Answered step by step

Verified Expert Solution

Question

1 Approved Answer

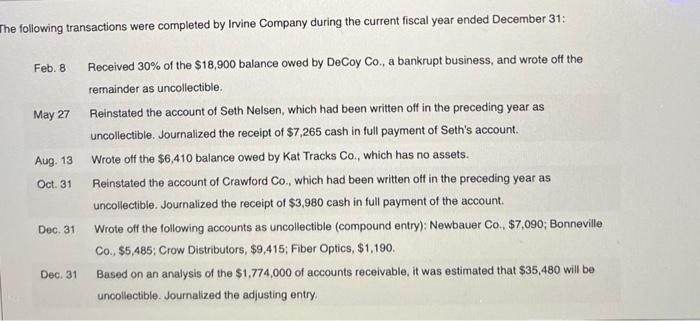

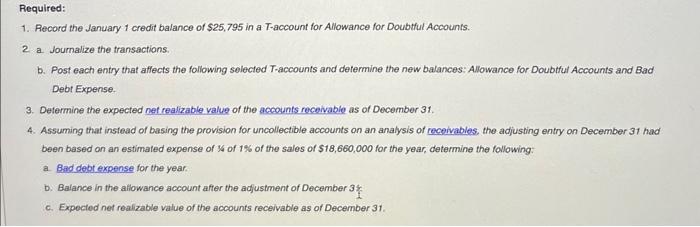

following transactions were completed by Irvine Company during the current fiscal year ended December 31: Feb. 8 Received 30% of the $18,900 balance owed by

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managing The Audit Function A Corporate Audit Department Procedures Guide

Authors: Michael P. Cangemi, Tommie W. Singleton

3rd Edition

0471281190, 978-0471281191