Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Fenton Ltd is a manufacturing organisation supplying specialised engineered products to a wide range of public and private sector throughout the UK. You are

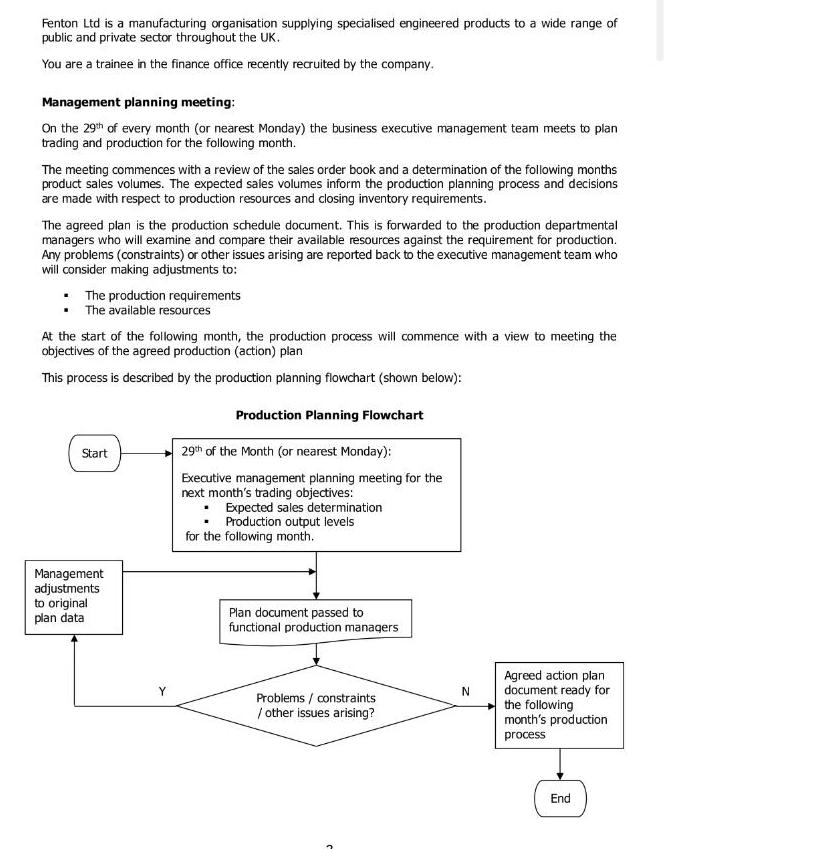

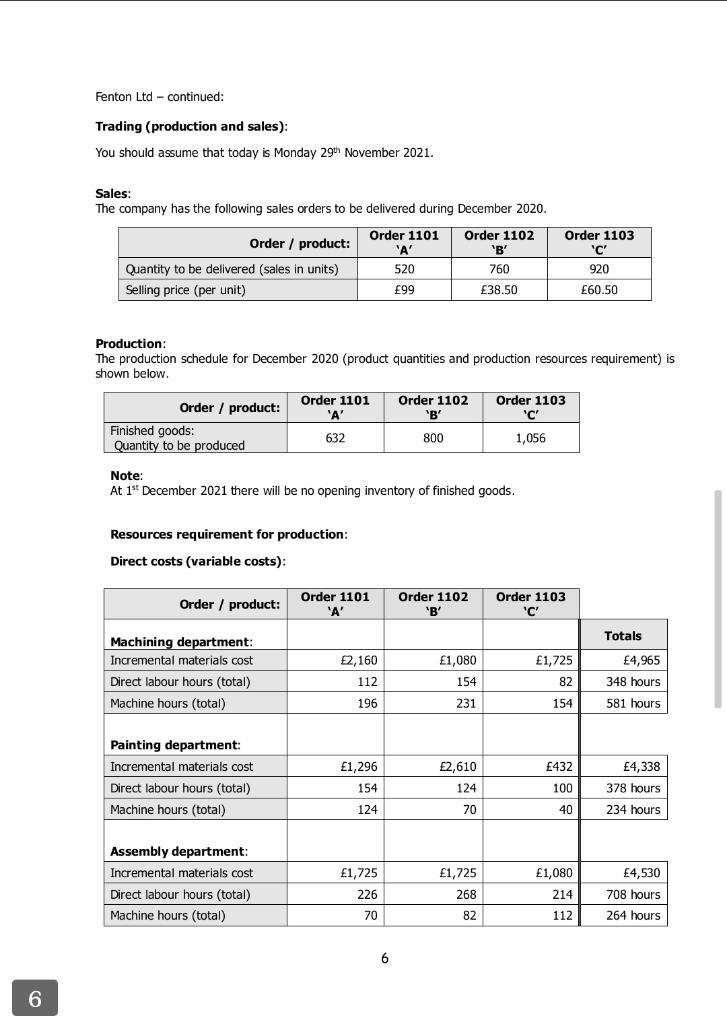

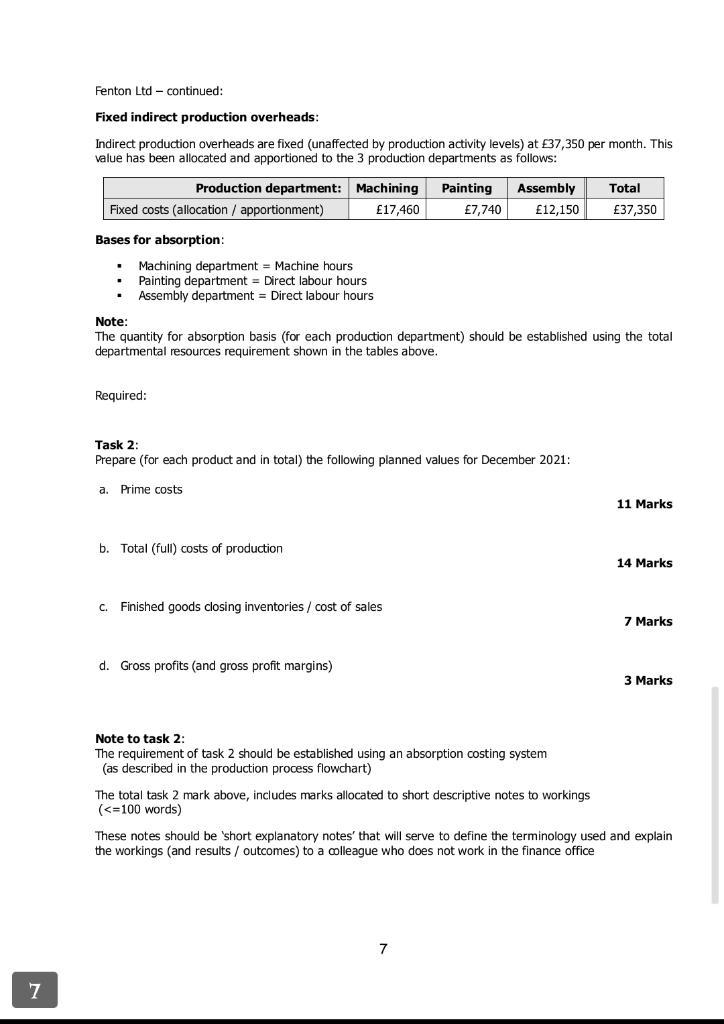

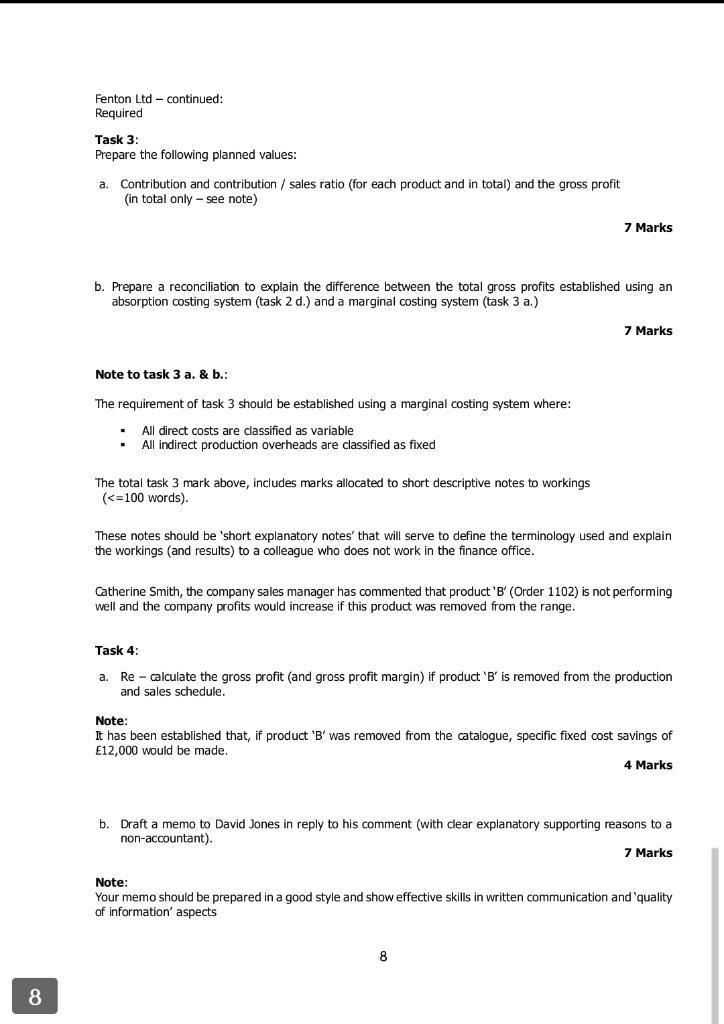

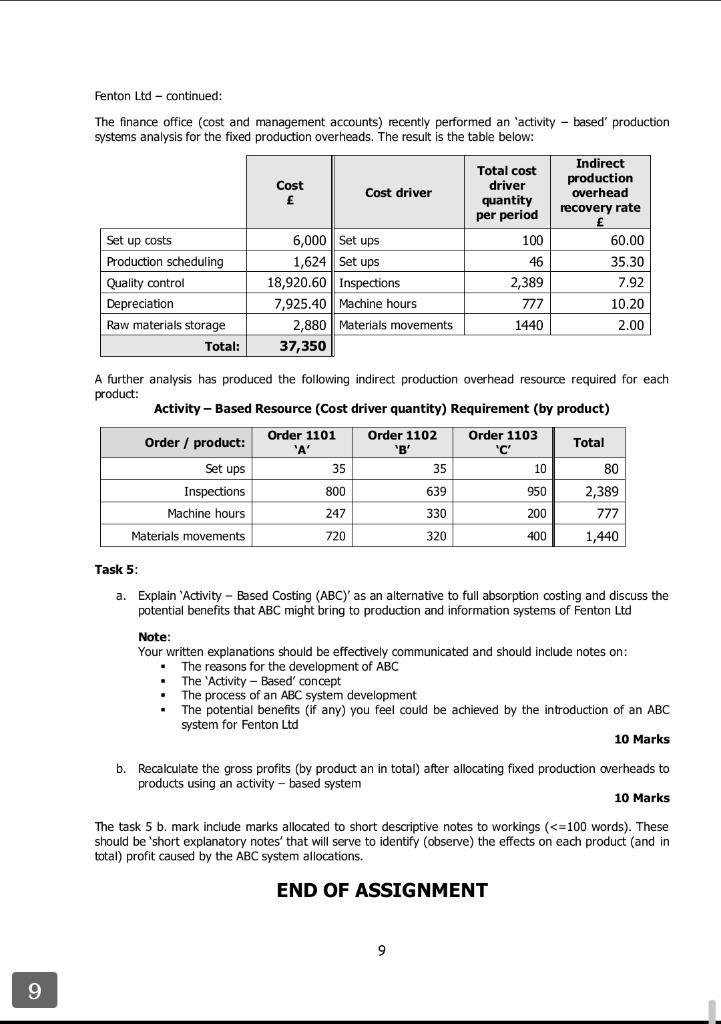

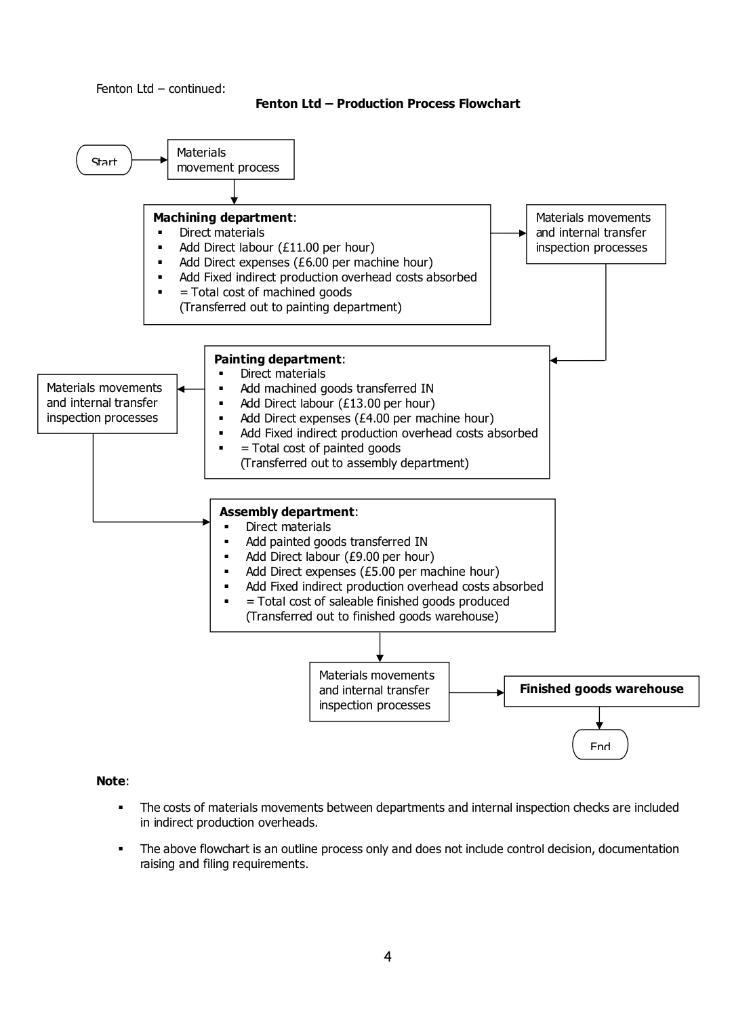

Fenton Ltd is a manufacturing organisation supplying specialised engineered products to a wide range of public and private sector throughout the UK. You are a trainee in the finance office recently recruited by the company. Management planning meeting: On the 29th of every month (or nearest Monday) the business executive management team meets to plan trading and production for the following month. The meeting commences with a review of the sales order book and a determination of the following months product sales volumes. The expected sales volumes inform the production planning process and decisions are made with respect to production resources and closing inventory requirements. The agreed plan is the production schedule document. This is forwarded to the production departmental managers who will examine and compare their available resources against the requirement for production. Any problems (constraints) or other issues arising are reported back to the executive management team who will consider making adjustments to: . The production requirements The available resources At the start of the following month, the production process will commence with a view to meeting the objectives of the agreed production (action) plan This process is described by the production planning flowchart (shown below): Production Planning Flowchart Start Management adjustments to original plan data 29th of the Month (or nearest Monday): Executive management planning meeting for the next month's trading objectives: Expected sales determination Production output levels for the following month. Plan document passed to functional production managers Problems / constraints / other issues arising? N Agreed action plan document ready for the following month's production process End 3 Fenton Ltd - continued: The production process: The production process of Fenton Ltd takes place through 3 production departments: machining, painting and assembly. Machining department: Direct materials are transferred from the direct materials stores to the machining department. These are transformed using direct labour employees and machine processes into machined goods. The total of the prime costs add the fixed production overhead (allocated and / or apportioned) is the total cost of machined goods transferred to the painting department. For the machining department, the direct labour employees are paid at a rate of 11.00 per hour and the variable machine cost is 6.00. Painting department: Incremental direct materials are transferred from the direct materials stores to the painting department. These are combined with the machined goods transferred in and are transformed using direct labour employees and machine processes into painted goods. The total combined costs add the fixed production overhead (allocated and / or apportioned) is the total cost of painted goods transferred to the assembly department. For the painting department, the direct labour employees are paid at a rate of 13.00 per hour and the variable machine cost is 4.00. Assembly department: Incremental direct materials and components are transferred from the direct materials stores to the assembly department. These are combined with the painted goods transferred in and are transformed using direct labour employees and machine processes into saleable finished goods. The total combined costs add the fixed production overhead (allocated and / or apportioned) is the total cost of the saleable finished goods transferred to the finished goods warehouse. For the assembly department, the direct labour employees are paid at a rate of 9.00 per hour and the variable machine cost is 5.00. The production process is described in the production process flowchart below: 3 5 Fenton Ltd continued: Goods receiving and locating / storage control process: When goods are received to the business raw materials stores, they are first checked by the store keeper for quantity against a copy of the original purchase order document (this is forwarded to the raw materials stores at the time that the order is placed with all money values removed). If the quantity is incorrect (allowing for approved part-order deliveries) a 'Quantity rejection note' is prepared. Goods that are acceptable by quantity are quality inspected for size, weight, colour etc. Where goods are found to be unacceptable by quality, a 'Quality rejection note' is prepared. Goods rejected by quantity or quality are located at the 'Returns room' ready for return to the supplier. Acceptable goods are initially identified as either 'Alpha' or 'Beta'. Alpha: . Beta: Alphas that are 'Square' are to be located at 'A01' If the Alphas are not 'Square' are 'Round'. 'Round' Alphas are further sub-analysed as 'Clear' or 'Opaque'. Alphas that are 'Clear' should be located at 'A02'; otherwise the Opaque' Alphas should be located at 'A03'. Betas that are 'Pentagon' should be located at 'B01' Betas that are not 'Pentagon' are 'Hexagon'. 'Hexagon' Betas are further sub-analysed as either 'Large' or 'Small'. Large Betas' should be located at 'B02'; otherwise the 'Small Betas' are to be located at 'B03'. After goods received have carefully and accurately been located, the store keeper will prepare a 'goods received note' (GRN). This will be forwarded to the finance office. Required: Task 1: Prepare a flowchart in a A4 size paper (one side only) to describe the goods receiving and locating / storage control process. Note: Your flowchart should be prepared in a good style using the Microsoft Office Word: 'Insert / Shapes / Flowchart facility (Maximum 20 marks including 6 marks credit for software use, good style and clear presentation). 5 20 Marks 6 Fenton Ltd continued: Trading (production and sales): You should assume that today is Monday 29th November 2021. Sales: The company has the following sales orders to be delivered during December 2020. Order product: Quantity to be delivered (sales in units) Selling price (per unit) Order product: Finished goods: Quantity to be produced Production: The production schedule for December 2020 (product quantities and production resources requirement) is shown below. Resources requirement for production: Direct costs (variable costs): Order / product: Machining department: Incremental materials cost Direct labour hours (total) Machine hours (total) Note: At 1st December 2021 there will be no opening inventory of finished goods. Painting department: Incremental materials cost Direct labour hours (total) Machine hours (total) Order 1101 'A' 520 99 Order 1101 'A' 632 Assembly department: Incremental materials cost Direct labour hours (total) Machine hours (total) Order 1101 'A' 2,160 112 196 1,296 154 124 Order 1102 'B' 760 38.50 1,725 226 70 6 Order 1102 Order 1103 'B' 'C' 800 1,056 Order 1102 'B' 1,080 154 231 Order 1103 'C' 920 60.50 2,610 124 70 1,725 268 82 Order 1103 'C' 1,725 82 154 432 100 40 1,080 214 112 Totals 4,965 348 hours 581 hours. 4,338 378 hours 234 hours 4,530 708 hours 264 hours 7 Fenton Ltd continued: Fixed indirect production overheads: Indirect production overheads are fixed (unaffected by production activity levels) at 37,350 per month. This value has been allocated and apportioned to the 3 production departments as follows: Fixed costs (allocation / apportionment) Bases for absorption: . Production department: Machining 17,460 Machining department Machine hours Painting department = Direct labour hours Assembly department Direct labour hours Required: a. Prime costs Note: The quantity for absorption basis (for each production department) should be established using the total departmental resources requirement shown in the tables above. b. Total (full) costs of production Task 2: Prepare (for each product and in total) the following planned values for December 2021: c. Finished goods closing inventories/ cost of sales Painting d. Gross profits (and gross profit margins) 7,740 Total Assembly 12,150 37,350 Note to task 2: The requirement of task 2 should be established using an absorption costing system (as described in the production process flowchart) 7 The total task 2 mark above, includes marks allocated to short descriptive notes to workings ( 8 Fenton Ltd continued: Required Task 3: Prepare the following planned values: a. Contribution and contribution / sales ratio (for each product and in total) and the gross profit (in total only see note) b. Prepare reconciliation to explain the difference between the total gross profits established using an absorption costing system (task 2 d.) and a marginal costing system (task 3 a.) Note to task 3 a. & b.:: The requirement of task 3 should be established using a marginal costing system where: All direct costs are classified as variable All indirect production overheads are classified as fixed . The total task 3 mark above, includes marks allocated to short descriptive notes to workings ( 9 Fenton Ltd - continued: The finance office (cost and management accounts) recently performed an 'activity based production systems analysis for the fixed production overheads. The result is the table below: Set up costs. Production scheduling Quality control Depreciation Raw materials storage Total: Task 5: a. Order / product: Set ups Inspections Machine hours Materials movements Cost Cost driver 6,000 Set ups 1,624 Set ups . 18,920.60 Inspections 7,925.40 Machine hours 2,880 Materials movements 37,350 35 800 247 720 Total cost driver quantity per period A further analysis has produced the following indirect production overhead resource required for each product: 100 46 Activity-Based Resource (Cost driver quantity) Requirement (by product) Order 1101 Order 1102 Order 1103 'A' 'B' 'C' 35 639 330 320 2,389 777 1440 Indirect production overhead 9 recovery rate 10 950 200 400 60.00 35.30 7.92 10.20 2.00 Total Explain 'Activity - Based Costing (ABC)' as an alternative to full absorption costing and discuss the potential benefits that ABC might bring to production and information systems of Fenton Ltd 80 2,389 777 1,440 Note: Your written explanations should be effectively communicated and should include notes on: The reasons for the development of ABC The 'Activity Based' concept The process of an ABC system development The potential benefits (if any) you feel could be achieved by the introduction of an ABC system for Fenton Ltd 10 Marks b. Recalculate the gross profits (by product an in total) after allocating fixed production overheads to products using an activity-based system 10 Marks The task 5 b. mark include marks allocated to short descriptive notes to workings ( Fenton Ltd - continued: Start Materials movements and internal transfer inspection processes Note: . Fenton Ltd - Production Process Flowchart Materials movement process Machining department: Direct materials Add Direct labour (11.00 per hour) Add Direct expenses (6.00 per machine hour) Add Fixed indirect production overhead costs absorbed = Total cost of machined goods (Transferred out to painting department) Painting department: Direct materials . Materials movements and internal transfer inspection processes Add machined goods transferred IN Add Direct labour (13.00 per hour) Add Direct expenses (4.00 per machine hour) Add Fixed indirect production overhead costs absorbed = Total cost painted goods (Transferred to assembly department) Assembly department: Direct materials Add painted goods transferred IN Add Direct labour (9.00 per hour) Add Direct expenses (5.00 per machine hour) Add Fixed indirect production overhead costs absorbed = Total cost of saleable finished goods produced (Transferred out to finished goods warehouse) Materials movements and internal transfer inspection processes Finished goods warehouse Fnd The costs of materials movements between departments and internal inspection checks are included in indirect production overheads. The above flowchart is an outline process only and does not include control decision, documentation raising and filing requirements.

Step by Step Solution

★★★★★

3.57 Rating (164 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Business Analytics Methods Models And Decisions

Authors: James R. Evans

2nd Edition

321997824, 978-1119298588, 978-0321997821