Question: Hello, I need assistance with the questions below. I do have most completed but need assistance with the others. #5, #8, #10, and #11. Also,

Hello, I need assistance with the questions below. I do have most completed but need assistance with the others. #5, #8, #10, and #11. Also, please review the others and add what I may be missing to help me prepare for my prep course. For question #10, I've attached the article that will help. Thank you.

1.) What are the three key financial statements? Explain their purpose and type of information provided by each.

- Income Statement - The income statement shows the performance of the company all throughout the accounting period. It displays the sales revenue, cost of goods sold, and expenses to calculate the net income generated by the company.

- Balance Sheet. - It shows the financial position of the business. Balance sheet includes assets, liabilities, and shareholder's equity.

- Cash flow Statement - Cash flow statement displays the net change in cash per accounting period and is divided three sections:

- Cash from Operations

- Cash used in Investing

- Cash from financing

2.) What is trend analysis and how does it relate to the firm's ratio?

- Trend Analysis is a technique used in technical analysis wherein it helps predict the future price movements based on the idea that has happened in the past. Trend Analysis can help compare two financial statements to determine the currency and percentage charges.

3.) What is benchmarking and how is it related to the firm's ratio?

- Benchmarking is the process through which a business measures its products, services, and practices against its competitors, or those companies recognized as the leaders in its industry. Benchmarking financial ratios help monitor the specific vital signs that a company knows when something starts trending downward and precisely where attention and resources are most needed.

4.) Why is the financial forecasting process important? How is it done?

- Financial Forecasting is the process of predicting or estimating the statistics of a business in the future. It helps forecast how the business will perform in the future based on the previous analysis of the financial statements (Income statement, Balance Sheet, etc.), current conditions, and past trend analysis of the financial, future internal and external environment.

5.) Explain how changes in forecast assumptions will affect a firm's external financing requirements.

6.) What is DuPont formula and how is it important in managing a firm's growth?

- DuPont formula calculates the Return on Equity (ROE) by dividing it into 3 parts- Profit Margins, Total Asset Turnover, and the Leverage factor. DuPont formula is effectively used by investors and financial analyst to understand how efficiently a company is in utilizing its resources and how leveraged the company is.

7.) What is sustainable growth rate and how is it important in managing a firm's growth?

- Sustainable Growth Rate is a company's maximum growth rate in sales using internal financial resources, while not having to increase payables or issue new equity. It is important because it can avoid straining financial resources and overextending their financial leverage.

8.) In terms of capital budgeting projects, which cash flows should be incrementally applied to a project and which ones should not be applied?

9.) How does accelerated depreciation affect project cash flows?

- Accelerated depreciation does not directly impact the amount of cash flow generated by a company, but it is tax-deductible and will reduce the cash outflows related to income taxes. Depreciation is considered a non-cash expense and designed to reduce the recorded asset.

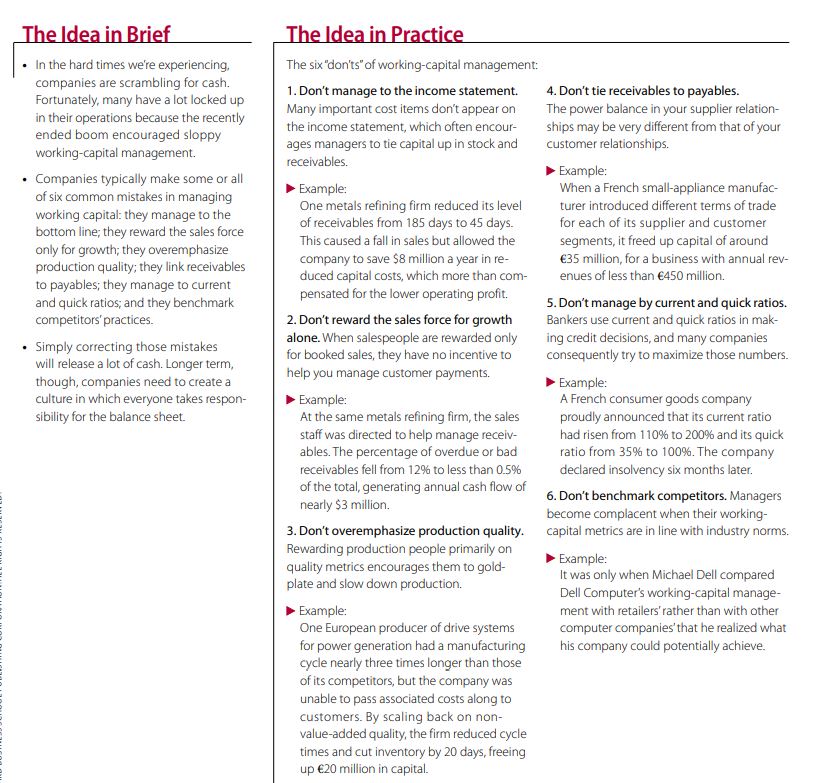

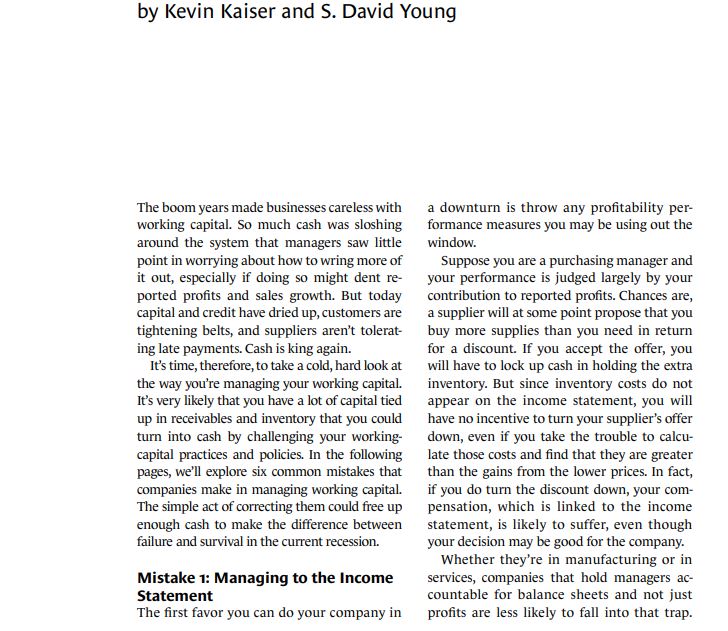

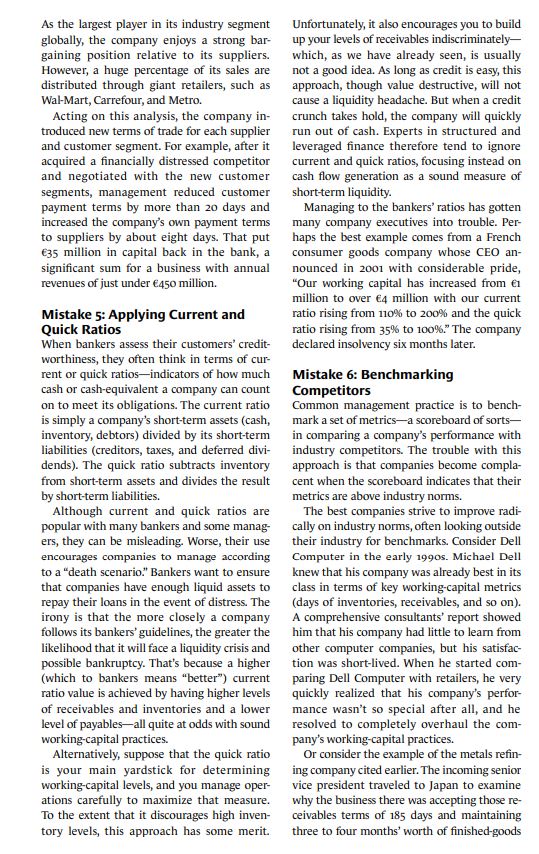

10.) From the article, "Need Cash? Look inside your Company" Discuss the 6 don'ts of working capital management. Provide examples.

11.) What are value drivers? What is the role they play in value creation? Select a value driver. Identify two strategies that you believe could boost stock price. Explain how each strategy would affect Free Cash Flow (FCF) and ultimately stock price.

12.) What is the intrinsic value of a share?

- Intrinsic Value of a stock refers to the measure of what a stock is worth. This measure is arrived at by means of an objective calculation or complex financial model, rather than using the currently trading market prices of the stock.

13.) What are the differences and similarities between capital budgeting project analysis and firm valuation?

- Capital Budgeting Project Analysis is a process of evaluating how a company invests in capital assets- assets that provide cash inflow for more than a year while Firm Valuation is a process used to predict the economic value of an owner's interest in a business. It is used by investors and financial analyst to determine the price they are willing to pay or receive to affect a sale of a business.

14.) Present the pros and cons of shareholder value creation as the goal of a firm.

- Shareholder Value Creation refers to the continued creation of shareholder wealth through annual dividend receipts and share price appreciation.

- Advantages:

- Shareholder's value creation offers the management of a company with a long-term view and based on this; the management can design strategic decisions.

- It allows the company to emphasize more on the future and its consumers and offers a universal approach as well.

- Disadvantages:

- The company cannot create shareholder value if they disregard the important constituencies. They must have a good relationship with customers, employees, suppliers, government and so on.

- Capital Markets are becoming progressively international. Investors can voluntarily shift investments to higher yielding opportunities.

- A lot of organizations tend to stress only upon maximizing their profits for the sake of maximizing shareholder's value and compromises business ethics but fetch profits.

15.) Explain the weighted average cost of capital (WACC) calculation. What is its significance in valuation analysis? What are the components of the calculation? What does each represent?

- Weighted Average Cost of Capital (WACC)is referred to as the firm's cost of capital. It represents the minimum return that a company must earn on an existing asset to satisfy its creditors, owners, and other providers of capital. There are two components of the WACC calculation - Debt and Equity. The Advantages of Debt are 1.) no loss of voting rights, and 2.) interest expense is deductible; For equity, The advantages include 1.) No legal obligation to pay and 2.) Lower Financial risk.

16.) Provide 5 reasons why a firm would want to acquire another firm. Explain why most acquisitions are unsuccessful.

- Companies acquire other companies for a number of reasons:

- Eliminating Competition - More dominance on the industry of the market and the products can be sold at a higher price due to the laws of Demand and Supply.

- Expand into new markets - Acquirers can provide an opportunity to grow market share without doing much. For example, a beer company may choose to buy a smaller brewery, enabling the smaller outfit to produce more beer and increase its sales to brand-loyal customers.

- Synergy - It is expected that two companies together will have greater revenues and its expenses will be lower. Expenses are expected to be lower due to economies of scale (combining operations; consolidating systems and computers; centralization, etc.)

- Increase Supply-chain Pricing power- By buying out one of its suppliers or distributors, a business can often gain the ability to ship out the products at a lower cost.

- Obtain advanced technology- A company can acquire a company that has the complete package that would be difficult or time-consuming to develop by the company itself.

- Overpaying is the most common reason why most acquisition fails. Most attractive target companies under the assumption that the business is always for sale when a buyer is willing to overpay. Also, one of the reasons why acquisition is unsuccessful is lack of strategic plan.

17.) Discuss synergy value and provide examples.

- Synergy is the concept that the combined value and performance of two companies will be greater than the sum of the separate individual parts. Real world example of Synergy is when Proctor and Gamble Company acquired Gillette in 2005. It is claimed that the increases to the company's growth objective are driven by the identified synergy opportunities from the P&G/Gillette merging.

18.) What is the maximum acceptable purchase price? What is value split between a buyer and a seller?

- In Merger and Acquisition transaction, Maximum acceptable Purchase Price refers to the highest price and acquirer is willing and able to pay.

19.) Discuss the importance of taxes and the risk of financial distress in determining capital structure?

- Income Tax usually have a significant effect on the cash flow of a company and should be taken into account while making Capital Budgeting Decisions. An investment that looks desirable without considering income tax may become unacceptable after considering income tax.

20.) Discuss the three decision tools used to analyzing capital budgeting projects. What are the advantages and disadvantages of each tool?

- Capital Budgeting is the process a business undergoes to evaluate potential major projects or investment. There are three analyzation tools that commonly used to know if a project is feasible or not:

- Discounted Cash Flow Analysis looks at the initial cash outflow needed to fund a project, the mix of cash inflows in the form or revenue, and other future outflows in the form of maintenance and other costs.

- Payback Analysis is the simplest form of capital budgeting analysis, but it is also the least accurate. It calculates how long it will take to recoup the costs of an investment.

- Throughput Analysis is the most complicated form of capital budgeting and also the most accurate in helping managers decide which projects to pursue. This analysis assumes that nearly all costs are operating expenses.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts