Question

Harry and Belinda Johnson spend $20 per month on life insurance in the form of a premium on a $10,000, paid-at-65 cash-value policy on Harry

Harry and Belinda Johnson spend $20 per month on life insurance in the form of a premium on a $10,000, paid-at-65 cash-value policy on Harry that his parents bought for him years ago. Belinda has a group term insurance policy from her employer with a face amount of $200,000. By choosing a group life insurance plan from his menu of employee benefits, Harry now has $100,000 of group term life insurance. Harry and Belinda have decided that, because they have no children, they could reduce their life insurance needs by protecting one another's income for only four years, assuming the survivor would be able to fend for himself or herself after that time. They also realize that their savings fund is so low that it would have no bearing on their life insurance needs. Harry and Belinda are basing their calculations on a projected 4 percent rate of return after taxes and inflation. They also estimate the following expenses: $15,000 for final expenses, $20,000 for readjustment expenses, and $5,000 for repayment of short-term debts.

REQUIRED:

1. Should the $3,000 interest earnings from Harry's trust fund be included in his annual income for the purposes of calculating the dollar loss if he were to die? Explain your response.

2. Based on your response to the previous question, how much more life insurance does Harry need? Next repeat the calculations to arrive at the additional life insurance needed on Belinda's life. (Use the Run the Numbers worksheet)

3. How might the Johnsons most economically meet any additional life insurance needs you have determined they may have?

4. In addition to their life insurance planning, how might the Johnsons begin to prepare for their retirement years?

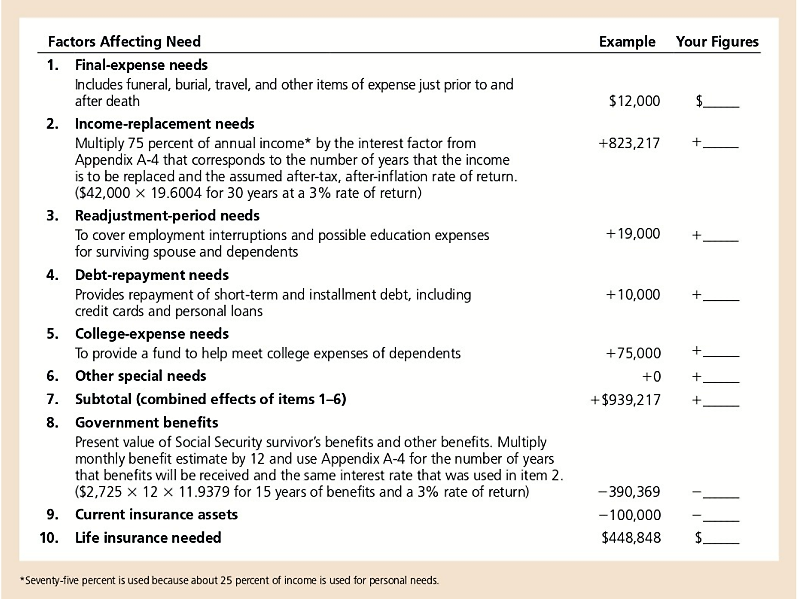

Run the numbers worksheet

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Preppers Financial Guide

Authors: Jim Cobb

1st Edition

1612434037, 978-1612434032