Answered step by step

Verified Expert Solution

Question

1 Approved Answer

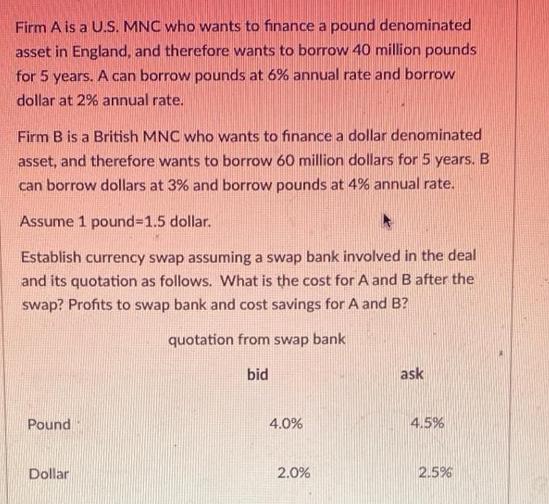

Firm A is a U.S. MNC who wants to finance a pound denominated asset in England, and therefore wants to borrow 40 million pounds

Firm A is a U.S. MNC who wants to finance a pound denominated asset in England, and therefore wants to borrow 40 million pounds for 5 years. A can borrow pounds at 6% annual rate and borrow dollar at 2% annual rate. Firm B is a British MNC who wants to finance a dollar denominated asset, and therefore wants to borrow 60 million dollars for 5 years. B can borrow dollars at 3% and borrow pounds at 4% annual rate. Assume 1 pound=1.5 dollar. Establish currency swap assuming a swap bank involved in the deal and its quotation as follows. What is the cost for A and B after the swap? Profits to swap bank and cost savings for A and B? quotation from swap bank Pound bid ask 4.0% 4.5% Dollar 2.0% 2.5%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Currency Swap Analysis This scenario presents a perfect opportunity for a currency swap to benefit both Firm A and Firm B Heres a breakdown of the sit...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Global Strategy

Authors: Mike W. Peng

5th Edition

0357512367, 978-0357512364