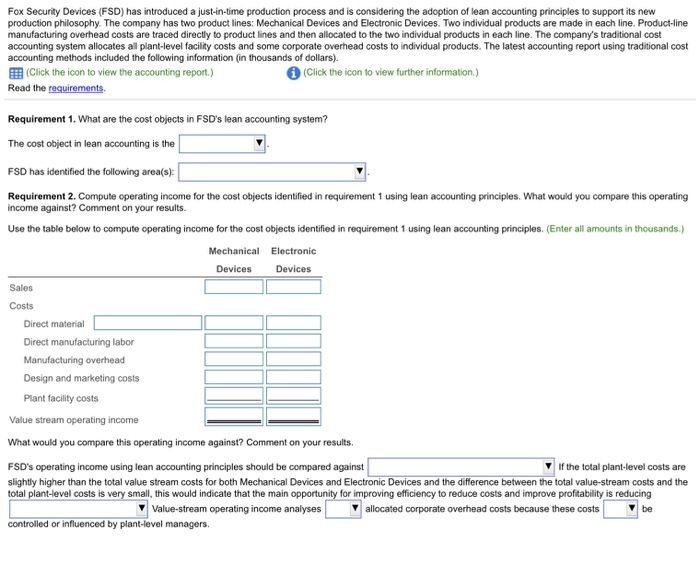

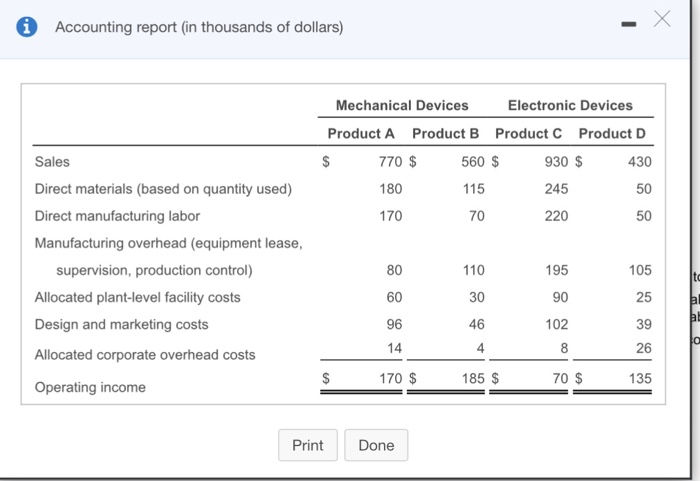

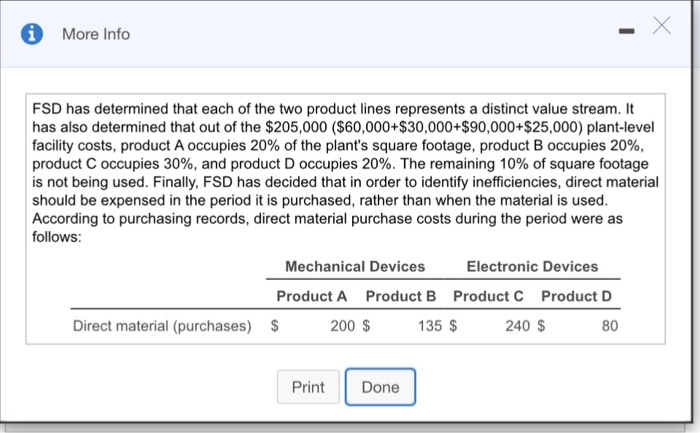

Fox Security Devices (FSD) has introduced a just-in-time production process and is considering the adoption of lean accounting principles to support its new production philosophy. The company has two product lines: Mechanical Devices and Electronic Devices. Two individual products are made in each line. Product-line manufacturing overhead costs are traced directly to product lines and then allocated to the two individual products in each line. The company's traditional cost accounting system allocates al plant-level facility costs and some corporate overhead costs to individual products. The latest accounting report using traditional cost accounting methods included the following information (in thousands of dollars). EEB (Click the icon to view the accounting report.) Read the requirements. (Click the icon to view further information.) Requirement 1. What are the cost objects in FSD's lean accounting system? The cost object in lean accounting is the FSD has identified the following area(s) Requirement 2. Compute operating income for the cost objects identified in requirement 1 using lean accounting principles. What would you compare this operating income against? Comment on your results Use the table below to compute operating income for the cost objects identified in requirement 1 using lean accounting principles. (Enter all amounts in thousands.) Mechanical Electronic Devices Devices Sales Costs Direct material Direct manufacturing labor Manufacturing overhead Design and marketing costs Plant facility costs Value stream operating income What would you compare this operating income against? Comment on your results. FSD's operating income using lean accounting principles should be compared against slightly higher than the total value stream costs for both Mechanical Devices and Electronic Devices and the difference between the total value-stream costs and the VIf the total plant-level costs are total costs is very small, this would indicate that the main for improving efficiency to reduce costs and improve profitability is reducing Value-stream operating income analyses V allocated corporate overhead costs because these costs be controlled or influenced by plant-level managers. Accounting report (in thousands of dollars) Mechanical Devices Electronic Devices Product A Product B Product C Product D Sales Direct materials (based on quantity used) Direct manufacturing labor Manufacturing overhead (equipment lease 770 $ 180 170 560 $ 115 70 930 $ 245 220 430 50 50 supervision, production control) Allocated plant-level facility costs Design and marketing costs Allocated corporate overhead costs Operating income 80 60 96 14 170 $ 110 30 46 4 185 $ 195 90 102 105 25 39 26 135 70 $ PrintDone More Info FSD has determined that each of the two product lines represents a distinct value stream. It has also determined that out of the $205,000 ($60,000+$30,000+$90,000+$25,000) plant-level facility costs, product A occupies 20% of the plant's square footage, product B occupies 20%, product C occupies 30%, and product D occupies 20%. The remaining 10% of square footage is not being used. Finally, FSD has decided that in order to identify inefficiencies, direct material should be expensed in the period it is purchased, rather than when the material is used According to purchasing records, direct material purchase costs during the period were as follows: Mechanical Devices Electronic Devices Product A Product B Product C Product D Direct material (purchases) $ 200 $ 135 $240 S 80 Print Done