Answered step by step

Verified Expert Solution

Question

1 Approved Answer

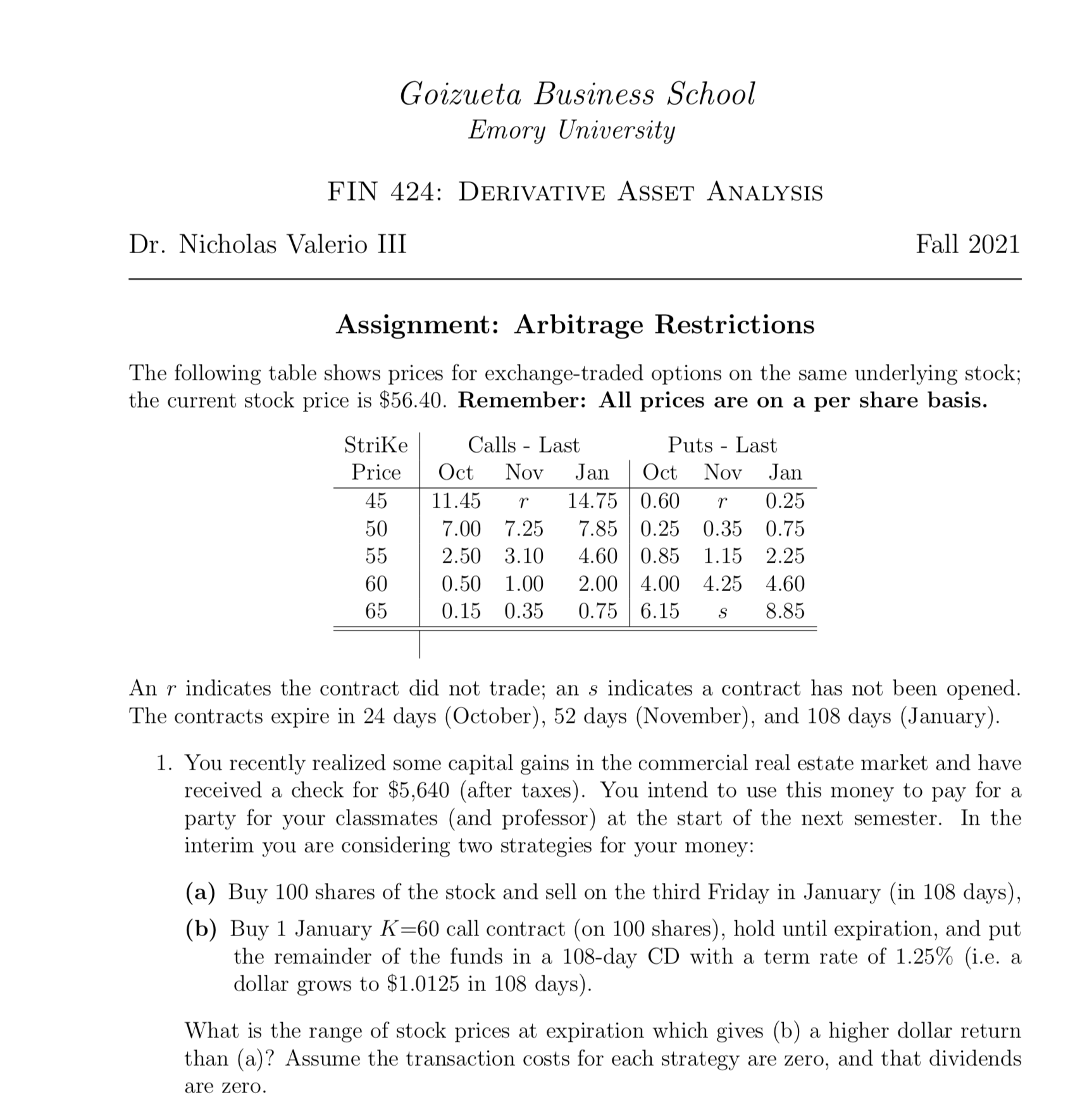

Goizueta Business School Emory University FIN 424: DERIVATIVE ASSET ANALYSIS Dr. Nicholas Valerio III Fall 2021 Assignment: Arbitrage Restrictions The following table shows prices

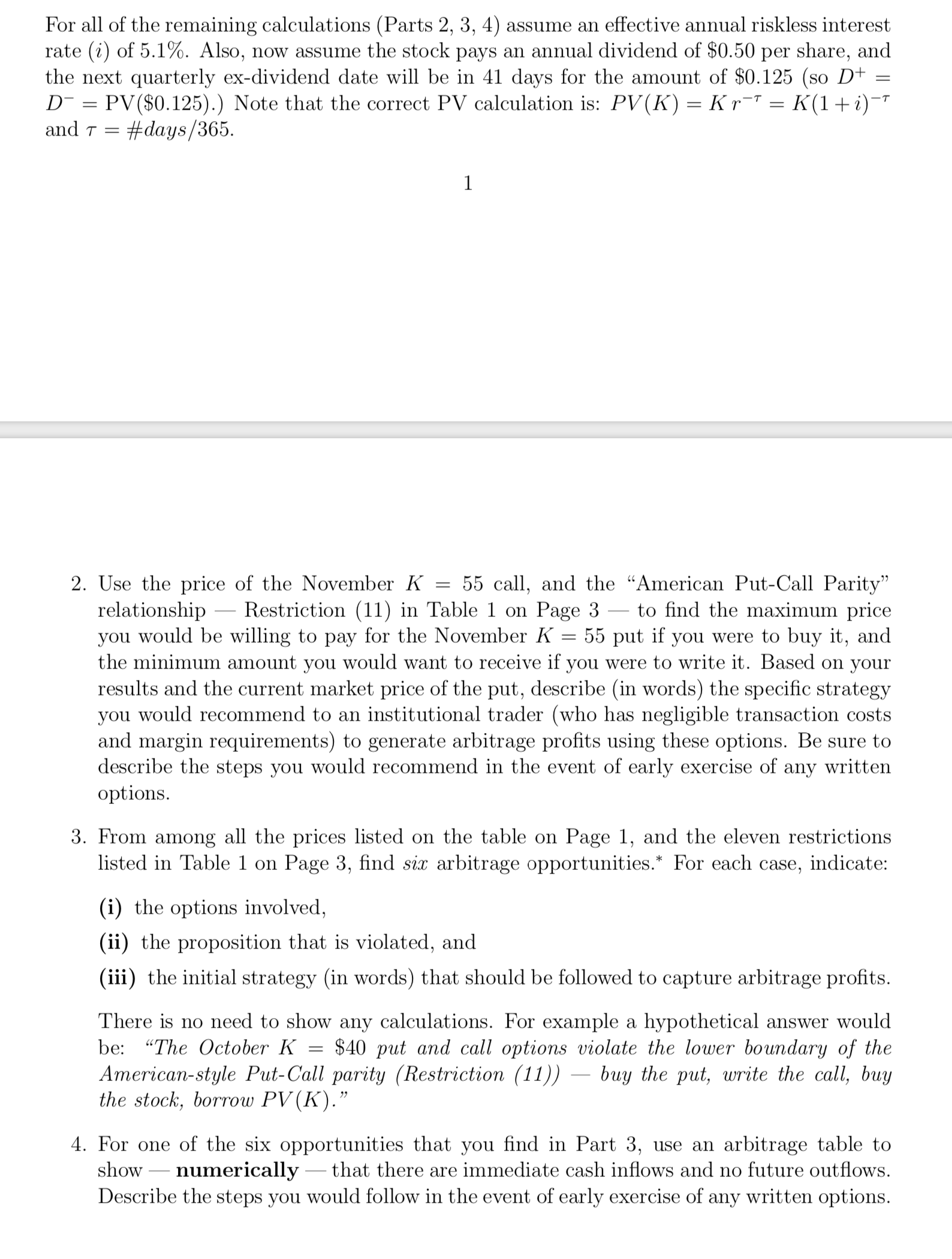

Goizueta Business School Emory University FIN 424: DERIVATIVE ASSET ANALYSIS Dr. Nicholas Valerio III Fall 2021 Assignment: Arbitrage Restrictions The following table shows prices for exchange-traded options on the same underlying stock; the current stock price is $56.40. Remember: All prices are on a per share basis. Strike Calls Last - Puts Last Price Oct Nov Jan Oct Nov Jan 45 11.45 r 50 7.00 7.25 55 2.50 3.10 14.75 0.60 r 0.25 7.85 0.25 4.60 0.85 0.35 0.75 1.15 2.25 60 0.50 1.00 65 0.15 0.35 2.00 4.00 0.75 6.15 S 8.85 4.25 4.60 An indicates the contract did not trade; an s indicates a contract has not been opened. The contracts expire in 24 days (October), 52 days (November), and 108 days (January). 1. You recently realized some capital gains in the commercial real estate market and have received a check for $5,640 (after taxes). You intend to use this money to pay for a party for your classmates (and professor) at the start of the next semester. In the interim you are considering two strategies for your money: (a) Buy 100 shares of the stock and sell on the third Friday in January (in 108 days), (b) Buy 1 January K=60 call contract (on 100 shares), hold until expiration, and put the remainder of the funds in a 108-day CD with a term rate of 1.25% (i.e. a dollar grows to $1.0125 in 108 days). What is the range of stock prices at expiration which gives (b) a higher dollar return than (a)? Assume the transaction costs for each strategy are zero, and that dividends are zero. For all of the remaining calculations (Parts 2, 3, 4) assume an effective annual riskless interest rate (i) of 5.1%. Also, now assume the stock pays an annual dividend of $0.50 per share, and the next quarterly ex-dividend date will be in 41 days for the amount of $0.125 (so D+ D = PV ($0.125).) Note that the correct PV calculation is: PV (K) = K r = K(1+i) and 7 = #days/365. = 1 2. Use the price of the November K = 55 call, and the "American Put-Call Parity" relationship - Restriction (11) in Table 1 on Page 3 = to find the maximum price you would be willing to pay for the November K 55 put if you were to buy it, and the minimum amount you would want to receive if you were to write it. Based on your results and the current market price of the put, describe (in words) the specific strategy you would recommend to an institutional trader (who has negligible transaction costs and margin requirements) to generate arbitrage profits using these options. Be sure to describe the steps you would recommend in the event of early exercise of any written options. 3. From among all the prices listed on the table on Page 1, and the eleven restrictions listed in Table 1 on Page 3, find six arbitrage opportunities.* For each case, indicate: (i) the options involved, (ii) the proposition that is violated, and (iii) the initial strategy (in words) that should be followed to capture arbitrage profits. There is no need to show any calculations. For example a hypothetical answer would be: "The October K = $40 put and call options violate the lower boundary of the American-style Put-Call parity (Restriction (11)) buy the put, write the call, buy the stock, borrow PV(K)." 4. For one of the six opportunities that you find in Part 3, use an arbitrage table to show numerically that there are immediate cash inflows and no future outflows. Describe the steps you would follow in the event of early exercise of any written options. Table 1: Arbitrage Restrictions on Call and Put Options If K < K2 < K3 then, for the same expiration date: C(K2) C(K) (1) C(K1)C(K2) K2 K (2) C(K2) AC(K) + (1 )C(K3) (3) P(K) P(K2) (4) P(K2) P(K1) K- K (5) P(K2) XP(K) + (1 X)P(K3) (6) where A = (K3-K2) and (1 - x) = (K2-K). Next, if 71 < 72 then, for the same K: C(T1) C(T2) T2 The Boundary propositions are: P(T1) P(T2) (7) (8) max - {0, S K, S PV(K) - D+} C S (9) max {0, K S, PV (K) + D S} - P K (10) = where PV (K): = Kr-T = K(1+i), with 7 = #days/365, and D+ the PV of the Maximum Expected Dividend and D- the PV of the Minimum Expected Dividend. = Finally, the American-style Put-Call parity relationship: C-SPV (K) P C-S + K +D+ (11)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Analysis for Financial Management

Authors: Robert Higgins

11th edition

77861787, 978-0077861780