Answered step by step

Verified Expert Solution

Question

1 Approved Answer

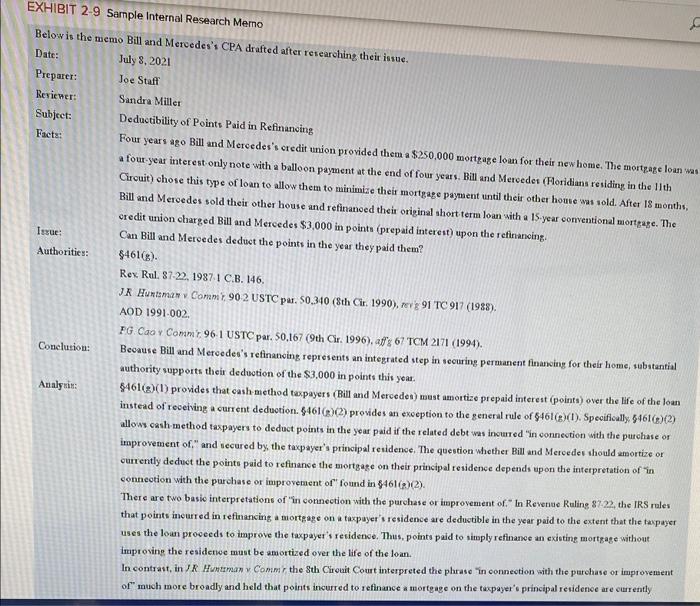

EXHIBIT 2-9 Sample Internal Research Memo Below is the memo Bill and Mercedes's CPA drafted after researching their issue. Date: Preparer: Reviewer: Subject: Facts:

EXHIBIT 2-9 Sample Internal Research Memo Below is the memo Bill and Mercedes's CPA drafted after researching their issue. Date: Preparer: Reviewer: Subject: Facts: July 8, 2021 Joe Staff Sandra Miller Deductibility of Points Paid in Refinancing C Isrue: Authorities: Conclusion: Analysis: Four years ago Bill and Mercedes's credit union provided them a $250,000 mortgage loan for their new home. The mortgage loan was a four-year interest only note with a balloon payment at the end of four years. Bill and Mercedes (Floridians residing in the 11th Circuit) chose this type of loan to allow them to minimize their mortgage payment until their other house was sold. After 18 months, Bill and Mercedes sold their other house and refinanced their original short term loan with a 15-year conventional mortgage. The credit union charged Bill and Mercedes $3,000 in points (prepaid interest) upon the refinancing. Can Bill and Mercedes deduct the points in the year they paid them? $461(g). Rex Rul. 87-22, 1987-1 C.B. 146. JR Huntsman v Comm 90-2 USTC par. 50,340 (8th Cir. 1990), rev 91 TC 917 (1988). AOD 1991-002. PG Cao v Commr. 96-1 USTC par. 50,167 (9th Cir. 1996), affg 67 TCM 2171 (1994). Because Bill and Mercedes's refinancing represents an integrated step in securing permanent financing for their home, substantial authority supports their deduction of the $3,000 in points this year. $461(2)(1) provides that cash-method taxpayers (Bill and Mercedes) must amortize prepaid interest (points) over the life of the loan instead of receiving a current deduction. $461(a)(2) provides an exception to the general rule of 5461(2)(1). Specifically, 5461(e)(2) allows cash-method taxpayers to deduct points in the year paid if the related debt was incurred "in connection with the purchase or improvement of," and secured by, the taxpayer's principal residence. The question whether Bill and Mercedes should amortize or currently deduct the points paid to refinance the mortgage on their principal residence depends upon the interpretation of "in connection with the purchase or improvement of" found in $461(2)(2). There are two basic interpretations of "in connection with the purchase or improvement of." In Revenue Ruling 87-22, the IRS rules that points incurred in refinancing a mortgage on a taxpayer's residence are deductible in the year paid to the extent that the taxpayer uses the loan proceeds to improve the taxpayer's residence. Thus, points paid to simply refinance an existing mortgage without improving the residence must be amortized over the life of the loan. In contrast, in R Huntsman v Commr, the 8th Circuit Court interpreted the phrase "in connection with the purchase or improvement of" much more broadly and held that points incurred to refinance a mortgage on the taxpayer's principal residence are currently

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Survey of Accounting

Authors: Carl S Warren

5th Edition

9780538489737, 538749091, 538489731, 978-0538749091