Answered step by step

Verified Expert Solution

Question

1 Approved Answer

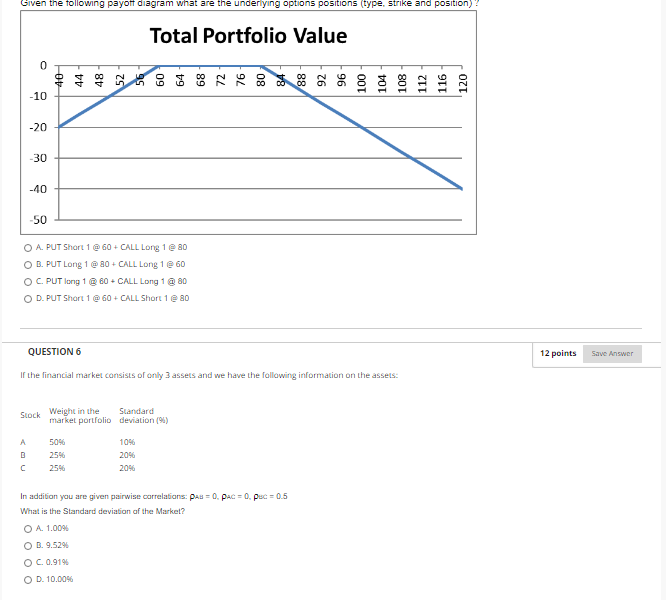

Given the following payoff diagram what are the underlying options positions (type, strike and position) Total Portfolio Value 0 108 112 116 120 -10 -20

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Budget Responsibility And National Audit Bill Source Book Edition Current Political Debates Of The UK Parliament 55th Parliament Volume

Authors: Jeff Nelson

1st Edition

3845468017, 978-3845468013