Answered step by step

Verified Expert Solution

Question

1 Approved Answer

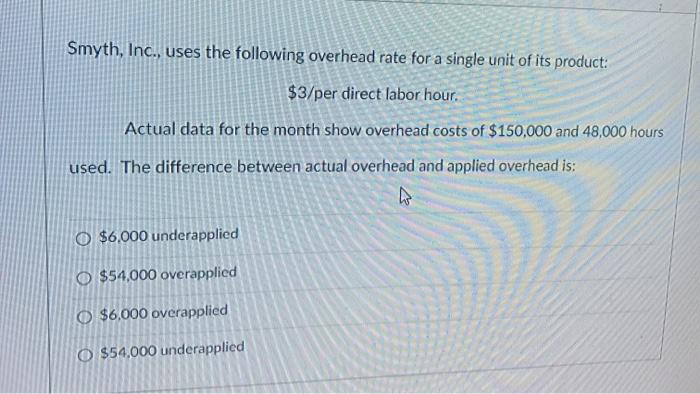

help?? Smyth, Inc., uses the following overhead rate for a single unit of its product: $3/per direct labor hour. Actual data for the month show

help??

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

How To Build A Cyber Resilient Organization Internal Audit And IT Audit

Authors: Dan Shoemaker, Anne Kohnke, Ken Sigler

1st Edition

1138558192, 978-1138558199