Answered step by step

Verified Expert Solution

Question

1 Approved Answer

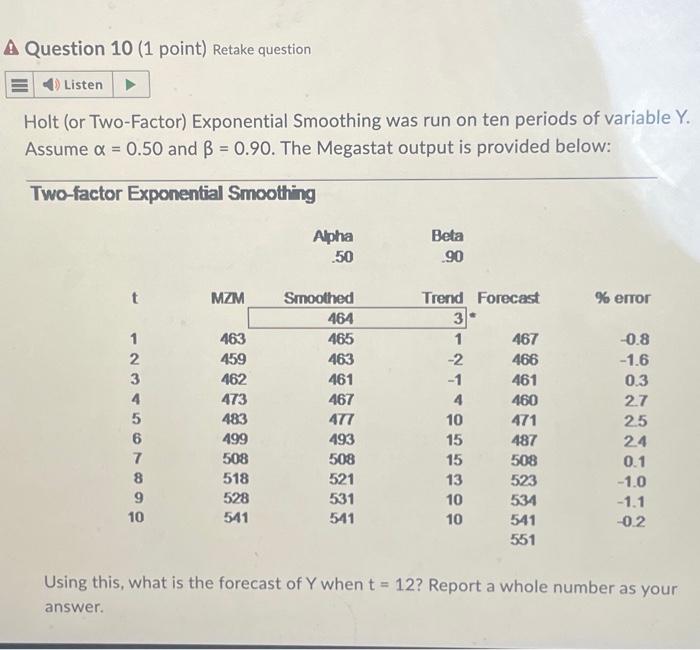

Holt (or Two-Factor) Exponential Smoothing was run on ten periods of variable Y. Assume x = 0.50 and B = 0.90. The Megastat output is

Holt (or Two-Factor) Exponential Smoothing was run on ten periods of variable Y. Assume x = 0.50 and B = 0.90. The Megastat output is provided below: Two-factor Exponential Smoothing 1234567890 MZM 463 459 462 473 483 499 508 518 528 541 Alpha ..50 Smoothed 464 465 463 461 467 477 493 508 521 531 541 Beta 90 Trend Forecast 3* 1 -2 -1 4 10 15 15 13 10 10 467 466 461 460 471 487 508 523 534 541 551 % error -0.8 -1.6 0.3 27 2.5 2.4 0.1 -1.0 -1.1 -0.2 Using this, what is the forecast of Y when t = 12? Report a whole number as your answer.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Funds Private Equity Hedge And All Core Structures

Authors: Matthew Hudson

1st Edition

1118790405, 978-1118790403