hi please use excel and =formulatext, show calculations please or send worksheet. and answer case 2 please all questions related and need answers please and show formulas and explain these please

hi please use excel and =formulatext, show calculations please or send worksheet. and answer case 2 please all questions related and need answers please and show formulas and explain these please

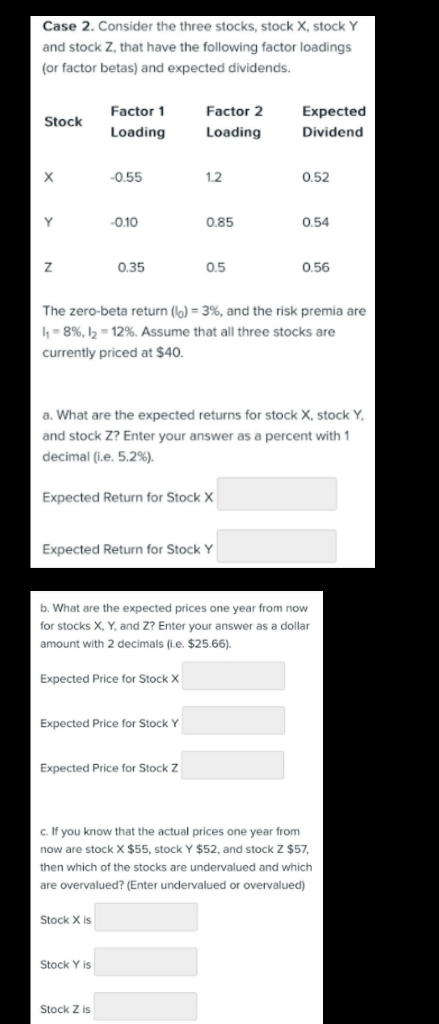

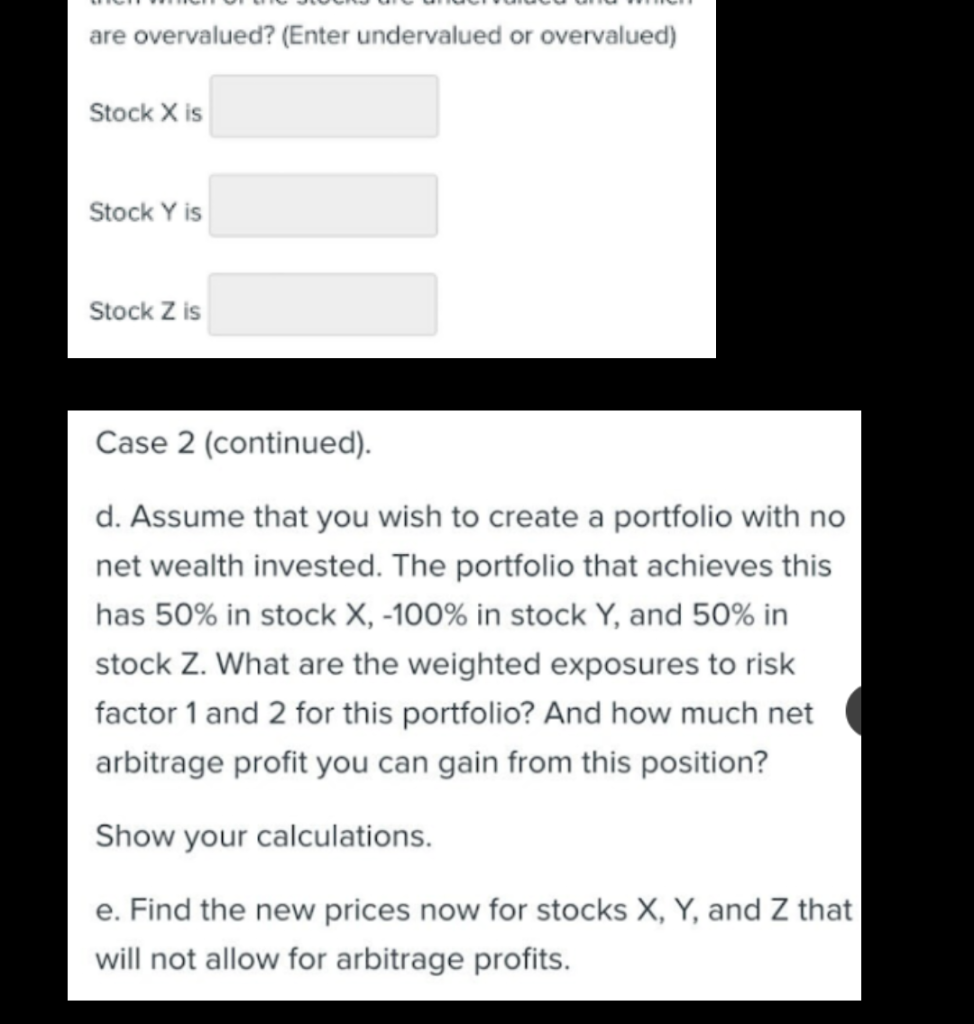

Case 2. Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas) and expected dividends. The zero-beta return (b0)=3%, and the risk premia are I1=8%,I2=12%. Assume that all three stocks are currently priced at $40. a. What are the expected returns for stock X, stock Y, and stock Z ? Enter your answer as a percent with 1 decimal (i.e. 5.2\%). Expected Return for Stock X Expected Return for Stock Y b. What are the expected prices one year from now for stocks X,Y, and Z ? Enter your answer as a dollar amount with 2 decimals (i.e. $25.66 ). Expected Price for Stock X Expected Price for Stock Y Expected Price for Stock Z c. If you know that the actual prices one year from now are stock X$55, stock Y$52, and stock Z$57, then which of the stocks are undervalued and which are overvalued? (Enter undervalued or overvalued) Stock X is Stock Y is Stock Z is are overvalued? (Enter undervalued or overvalued) Stock X is Stock Y is Stock Z is Case 2 (continued). d. Assume that you wish to create a portfolio with no net wealth invested. The portfolio that achieves this has 50% in stock X,100% in stock Y, and 50% in stock Z. What are the weighted exposures to risk factor 1 and 2 for this portfolio? And how much net arbitrage profit you can gain from this position? Show your calculations. e. Find the new prices now for stocks X,Y, and Z that will not allow for arbitrage profits. Case 2. Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas) and expected dividends. The zero-beta return (b0)=3%, and the risk premia are I1=8%,I2=12%. Assume that all three stocks are currently priced at $40. a. What are the expected returns for stock X, stock Y, and stock Z ? Enter your answer as a percent with 1 decimal (i.e. 5.2\%). Expected Return for Stock X Expected Return for Stock Y b. What are the expected prices one year from now for stocks X,Y, and Z ? Enter your answer as a dollar amount with 2 decimals (i.e. $25.66 ). Expected Price for Stock X Expected Price for Stock Y Expected Price for Stock Z c. If you know that the actual prices one year from now are stock X$55, stock Y$52, and stock Z$57, then which of the stocks are undervalued and which are overvalued? (Enter undervalued or overvalued) Stock X is Stock Y is Stock Z is are overvalued? (Enter undervalued or overvalued) Stock X is Stock Y is Stock Z is Case 2 (continued). d. Assume that you wish to create a portfolio with no net wealth invested. The portfolio that achieves this has 50% in stock X,100% in stock Y, and 50% in stock Z. What are the weighted exposures to risk factor 1 and 2 for this portfolio? And how much net arbitrage profit you can gain from this position? Show your calculations. e. Find the new prices now for stocks X,Y, and Z that will not allow for arbitrage profits