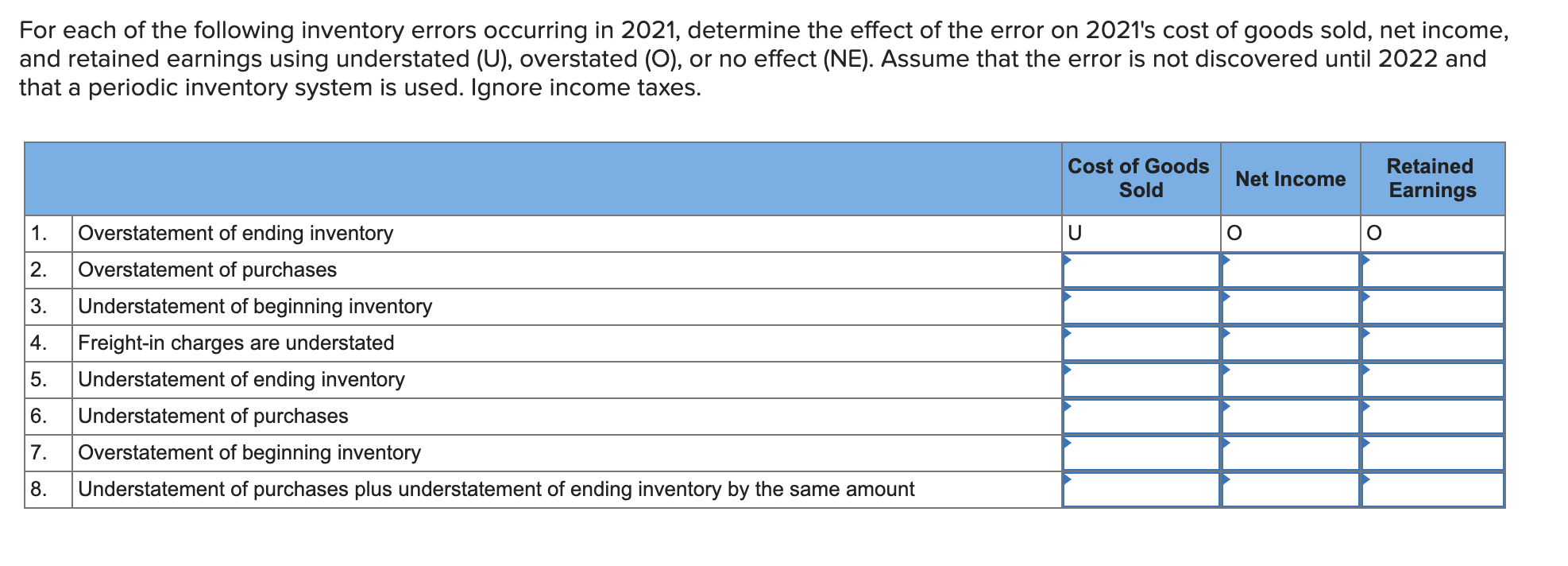

Question

Goddard Company has used the FIFO method of inventory valuation since it began operations in 2018. Goddard decided to change to the average cost method

Goddard Company has used the FIFO method of inventory valuation since it began operations in 2018. Goddard decided to change to the average cost method for determining inventory costs at the beginning of 2021. The following schedule shows year-end inventory balances under the FIFO and average cost methods:

| Year | FIFO | Average Cost | ||||

| 2018 | $ | 45,700 | $ | 55,400 | ||

| 2019 | 80,100 | 71,700 | ||||

| 2020 | 85,800 | 80,100 | ||||

Required: 1. Ignoring income taxes, prepare the 2021 journal entry to adjust the accounts to reflect the average cost method. 2. How much higher or lower would cost of goods sold be in the 2020 revised income statement?

2*******

COGS for 2020 would be _________,_______________ in the revised income statement.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Report Chavarria Dinne And Lamey LLC Contract Deliverables Office Of Inspector U.S Department Of The Interior

Authors: United States Department Of The Interior

1st Edition

1511678526, 978-1511678520