Answered step by step

Verified Expert Solution

Question

1 Approved Answer

find the beta of each stock with respect to the market portfolio, respectively. Suppose the market portfolio consists of weights wa= 0.3,08 = 0.5 0c=0.2.

find the beta of each stock with respect to the market portfolio, respectively.

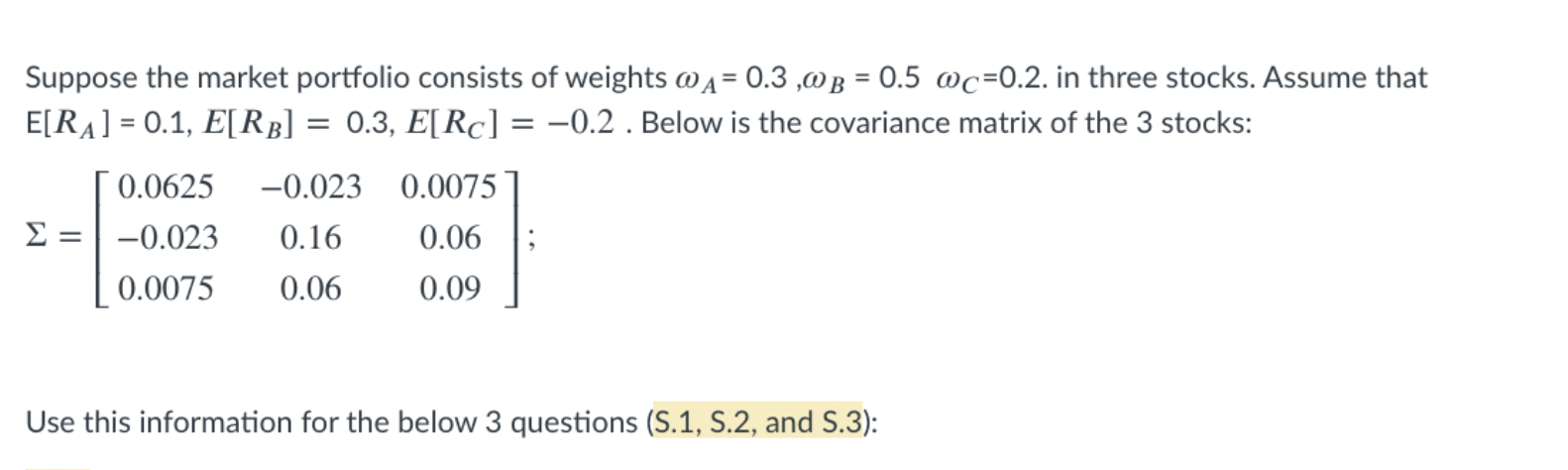

Suppose the market portfolio consists of weights wa= 0.3,08 = 0.5 0c=0.2. in three stocks. Assume that E[RA] = 0.1, E[RB] = 0.3, E[RC] = -0.2 . Below is the covariance matrix of the 3 stocks: 0.0625 -0.023 = -0.023 0.0075 0.16 0.06 0.06 0.09 0.0075 Use this information for the below 3 questions (S.1, S.2, and S.3): Suppose the market portfolio consists of weights wa= 0.3,08 = 0.5 0c=0.2. in three stocks. Assume that E[RA] = 0.1, E[RB] = 0.3, E[RC] = -0.2 . Below is the covariance matrix of the 3 stocks: 0.0625 -0.023 = -0.023 0.0075 0.16 0.06 0.06 0.09 0.0075 Use this information for the below 3 questions (S.1, S.2, and S.3)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Venture capital and the finance of innovation

Authors: Andrew Metrick

2nd Edition

9781118137888, 470454709, 1118137884, 978-0470454701