Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Financial Statements include balance sheet, income statement, statement of stockholders equity, 2021 Transactions 1. During 2021, a new gift card program was started and customers

Financial Statements include balance sheet, income statement, statement of stockholders equity,

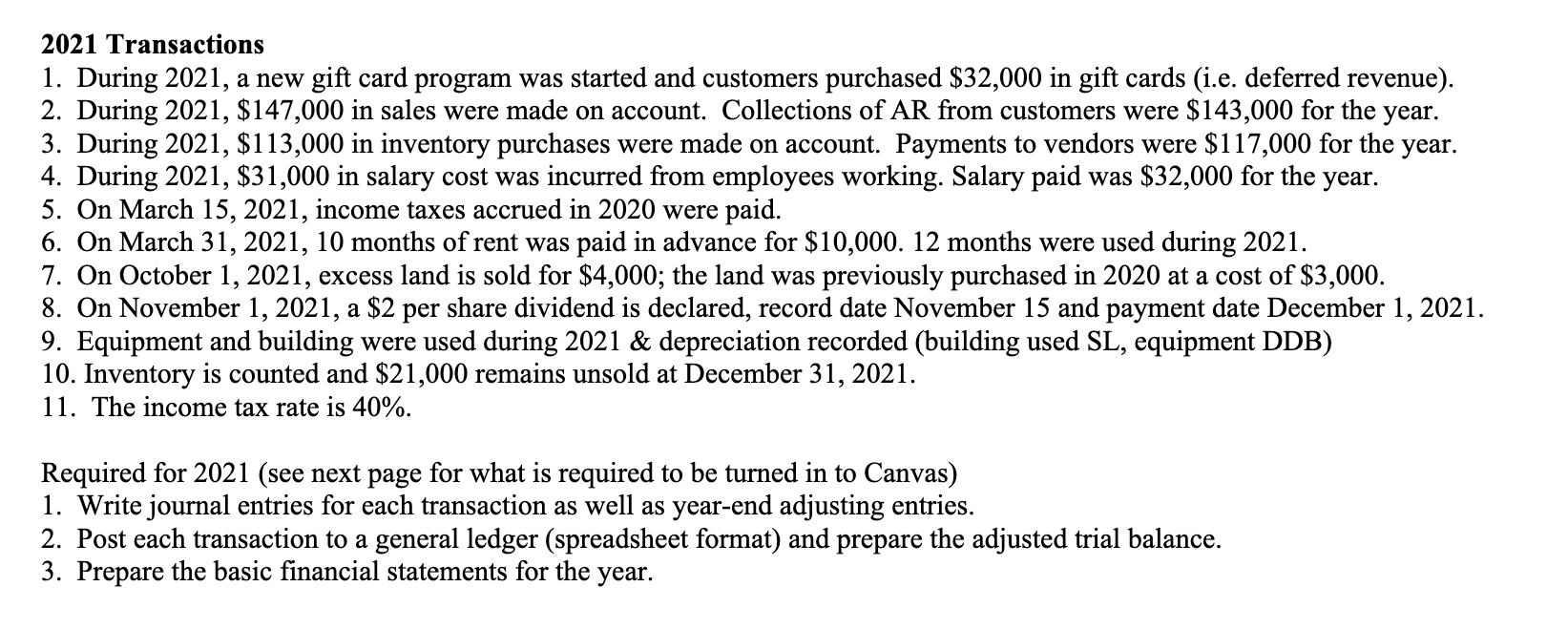

2021 Transactions 1. During 2021, a new gift card program was started and customers purchased $32,000 in gift cards (i.e. deferred revenue). 2. During 2021, $147,000 in sales were made on account. Collections of AR from customers were $143,000 for the year. 3. During 2021, $113,000 in inventory purchases were made on account. Payments to vendors were $117,000 for the year. 4. During 2021, $31,000 in salary cost was incurred from employees working. Salary paid was $32,000 for the year. 5. On March 15, 2021, income taxes accrued in 2020 were paid. 6. On March 31, 2021, 10 months of rent was paid in advance for $10,000.12 months were used during 2021. 7. On October 1, 2021, excess land is sold for $4,000; the land was previously purchased in 2020 at a cost of $3,000. 8. On November 1, 2021, a $2 per share dividend is declared, record date November 15 and payment date December 1,2021. 9. Equipment and building were used during 2021& depreciation recorded (building used SL, equipment DDB) 10. Inventory is counted and $21,000 remains unsold at December 31, 2021. 11. The income tax rate is 40%. Required for 2021 (see next page for what is required to be turned in to Canvas) 1. Write journal entries for each transaction as well as year-end adjusting entries. 2. Post each transaction to a general ledger (spreadsheet format) and prepare the adjusted trial balance. 3. Prepare the basic financial statements for the year. 2021 Transactions 1. During 2021, a new gift card program was started and customers purchased $32,000 in gift cards (i.e. deferred revenue). 2. During 2021, $147,000 in sales were made on account. Collections of AR from customers were $143,000 for the year. 3. During 2021, $113,000 in inventory purchases were made on account. Payments to vendors were $117,000 for the year. 4. During 2021, $31,000 in salary cost was incurred from employees working. Salary paid was $32,000 for the year. 5. On March 15, 2021, income taxes accrued in 2020 were paid. 6. On March 31, 2021, 10 months of rent was paid in advance for $10,000.12 months were used during 2021. 7. On October 1, 2021, excess land is sold for $4,000; the land was previously purchased in 2020 at a cost of $3,000. 8. On November 1, 2021, a $2 per share dividend is declared, record date November 15 and payment date December 1,2021. 9. Equipment and building were used during 2021& depreciation recorded (building used SL, equipment DDB) 10. Inventory is counted and $21,000 remains unsold at December 31, 2021. 11. The income tax rate is 40%. Required for 2021 (see next page for what is required to be turned in to Canvas) 1. Write journal entries for each transaction as well as year-end adjusting entries. 2. Post each transaction to a general ledger (spreadsheet format) and prepare the adjusted trial balance. 3. Prepare the basic financial statements for the yearStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Acca F7 Financial Reporting Practice And Revision Kit

Authors: BPP Learning Media

1st Edition

1472726898, 978-1472726896