Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Given the following information, and the assumptions of the single-factor model, what is the beta factor of stock 1 ? [ begin{array}{l} beta_{2}=1.2 sigma^{2}left(r_{m}

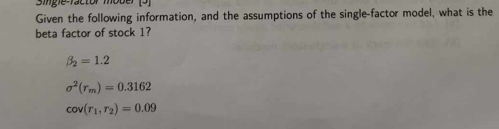

Given the following information, and the assumptions of the single-factor model, what is the beta factor of stock 1 ? \\[ \\begin{array}{l} \\beta_{2}=1.2 \\\\ \\sigma^{2}\\left(r_{m}\ ight)=0.3162 \\\\ \\operatorname{cov}\\left(r_{1}, r_{2}\ ight)=0.09 \\end{array} \\] Given the following information, and the assumptions of the single-factor model, what is the beta factor of stock 1 ? \\[ \\begin{array}{l} \\beta_{2}=1.2 \\\\ \\sigma^{2}\\left(r_{m}\ ight)=0.3162 \\\\ \\operatorname{cov}\\left(r_{1}, r_{2}\ ight)=0.09 \\end{array} \\]

Given the following information, and the assumptions of the single-factor model, what is the beta factor of stock 1 ? \\[ \\begin{array}{l} \\beta_{2}=1.2 \\\\ \\sigma^{2}\\left(r_{m}\ ight)=0.3162 \\\\ \\operatorname{cov}\\left(r_{1}, r_{2}\ ight)=0.09 \\end{array} \\] Given the following information, and the assumptions of the single-factor model, what is the beta factor of stock 1 ? \\[ \\begin{array}{l} \\beta_{2}=1.2 \\\\ \\sigma^{2}\\left(r_{m}\ ight)=0.3162 \\\\ \\operatorname{cov}\\left(r_{1}, r_{2}\ ight)=0.09 \\end{array} \\] Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Introduction To Derivatives And Risk Management

Authors: Don M. Chance, Roberts Brooks

7th Edition

0324321392, 9780324321395