Answered step by step

Verified Expert Solution

Question

1 Approved Answer

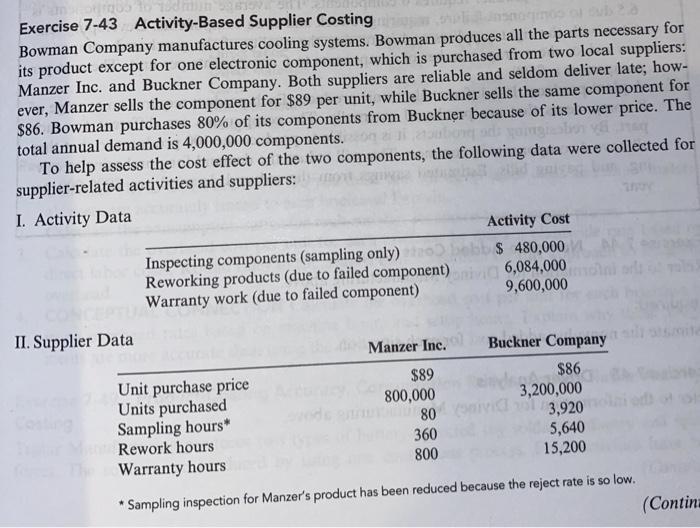

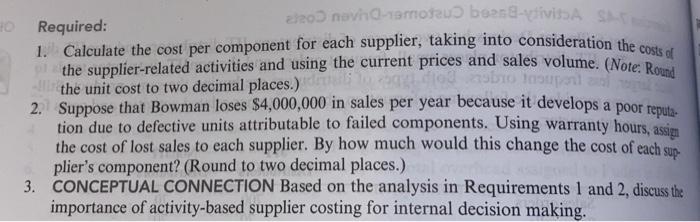

Exercise 7-43 Activity-Based Supplier Costing Bowman Company manufactures cooling systems. Bowman produces all the parts necessary for its product except for one electronic component, which

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Life Audit Journal What Is My Why

Authors: A S

1st Edition

B08F6TXV7Z, 9798672209692