Answered step by step

Verified Expert Solution

Question

1 Approved Answer

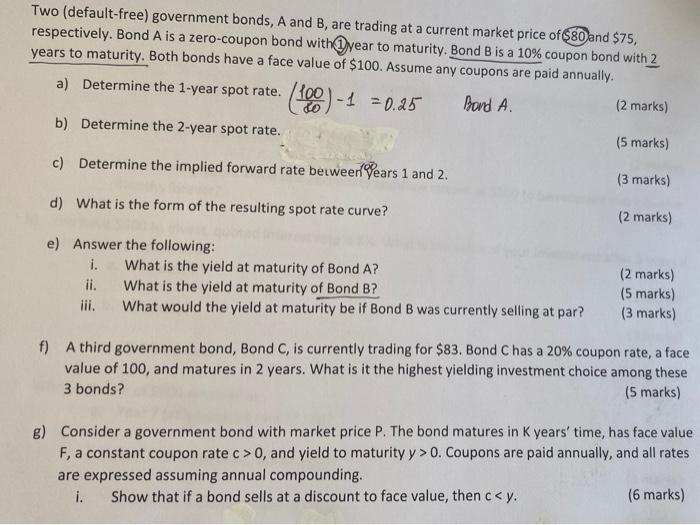

How to solve part e iii), f, g? Two (default-free) government bonds, A and B, are trading at a current market price of $80 and

How to solve part e iii), f, g?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quantitative Fund Management

Authors: M.A.H. Dempster, Gautam Mitra , Georg Pflug

1st Edition

1420081918,1420081926