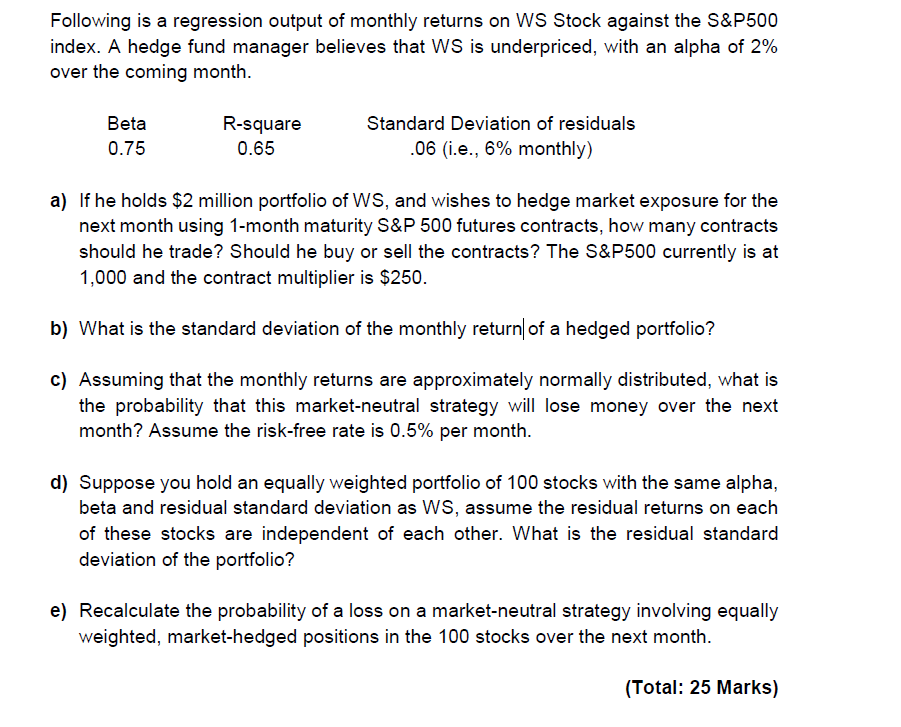

Following is a regression output of monthly returns on WS Stock against the S\&P500 index. A hedge fund manager believes that WS is underpriced, with an alpha of 2% over the coming month. a) If he holds $2 million portfolio of WS, and wishes to hedge market exposure for the next month using 1-month maturity S\&P 500 futures contracts, how many contracts should he trade? Should he buy or sell the contracts? The S\&P500 currently is at 1,000 and the contract multiplier is $250. b) What is the standard deviation of the monthly return| of a hedged portfolio? c) Assuming that the monthly returns are approximately normally distributed, what is the probability that this market-neutral strategy will lose money over the next month? Assume the risk-free rate is 0.5% per month. d) Suppose you hold an equally weighted portfolio of 100 stocks with the same alpha, beta and residual standard deviation as WS, assume the residual returns on each of these stocks are independent of each other. What is the residual standard deviation of the portfolio? e) Recalculate the probability of a loss on a market-neutral strategy involving equally weighted, market-hedged positions in the 100 stocks over the next month. (Total: 25 Marks) Following is a regression output of monthly returns on WS Stock against the S\&P500 index. A hedge fund manager believes that WS is underpriced, with an alpha of 2% over the coming month. a) If he holds $2 million portfolio of WS, and wishes to hedge market exposure for the next month using 1-month maturity S\&P 500 futures contracts, how many contracts should he trade? Should he buy or sell the contracts? The S\&P500 currently is at 1,000 and the contract multiplier is $250. b) What is the standard deviation of the monthly return| of a hedged portfolio? c) Assuming that the monthly returns are approximately normally distributed, what is the probability that this market-neutral strategy will lose money over the next month? Assume the risk-free rate is 0.5% per month. d) Suppose you hold an equally weighted portfolio of 100 stocks with the same alpha, beta and residual standard deviation as WS, assume the residual returns on each of these stocks are independent of each other. What is the residual standard deviation of the portfolio? e) Recalculate the probability of a loss on a market-neutral strategy involving equally weighted, market-hedged positions in the 100 stocks over the next month. (Total: 25 Marks)