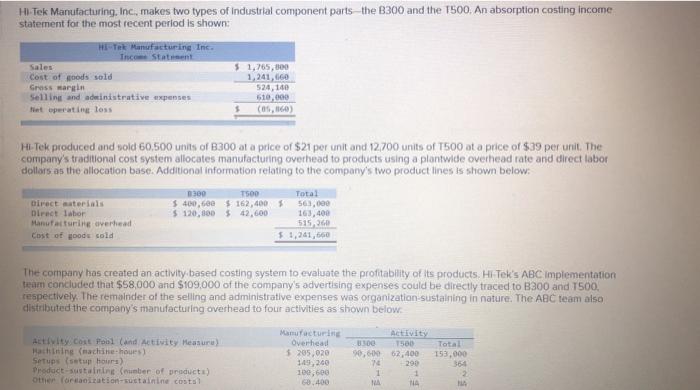

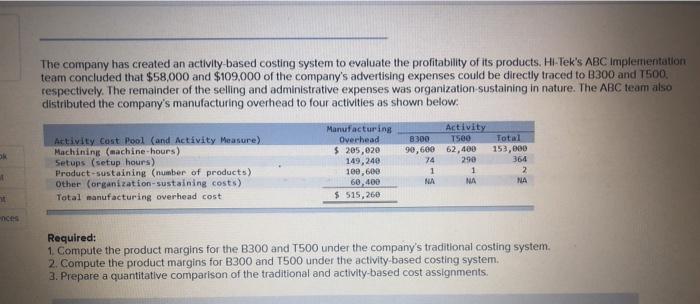

Hi-Tek Manufacturing, Inc, makes two types of Industrial component parts the 1300 and the 1500. An absorption costing income statement for the most recent period is shown HET Manufacturing Inc. Inco Staten Sales $ 1,765,500 Cost of nods sold 1,241,60 Grass margin 524,140 Selling and administrative expenses 510,000 Net operating loss (05, 1160) Hi-Tek produced and sold 60,500 units of 300 at a price of $21 por unit and 12,700 units of T500 at a price of $39 per unit. The company's traditional cost system allocates manufacturing overhead to products using a plontwide overhead rate and direct labor dollors as the allocation base. Additional information relating to the company's two product lines is shown below. 0300 T500 Total Direct materials $ 400,60 $ 162,4005 561,000 Direct labor $ 120,000 $ 42,600 163,400 Manufacturing overhead 515,260 Cost of BDO cold $1,241,660 The company has created an activity based costing system to evaluate the profitability of its products. Hi Tek's ABC implementation team concluded that $58,000 and $109,000 of the company's advertising expenses could be directly traced to B300 and T500, respectively. The remainder of the selling and administrative expenses was organization-sustaining in nature. The ABC team also distributed the company's manufacturing overhead to four activities as shown below. 90,00 Activity Cost Pool (and Activity Measuru) Machine (machine-hous) Setups (setup hours) Product-sustainine (number of products) Other foretation sustaining costs Manufacturing Overhead $ 205,020 149,240 100,600 68.400 Activity 1500 Total 62,400 153,000 290 1 TA 1 The company has created an activity based costing system to evaluate the profitability of its products. Hi-Tek's ABC implementation team concluded that $58,000 and $109,000 of the company's advertising expenses could be directly traced to $300 and T500 respectively. The remainder of the selling and administrative expenses was organization-sustaining in nature. The ABC team also distributed the company's manufacturing overhead to four activities as shown below: Activity Cost Pool (and Activity Measure) Machining (machine-hours) Setups (setup hours) Product-sustaining (number of products) Other (organization-sustaining costs) Total manufacturing overhead cost Manufacturing Overhead $ 205,020 149,240 100,600 60,400 $ 515,260 Activity 8300 T500 90,600 62,400 74 290 1 1 NA NA Total 153,000 364 2 NA ances Required: 1. Compute the product margins for the B300 and 1500 under the company's traditional costing system. 2. Compute the product margins for B300 and T500 under the activity-based costing system. 2. Prepare a quantitative comparison of the traditional and activity-based cost assignments