Question

he data for this question is provided in the sheet labelled Question 3. Suppose that you can borrow or lend at the contemporaneous LIBOR rate,

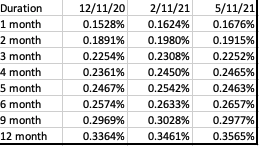

he data for this question is provided in the sheet labelled "Question 3."

Suppose that you can borrow or lend at the contemporaneous LIBOR rate, and you wish to lend $350,000 from 2/11/2021 until 5/11/2021 but wish to lock in the rate at which you can lend now (assume that "now" is 12/11/2020). All rates are annualized (and yes, they are all less than 1%).

a. What type of FRA would you want to take out (i.e. what are t1 and t2)?

b. Assuming that there are no arbitrage opportunities and no bid-ask spread on any of the LIBOR rates or the FRA, what must the rate of this FRA be?

c.To lock in your rate, would you need to go long or short this FRA? What would be its notional value?

d.In my Excel file, Column B lists the LIBOR yield curve on 12/11/2020. Column C lists it for 2/22/2021, and Column C lists it for 5/11/2021. In order to effectively lend the desired amount, what further transaction would you need to take, when, and at what rate? (Hint: On 2/11/2021 you should have a net cash outflow of $350,000).

e.Show that given all the transactions you have taken, your cash inflow on 5/11/2021 is the same as what you would expect if you lent $350,000 at the rate you calculated in part b.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Derivatives And Risk Management

Authors: Robert Brooks, Don M Chance, Roberts Brooks

8th Edition

0324601212, 9780324601213