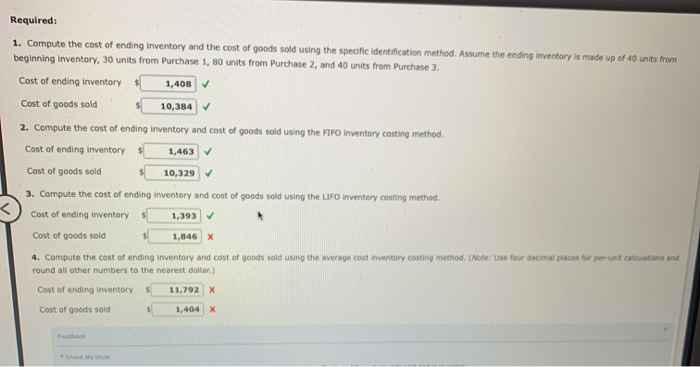

Exercise 6-50 Inventory Costing Methods Crandall Distributors uses a perpetual inventory system and has the following data available for inventory, purchases, and sales for a

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Lean Audit A Detailed User Guide For The Lean Factory Audit Online

Authors: Isaias Wallaker

1st Edition

B09R3HXJ11, 979-8408651320