Question

Hi im studying to a exam. This is a example question from a older exam. Can you help me to solve it and show calculations,

Hi im studying to a exam. This is a example question from a older exam. Can you help me to solve it and show calculations, and also give me a few words in explanation.

The correct answer on this question is A

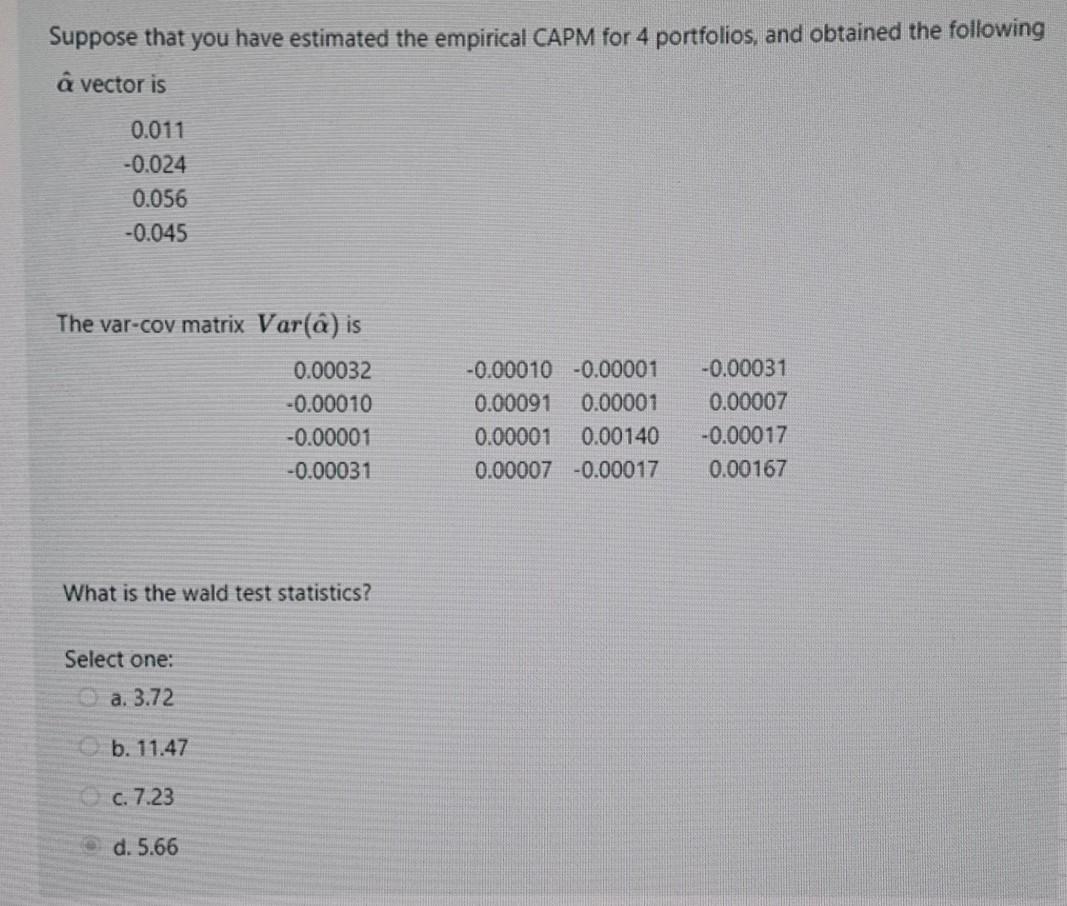

Suppose that you have estimated the empirical CAPM for 4 portfolios, and obtained the following vector is 0.011 -0.024 0.056 -0.045 The var-cov matrix Var(a) is 0.00032 -0.00010 -0.00001 -0.00031 -0.00010 -0.00001 0.00091 0.00001 0.00001 0.00140 0.00007 -0.00017 -0.00031 0.00007 -0.00017 0.00167 What is the wald test statistics? Select one: a. 3.72 b. 11.47 c. 7.23 d. 5.66 Suppose that you have estimated the empirical CAPM for 4 portfolios, and obtained the following vector is 0.011 -0.024 0.056 -0.045 The var-cov matrix Var(a) is 0.00032 -0.00010 -0.00001 -0.00031 -0.00010 -0.00001 0.00091 0.00001 0.00001 0.00140 0.00007 -0.00017 -0.00031 0.00007 -0.00017 0.00167 What is the wald test statistics? Select one: a. 3.72 b. 11.47 c. 7.23 d. 5.66Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Valuation Measuring and managing the values of companies

Authors: Mckinsey, Tim Koller, Marc Goedhart, David Wessel

5th edition

978-0470424650, 9780470889930, 470424656, 470889934, 978-047042470