Answered step by step

Verified Expert Solution

Question

1 Approved Answer

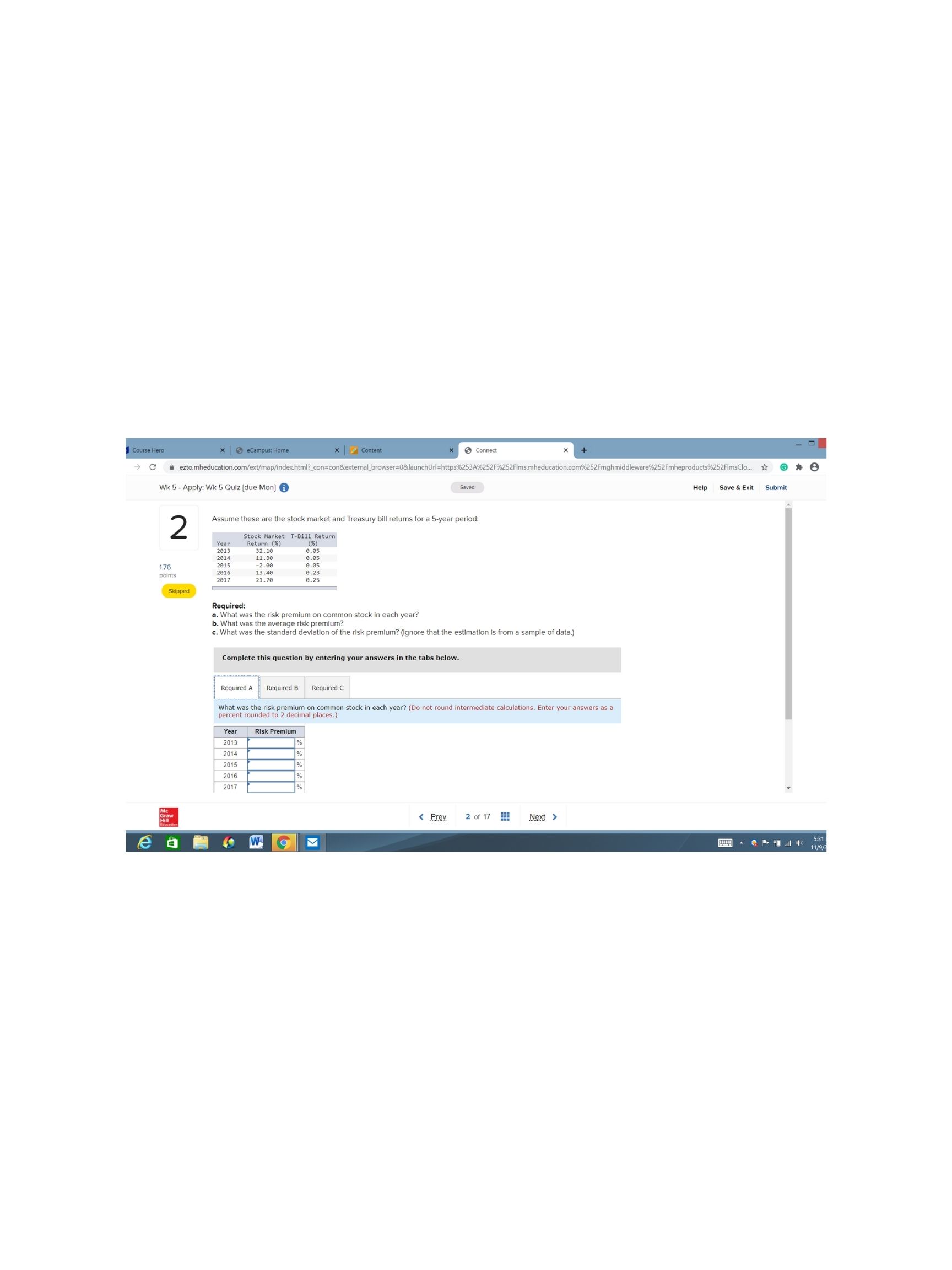

help with question Course Hero * | eCampus : Home * | Content * Connect C a ezto.mheducation.com/ext/map/index.html?_con=con&external_browser=08launchUrl=https6253A%252F6252Fims.mheducation.com%252Fmghmiddleware%252Fmheproducts%252FlmsClo... # @ * Wk 5 - Apply:

help with question

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Modeling

Authors: Simon Benninga

2nd Edition

0262024829, 9780262024822