Question

Forward Interest Rates --- According to the pure expectations theory of interest rates, how much do you expect to pay for a one-year STRIPS on

Forward Interest Rates --- According to the pure expectations theory of interest rates, how much do you expect to pay for a one-year STRIPS on February 15, 2011? What is the corresponding implied forward rate? How does your answer compare to the current yield on a one-year STRIPS? What does this tell you about the relationship between implied forward rates, the shape of the zero coupon yield curve, and market expectations about future spot interest rates? Please show all equations.

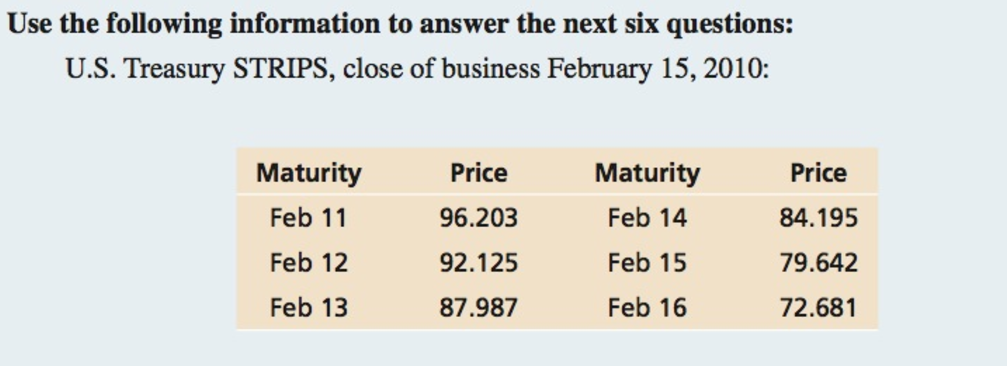

Use the following information to answer the next six questions: U.S. Treasury STRIPS, close of business February 15, 2010: Maturity Maturity Price Price Feb 14 Feb 11 96.203 84.195 Feb 15 79.642 Feb 12 92.125 Feb 13 Feb 16 72.681 87.987Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Structured Finance And Insurance

Authors: Christopher L. Culp

2nd Edition

0471706310, 978-0471706311