Answered step by step

Verified Expert Solution

Question

1 Approved Answer

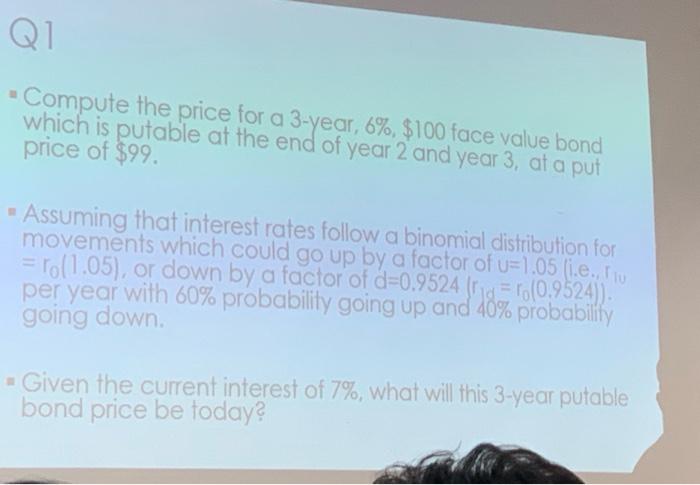

Help me please Compute the price for a 3-year, 6%, $100 face value bond which is putable at the end of year 2 and year

Help me please

"Compute the price for a 3-year, 6\%, \$100 face value bond which is putable at the end of year 2 and year 3 , at a put price of $99. - Assuming that interest rates follow a binomial distribution for movements which could go up by a factor of u=1.05 (i.e. r1. =r0(1.05), or down by a factor of d=0.9524(r,r0=r0(0.9524). per year with 60% probability going up and 40% probavinty going down. " Given the current interest of 7%, what will this 3-year putable bond price be today? "Compute the price for a 3-year, 6\%, \$100 face value bond which is putable at the end of year 2 and year 3 , at a put price of $99. - Assuming that interest rates follow a binomial distribution for movements which could go up by a factor of u=1.05 (i.e. r1. =r0(1.05), or down by a factor of d=0.9524(r,r0=r0(0.9524). per year with 60% probability going up and 40% probavinty going down. " Given the current interest of 7%, what will this 3-year putable bond price be today Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Nurse Managers Guide To Budgeting And Finance

Authors: Al Rundio

2nd Edition

1940446589, 978-1940446585