How do you solve this please?

I am trying to solve it and I'd like a detailed explanation!

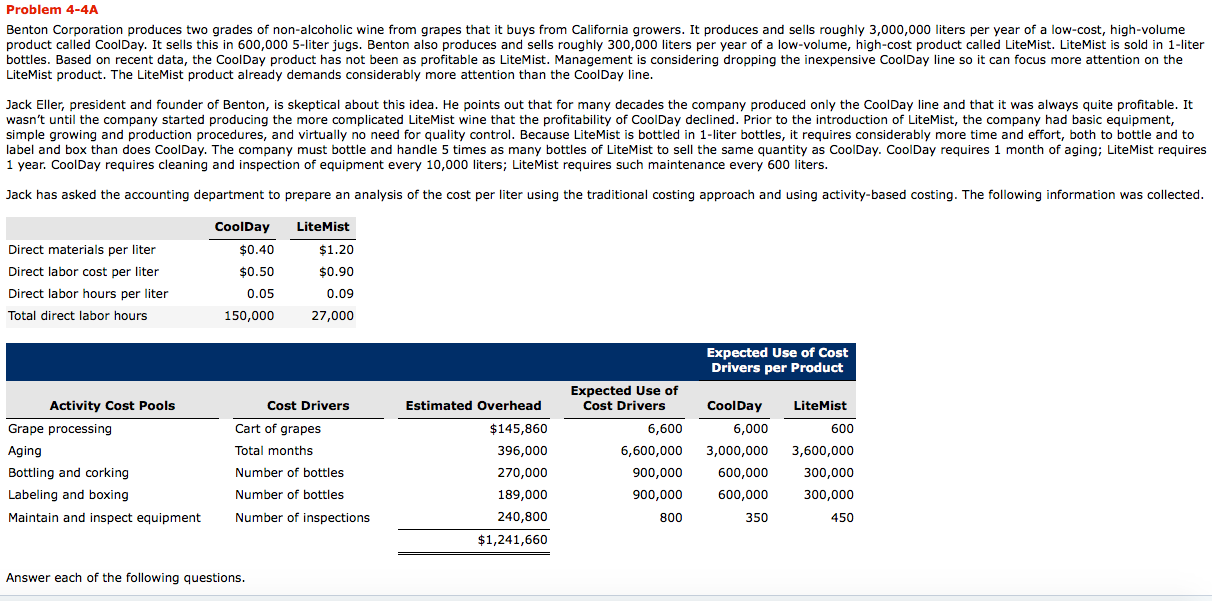

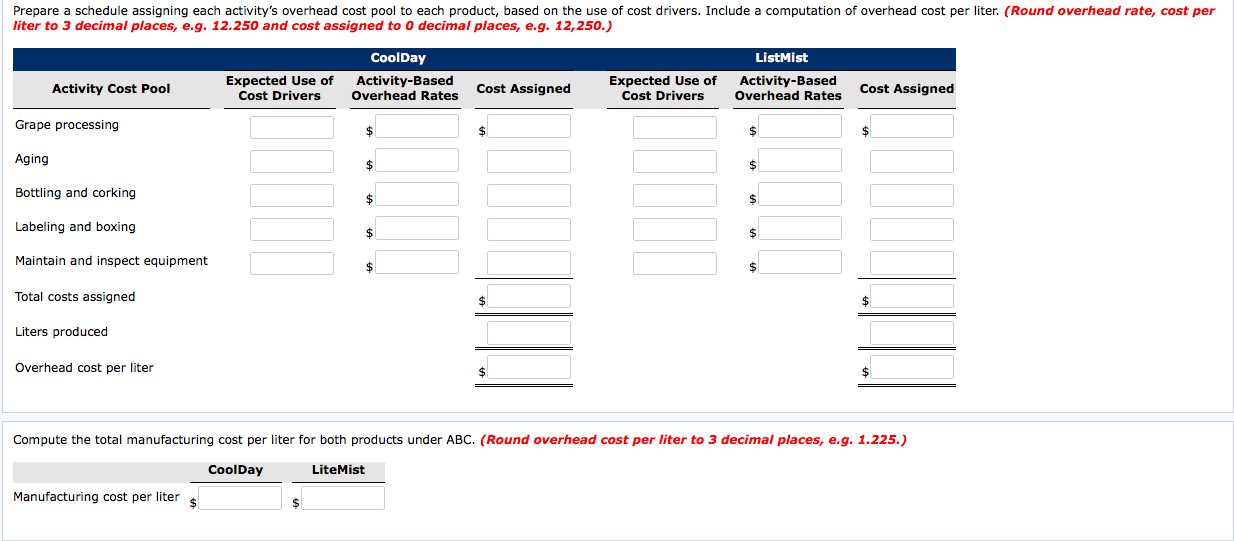

Benton Corporation produces two grades of non-alcoholic wine from grapes that it buys from California growers. It produces and sells roughly 3,000,000 liters per year of a low-cost, high-volume product called CoolDay. It sells this in 600,000 5-liter jugs. Benton also produces and sells roughly 300,000 liters per year of a low-volume, high-cost product called LiteMist. LiteMist is sold in 1-liter bottles. Based on recent data, the CoolDay product has not been as profitable as LiteMist. Management is considering dropping the inexpensive CoolDay line so it can focus more attention on the LiteMist product. The LiteMist product already demands considerably more attention than the CoolDay line.

Jack Eller, president and founder of Benton, is skeptical about this idea. He points out that for many decades the company produced only the CoolDay line and that it was always quite profitable. It wasn't until the company started producing the more complicated LiteMist wine that the profitability of CoolDay declined. Prior to the introduction of LiteMist, the company had basic equipment, simple growing and production procedures, and virtually no need for quality control. Because LiteMist is bottled in 1-liter bottles, it requires considerably more time and effort, both to bottle and to label and box than does CoolDay. The company must bottle and handle 5 times as many bottles of LiteMist to sell the same quantity as CoolDay. CoolDay requires 1 month of aging; LiteMist requires 1 year. CoolDay requires cleaning and inspection of equipment every 10,000 liters; LiteMist requires such maintenance every 600 liters.

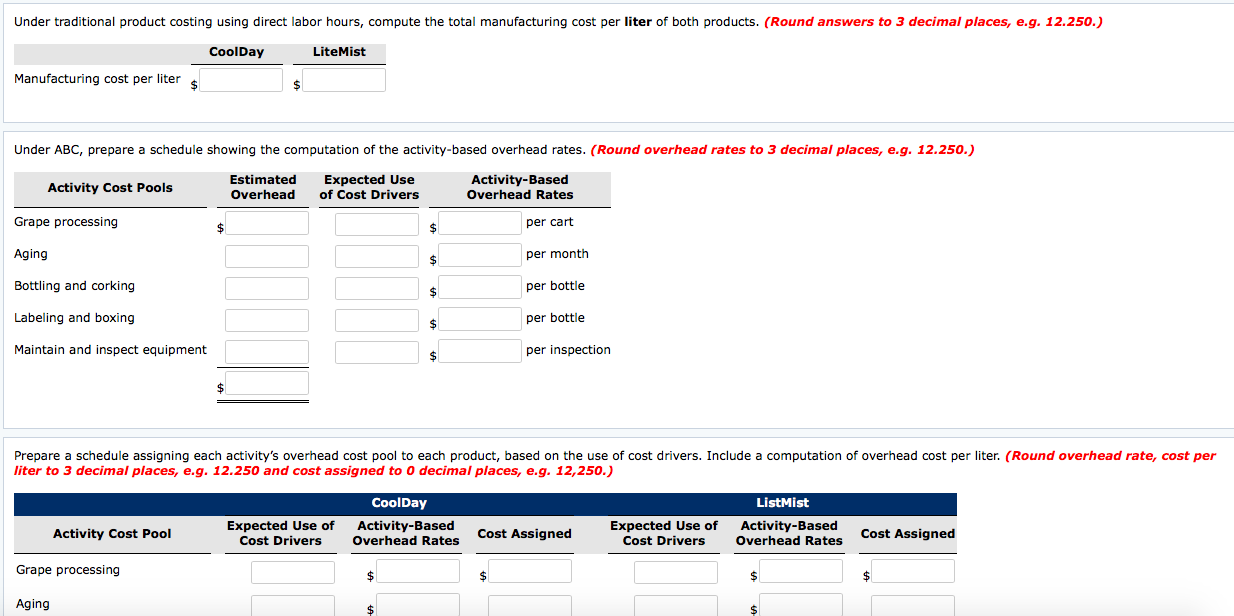

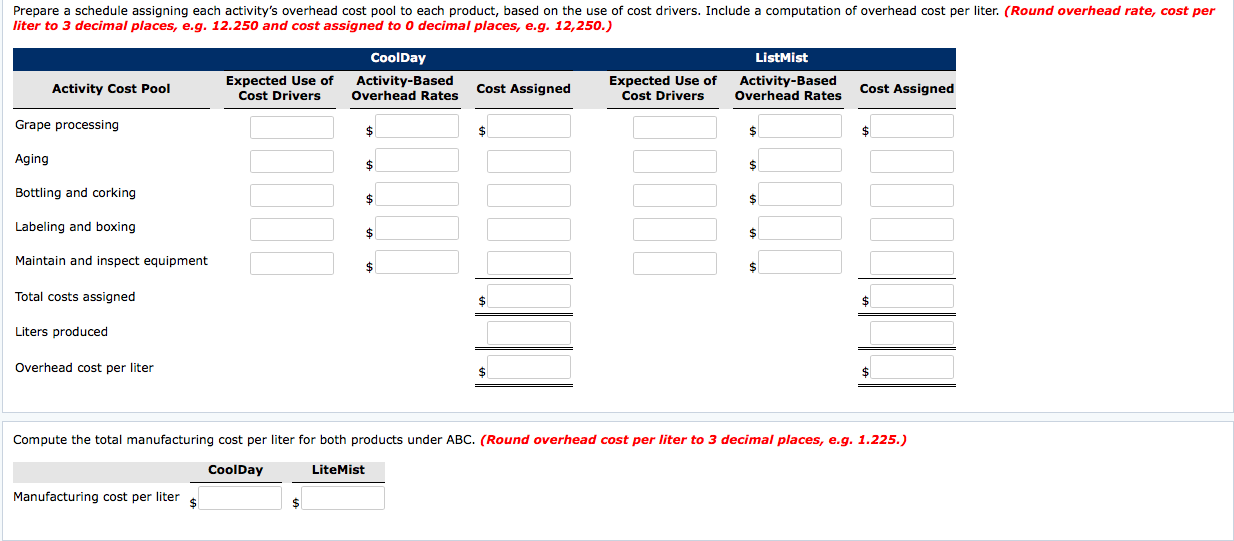

Jack has asked the accounting department to prepare an analysis of the cost per liter using the traditional costing approach and using activity-based costing. The following information was collected.

Problem 4-\" Benton Corporation produces two grades of non-alcohollc wine from grapes that it buys from California growers. It produces and sells roughly 3,000,000 llters per year of a low-cost, hlgh-yolume product called CoolDay. It sells thls In 600,000 5literjugs. Benton also produces and sells roughly 300,000 liters per year of a low-volume, high-cost product called theMist. UteMlst is sold in 1-liter bottles. Based on recent data, the CoolDay product has not been as protable as UteMlst. Management ls conslderlng dropping the inexpensive CoolDay line so it can focus more attentlon on the theMlst product. The LiteMist product already demands considerably more attentlon than the CoolDay line. Jack Eller, president and founder of Benton, is skeptical about this idea. He points out that for many decades the company produced only the CoolDay line and that it was always qulte protable. It wasn't until the company started producing the more complicated LiteMist wine that the protabllity of CoolD'ay declined. Prlor to the lntroductlon 0f theMlst, the company had basic equipment, simple growing and production procedures, and virtually no need for quality control. Because UteMlst is bottled in l-llter bottles, lt requires conslderably more time and effort, both to bottle and to label and box than does CoolDay. The company must bottle and handle 5 tlmes as many homes of UteMlst to sell the same quantity as CoolDay. CoolDay requlres 1 month of aging: theMist requires 1 year. CoolDay requires cleanlng and inspectlon of equipment every 10,000 liters: theMist requires such n'ialntenance every 600 llters. Jack has asked the accounting department to prepare an analysis of the amt per liter uslng the traditional costlng approach and using activlty-based costing. The followlng information was collected. CooIDay Libellisl: Direct materials per liter $0.40 $1.20 Direct labor cost per liter $0.50 $0.90 Direct labor hours per llter 0.05 0.09 Total direct labor hours 150,000 2?,000 D ers per Product Expected Use of Aclivlty Oust Pools Oust Drivers Estimated Overhead Cent Drlwen ObolDay Ll'llellist Grape processing Cart of grapes $145,860 6,600 6,000 600 Alglng Total months 396,000 6,600,000 3,000,000 3,600,000 Bottling and wrking Number of bottles 270,000 900,000 500,000 300,000 Labellng and boxing Number of bottles 189,000 900,000 600,000 300,000 Maintain and Inspect equlpn'ient Number of inspectlons 240,800 800 350 450 $1,241,660 Answer each of the following quatlons. Under traditlonal product costing uslng dlrect labor hours, compute the total manufacturing cost per liter of both products. (Round answers to 3 decimal places, e.g. 12.250.) CuaIDIy leellt Manufacturing cost per liter 5 5 Under ABC, prepare a schedule showing the computation of the activity-based overhead rates. (Round overhead rates to 3 decimal places, 2.9. 12.250.) mm...m.. Ems\": isms; Mummies. Grape processing $ $ per cart Aglng $ per month Bottling and corking $ per bottle Lapellng and boxing $ per bottle Maintain and Inspect equlpment 5 per inspectlon $ Prepare a schedule asslgning each activlty's overhead cost pool to each product, based on the use of cost drivers. Include a computatlon of overhead cost per liter. (Round overhead rate, cost per Mar to 3 decimal places, 2.9. 12.25:: and cast assigned to 0 decimal places, 9.9. 12,250.) CoalDay ListMist Expected Use of Activity-Bum! Expected Use of Why-Based Mthrl'ly M MI Cull: Driver! Overhead Rah: M Assigned Call: Driven Overhead Rate: Celt mulled Grape processing $ 5 S $ AIglng I I $I I I I I SI I I I Prepare a schedule assigning each attiwty's overhead cost pool to each product, based on the use of cost drivers. Include a computation of overhead cost per liter. (Round overhead rate, cost per mer- to 3 decimal places, e.r. 12.250 and cast assigned to 0 decimal places, 2.9. 12,250.) COOIDBVJIr Li stMist Expected Use ef Activity-Bleed Expected Use of Ae'vltyBeled \"mm" M M' non Drivel-I overhead Ram M \"\"9\"\" Cost Drivers Overhead Rate: a\": \"\"9"\"! Grape processing $ $ $ $ \"9""! $ s Bottling and cor-King $ $ Labeling and boxing $ $ Maintain and inspect equipment $ $ Total costs assigned 5 $ Liters produced Overhead cost per liter 5 $ Compute the total manufacturing cost per liter For both producm under ABC. {Round overhead cast per liter to 3 decimal places, e.g. 1.225.} CnolDay Llliellllt Manufacturing cost per liter 5 5