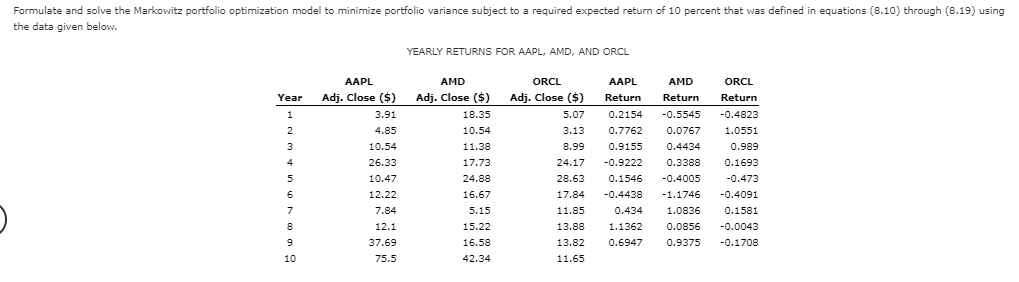

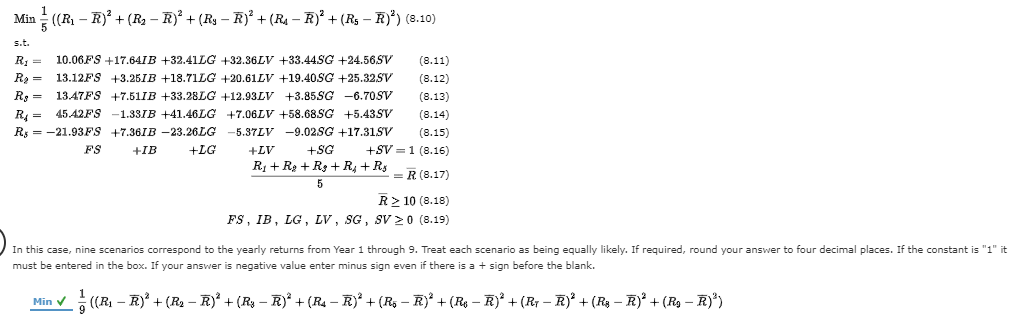

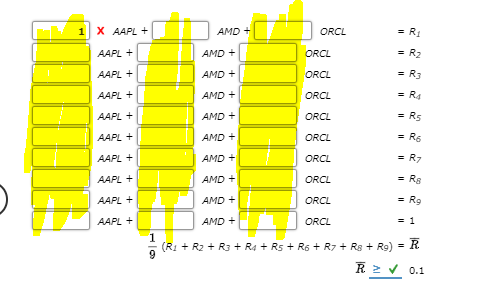

Formulate and solve the Markowitz portfolio optimization model to minimize portfolio variance subject to a required expected return of 10 percent that was defined in equations (8.10) through (8.19) using the data given below. YEARLY RETURNS FOR AAPL, AMD, AND ORCL ORCL AMD Return Year 1 2 3 4 AAPL AMD ORCL Adj. Close($) Adj. Close($) Adj. Close ($) 3.91 18.35 5.07 4.85 10.54 3.13 10 40 10.54 11.38 8.99 26.33 42 17.73 24.17 10.47 24.88 28.63 4202 12.22 16.67 17.84 7.84 5.15 11.85 1932 1900 12.1 15.22 13.88 37.69 16.58 13.82 75.5 42.34 11.65 AAPL Return 0.2154 0.7762 0.9155 -0.9222 0.1546 1400 -0.4438 0.434 1.1362 0.6947 Return 2002 -0.4823 1.0551 0.989 150 0.1693 24 -0.473 -0.4091 0.1581 -0.5545 0.0767 0.4434 0.3388 -0.4005 -1.1746 1.0836 0.0856 0.9375 5 6 7 8 -0.0043 -0.1708 10 Min ((R R)* +(R2 R)* + (R3 R5 + (R4 R)? + (R3 R)) (8.10) s.t. R = 10.06F9 +17.641B +32.41LG +32.36LV +33.445G +24.56SV (8.11) R2 = 13.12FS +3.251B +18.71LG +20.61LV +19.40SG +25.32SV (8.12) Rg = 13.47FS +7.511 B +33.28LG +12.93LV +3.85 SG -6.70 SV (8.13) R = 45.42FS -1.331B +41.46LG +7.06LV +58.68.SG +5.43SV (8.14) Rs = -21.93 FS +7.361B-23.26LG -5.37LV -9.02SG +17.31SV (8.15) FS +IB +LG +LV +SG +SV = 1 (8.16) R1 + R+R$ +R, +Ry = R(8.17) 5 R > 10 (8.18) FS, IB, LG, LV, SG, SV 20 (8.19) In this case, nine scenarios correspond to the yearly returns from Year 1 through 9. Treat each scenario as being equally likely. If required, round your answer to four decimal places. If the constant is "1" it must be entered in the box. If your answer is negative value enter minus sign even if there is a + sign before the blank. Min - ((R3 R)* + (R2 R) + (Ry R)* + (Re R) + (RO R)* + (Rev R)* + (R1 R)* + (R$ R) + (R9 R)) 1 X AAPL + AMD + ORCL SRI AAPL + AMD + ORCL = R2 AAPL + AMD + ORCL = R3 AAPL + AMD + ORCL = R4 AAPL + AMD + ORCL S RS AAPL + AMD + ORCL R6 AAPL + AMD + ORCL R7 AAPL + AMD + ORCL SRS AAPL + AMD + ORCL s R9 AAPL + AMD + ORCL = 1 1 lo (R1 + R2 + R3 + Ra + Rs + R6 + R2 + R$ + R9) = R. R> 0.1 The optimal solution to this model is: (If required, round your answer to four decimal places. If your answer is zero, enter "0" and for subtractive or negative numbers use a minus sign even if there is a + sign before the blank.) Variable Value Reduced Cost 1 X R1 R R2 R3 R4 RS R6 R RS R9 AAPL AMD ORCL Formulate and solve the Markowitz portfolio optimization model to minimize portfolio variance subject to a required expected return of 10 percent that was defined in equations (8.10) through (8.19) using the data given below. YEARLY RETURNS FOR AAPL, AMD, AND ORCL ORCL AMD Return Year 1 2 3 4 AAPL AMD ORCL Adj. Close($) Adj. Close($) Adj. Close ($) 3.91 18.35 5.07 4.85 10.54 3.13 10 40 10.54 11.38 8.99 26.33 42 17.73 24.17 10.47 24.88 28.63 4202 12.22 16.67 17.84 7.84 5.15 11.85 1932 1900 12.1 15.22 13.88 37.69 16.58 13.82 75.5 42.34 11.65 AAPL Return 0.2154 0.7762 0.9155 -0.9222 0.1546 1400 -0.4438 0.434 1.1362 0.6947 Return 2002 -0.4823 1.0551 0.989 150 0.1693 24 -0.473 -0.4091 0.1581 -0.5545 0.0767 0.4434 0.3388 -0.4005 -1.1746 1.0836 0.0856 0.9375 5 6 7 8 -0.0043 -0.1708 10 Min ((R R)* +(R2 R)* + (R3 R5 + (R4 R)? + (R3 R)) (8.10) s.t. R = 10.06F9 +17.641B +32.41LG +32.36LV +33.445G +24.56SV (8.11) R2 = 13.12FS +3.251B +18.71LG +20.61LV +19.40SG +25.32SV (8.12) Rg = 13.47FS +7.511 B +33.28LG +12.93LV +3.85 SG -6.70 SV (8.13) R = 45.42FS -1.331B +41.46LG +7.06LV +58.68.SG +5.43SV (8.14) Rs = -21.93 FS +7.361B-23.26LG -5.37LV -9.02SG +17.31SV (8.15) FS +IB +LG +LV +SG +SV = 1 (8.16) R1 + R+R$ +R, +Ry = R(8.17) 5 R > 10 (8.18) FS, IB, LG, LV, SG, SV 20 (8.19) In this case, nine scenarios correspond to the yearly returns from Year 1 through 9. Treat each scenario as being equally likely. If required, round your answer to four decimal places. If the constant is "1" it must be entered in the box. If your answer is negative value enter minus sign even if there is a + sign before the blank. Min - ((R3 R)* + (R2 R) + (Ry R)* + (Re R) + (RO R)* + (Rev R)* + (R1 R)* + (R$ R) + (R9 R)) 1 X AAPL + AMD + ORCL SRI AAPL + AMD + ORCL = R2 AAPL + AMD + ORCL = R3 AAPL + AMD + ORCL = R4 AAPL + AMD + ORCL S RS AAPL + AMD + ORCL R6 AAPL + AMD + ORCL R7 AAPL + AMD + ORCL SRS AAPL + AMD + ORCL s R9 AAPL + AMD + ORCL = 1 1 lo (R1 + R2 + R3 + Ra + Rs + R6 + R2 + R$ + R9) = R. R> 0.1 The optimal solution to this model is: (If required, round your answer to four decimal places. If your answer is zero, enter "0" and for subtractive or negative numbers use a minus sign even if there is a + sign before the blank.) Variable Value Reduced Cost 1 X R1 R R2 R3 R4 RS R6 R RS R9 AAPL AMD ORCL