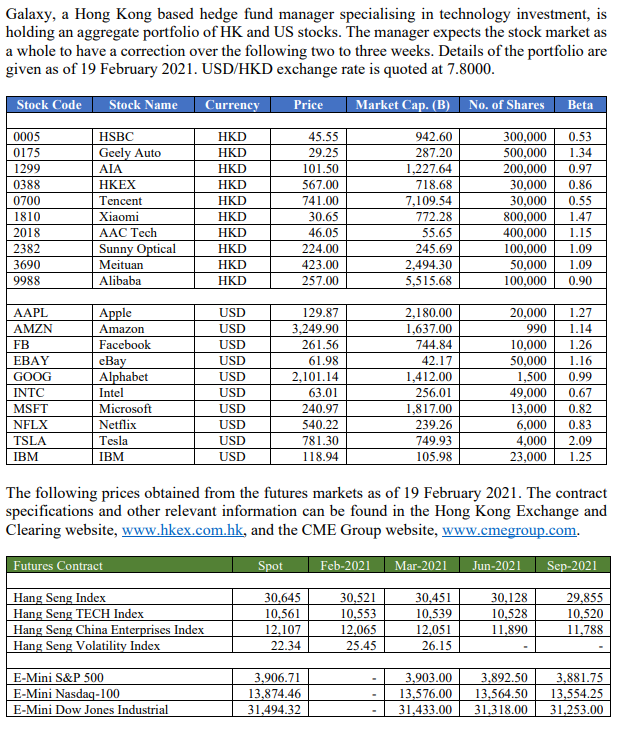

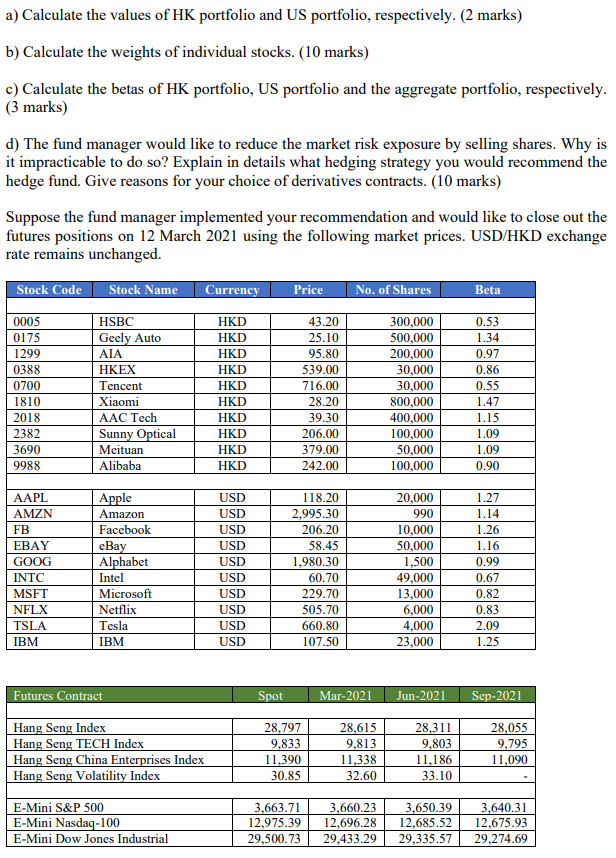

Galaxy, a Hong Kong based hedge fund manager specialising in technology investment, is holding an aggregate portfolio of HK and US stocks. The manager expects the stock market as a whole to have a correction over the following two to three weeks. Details of the portfolio are given as of 19 February 2021. USD/HKD exchange rate is quoted at 7.8000. Stock Code Stock Name Currency Price Market Cap. (B) No. of Shares Beta 0005 0175 1299 0388 0700 1810 2018 2382 3690 9988 HSBC Geely Auto AIA HKEX Tencent Xiaomi AAC Tech Sunny Optical Meituan Alibaba HKD HKD HKD HKD HKD HKD HKD HKD HKD HKD 45.55 29.25 101.50 567.00 741.00 30.65 46.05 224.00 423.00 257.00 942.60 287.20 1,227.64 718.68 7,109.54 772.28 55.65 245.69 2,494.30 5,515.68 300,000 500,000 200,000 30,000 30,000 800,000 400,000 100,000 50,000 100,000 0.53 1.34 0.97 0.86 0.55 1.47 1.15 1.09 1.09 0.90 AAPL AMZN FB EBAY GOOG INTC MSFT NFLX TSLA IBM Apple Amazon Facebook eBay Alphabet Intel Microsoft Netflix Tesla IBM USD USD USD USD USD USD USD USD USD USD 129.87 3,249.90 261.56 61.98 2.101.14 63.01 240.97 540.22 781.30 118.94 2,180.00 1,637.00 744.84 42.17 1,412.00 256.01 1,817.00 239.26 749.93 105.98 20,000 990 10,000 50,000 1,500 49,000 13,000 6,000 4,000 23,000 1.27 1.14 1.26 1.16 0.99 0.67 0.82 0.83 2.09 1.25 The following prices obtained from the futures markets as of 19 February 2021. The contract specifications and other relevant information can be found in the Hong Kong Exchange and Clearing website, www.hkex.com.hk, and the CME Group website, www.cmegroup.com. Futures Contract Spot Feb-2021 Mar-2021 Jun-2021 Sep-2021 Hang Seng Index Hang Seng TECH Index Hang Seng China Enterprises Index Hang Seng Volatility Index 30,645 10,561 12.107 22.34 30,521 10,553 12,065 25.45 30,451 10,539 12,051 26.15 30,128 10,528 11,890 29,855 10,520 11.788 E-Mini S&P 500 E-Mini Nasdaq-100 E-Mini Dow Jones Industrial 3,906.71 13,874.46 31,494.32 3.903.00 13,576.00 31,433.00 3,892.50 13,564.50 31,318.00 3,881.75 13,554.25 31,253.00 a) Calculate the values of HK portfolio and US portfolio, respectively. (2 marks) b) Calculate the weights of individual stocks. (10 marks) c) Calculate the betas of HK portfolio, US portfolio and the aggregate portfolio, respectively. (3 marks) d) The fund manager would like to reduce the market risk exposure by selling shares. Why is it impracticable to do so? Explain in details what hedging strategy you would recommend the hedge fund. Give reasons for your choice of derivatives contracts. (10 marks) Suppose the fund manager implemented your recommendation and would like to close out the futures positions on 12 March 2021 using the following market prices. USD/HKD exchange rate remains unchanged. Stock Code Stock Name Currency Price No. of Shares Beta 0005 0175 1299 0388 0700 1810 2018 2382 3690 9988 HSBC Geely Auto AIA HKEX Tencent Xiaomi AAC Tech Sunny Optical Meituan Alibaba HKD HKD HKD HKD HKD HKD HKD HKD HKD HKD 43.20 25.10 95.80 539.00 716.00 28.20 39.30 206.00 379.00 242.00 300,000 500,000 200,000 30,000 30,000 800,000 400,000 100,000 50,000 100,000 0.53 1.34 0.97 0.86 0.55 1.47 1.15 1.09 1.09 0.90 AAPL AMZN FB EBAY GOOG INTC MSFT NFLX TSLA IBM Apple Amazon Facebook eBay Alphabet Intel Microsoft Netflix Tesla IBM USD USD USD USD USD USD USD USD USD USD 118.20 2,995.30 206.20 58.45 1,980.30 60.70 229.70 505.70 660.80 107.50 20,000 990 10,000 50,000 1,500 49,000 13,000 6,000 4,000 23,000 1.27 1.14 1.26 1.16 0.99 0.67 0.82 0.83 2.09 1.25 Futures Contract Spot Mar-2021 Jun-2021 Sep-2021 Hang Seng Index Hang Seng TECH Index Hang Seng China Enterprises Index Hang Seng Volatility Index 28.797 9.833 11.390 30.85 28,615 9,813 11,338 32.60 28.311 9,803 11,186 33.10 28,055 9,795 11,090 E-Mini S&P 500 E-Mini Nasdaq-100 E-Mini Dow Jones Industrial 3,663.71 12,975.39 29,500.73 3,660.23 12,696.28 29,433.29 3,650.39 12,685.52 29,335.57 3,640.31 12,675.93 29,274.69 e) Calculate the profit/loss of HK portfolio, US portfolio and the futures positions taken, respectively. (4 marks) f) Calculate the overall profit/loss and comment the effectiveness of the hedging strategy. (4 marks) After the market correction, the fund manager foresees the benefit of massive capital inflows from mainland China to Hong Kong. He decides to increase the beta of HK portfolio to 1.20 and re-allocate 100% of the US fund to the HK stock market temporarily. g) Advice the fund manage how this position can be achieved using the futures contracts as of 12 March. (10 marks) h) If retaining this position for 12 months, what alternative trading strategies should be taken? (7 marks) Galaxy, a Hong Kong based hedge fund manager specialising in technology investment, is holding an aggregate portfolio of HK and US stocks. The manager expects the stock market as a whole to have a correction over the following two to three weeks. Details of the portfolio are given as of 19 February 2021. USD/HKD exchange rate is quoted at 7.8000. Stock Code Stock Name Currency Price Market Cap. (B) No. of Shares Beta 0005 0175 1299 0388 0700 1810 2018 2382 3690 9988 HSBC Geely Auto AIA HKEX Tencent Xiaomi AAC Tech Sunny Optical Meituan Alibaba HKD HKD HKD HKD HKD HKD HKD HKD HKD HKD 45.55 29.25 101.50 567.00 741.00 30.65 46.05 224.00 423.00 257.00 942.60 287.20 1,227.64 718.68 7,109.54 772.28 55.65 245.69 2,494.30 5,515.68 300,000 500,000 200,000 30,000 30,000 800,000 400,000 100,000 50,000 100,000 0.53 1.34 0.97 0.86 0.55 1.47 1.15 1.09 1.09 0.90 AAPL AMZN FB EBAY GOOG INTC MSFT NFLX TSLA IBM Apple Amazon Facebook eBay Alphabet Intel Microsoft Netflix Tesla IBM USD USD USD USD USD USD USD USD USD USD 129.87 3,249.90 261.56 61.98 2.101.14 63.01 240.97 540.22 781.30 118.94 2,180.00 1,637.00 744.84 42.17 1,412.00 256.01 1,817.00 239.26 749.93 105.98 20,000 990 10,000 50,000 1,500 49,000 13,000 6,000 4,000 23,000 1.27 1.14 1.26 1.16 0.99 0.67 0.82 0.83 2.09 1.25 The following prices obtained from the futures markets as of 19 February 2021. The contract specifications and other relevant information can be found in the Hong Kong Exchange and Clearing website, www.hkex.com.hk, and the CME Group website, www.cmegroup.com. Futures Contract Spot Feb-2021 Mar-2021 Jun-2021 Sep-2021 Hang Seng Index Hang Seng TECH Index Hang Seng China Enterprises Index Hang Seng Volatility Index 30,645 10,561 12.107 22.34 30,521 10,553 12,065 25.45 30,451 10,539 12,051 26.15 30,128 10,528 11,890 29,855 10,520 11.788 E-Mini S&P 500 E-Mini Nasdaq-100 E-Mini Dow Jones Industrial 3,906.71 13,874.46 31,494.32 3.903.00 13,576.00 31,433.00 3,892.50 13,564.50 31,318.00 3,881.75 13,554.25 31,253.00 a) Calculate the values of HK portfolio and US portfolio, respectively. (2 marks) b) Calculate the weights of individual stocks. (10 marks) c) Calculate the betas of HK portfolio, US portfolio and the aggregate portfolio, respectively. (3 marks) d) The fund manager would like to reduce the market risk exposure by selling shares. Why is it impracticable to do so? Explain in details what hedging strategy you would recommend the hedge fund. Give reasons for your choice of derivatives contracts. (10 marks) Suppose the fund manager implemented your recommendation and would like to close out the futures positions on 12 March 2021 using the following market prices. USD/HKD exchange rate remains unchanged. Stock Code Stock Name Currency Price No. of Shares Beta 0005 0175 1299 0388 0700 1810 2018 2382 3690 9988 HSBC Geely Auto AIA HKEX Tencent Xiaomi AAC Tech Sunny Optical Meituan Alibaba HKD HKD HKD HKD HKD HKD HKD HKD HKD HKD 43.20 25.10 95.80 539.00 716.00 28.20 39.30 206.00 379.00 242.00 300,000 500,000 200,000 30,000 30,000 800,000 400,000 100,000 50,000 100,000 0.53 1.34 0.97 0.86 0.55 1.47 1.15 1.09 1.09 0.90 AAPL AMZN FB EBAY GOOG INTC MSFT NFLX TSLA IBM Apple Amazon Facebook eBay Alphabet Intel Microsoft Netflix Tesla IBM USD USD USD USD USD USD USD USD USD USD 118.20 2,995.30 206.20 58.45 1,980.30 60.70 229.70 505.70 660.80 107.50 20,000 990 10,000 50,000 1,500 49,000 13,000 6,000 4,000 23,000 1.27 1.14 1.26 1.16 0.99 0.67 0.82 0.83 2.09 1.25 Futures Contract Spot Mar-2021 Jun-2021 Sep-2021 Hang Seng Index Hang Seng TECH Index Hang Seng China Enterprises Index Hang Seng Volatility Index 28.797 9.833 11.390 30.85 28,615 9,813 11,338 32.60 28.311 9,803 11,186 33.10 28,055 9,795 11,090 E-Mini S&P 500 E-Mini Nasdaq-100 E-Mini Dow Jones Industrial 3,663.71 12,975.39 29,500.73 3,660.23 12,696.28 29,433.29 3,650.39 12,685.52 29,335.57 3,640.31 12,675.93 29,274.69 e) Calculate the profit/loss of HK portfolio, US portfolio and the futures positions taken, respectively. (4 marks) f) Calculate the overall profit/loss and comment the effectiveness of the hedging strategy. (4 marks) After the market correction, the fund manager foresees the benefit of massive capital inflows from mainland China to Hong Kong. He decides to increase the beta of HK portfolio to 1.20 and re-allocate 100% of the US fund to the HK stock market temporarily. g) Advice the fund manage how this position can be achieved using the futures contracts as of 12 March. (10 marks) h) If retaining this position for 12 months, what alternative trading strategies should be taken? (7 marks)