I. About the Module The method of payment determines how payment is going to be made, i.e., the obligations that rest with both buyer and

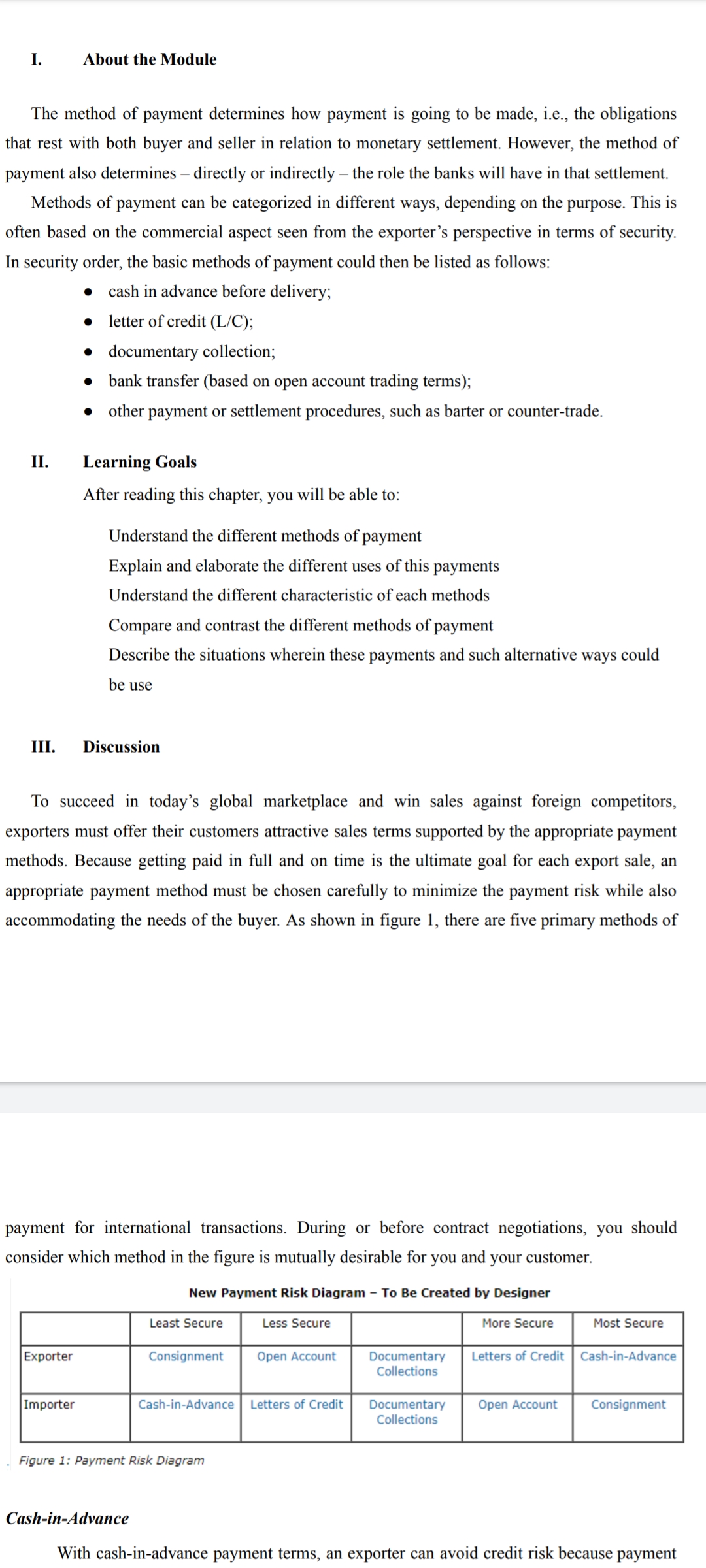

I. About the Module The method of payment determines how payment is going to be made, i.e., the obligations that rest with both buyer and seller in relation to monetary settlement. However, the method of payment also determines directly or indirectly the role the banks will have in that settlement, Methods of payment can be categorized in different ways, depending on the purpose, This is often based on the commercial aspect seen from the exporter's perspective in terms of security. In security order, the basic methods of payment could then be listed as follows: 0 cash in advance before delivery; o letter of credit (MC); 0 documentary collection; 0 bank transfer (based on open account trading terms); 0 other payment or settlement procedures, such as barter or countertrade. 11. Learning Goals After reading this chapter, you will be able to: Understand the different methods of payment Explain and elaborate the different uses of this payments Understand the different characteristic of each methods Compare and contrast the different methods of payment Describe the situations wherein these payments and such alternative ways could be use Ill. Discussion To succeed in today's global marketplace and win sales against foreign competitors, exporters must offer their customers attractive sales terms supported by the appropriate payment methods. Because getting paid in full and on time is the ultimate goal for each export sale, an appropriate payment method must be chosen carefully to minimize the payment risk while also accommodating the needs ofthe buyer. As shown in gure 1. there are ve primary methods of payment for international transactions. During or before contract negotiations, you should consider which method in the gure is mutually desirable for you and your customer New Pavment Risk Diagram To Be Created by Designer Exporter Consignment Open Account Documentarw Letters of Credit Cash-in-Advance Collections Importer Cash-in-Advance Letters of Credit Documentary Oper' Account Consignment Collections Figure 1: Payment RfSk Diagram Cash-in-A dvnnce With cash~in-advance payment terms, an exporter can avoid credit risk because payment Cash-in-A (ivrmce With cash-in-advance payment terms, an exporter can avoid credit risk because payment is received before the ownership of the goods is transferred. For international sales, wire transfers and credit cards are the most commonly used cash-in-advance options available to exporters. With the advancement of the lntemet, escrow services are becoming another cash-in-advance option for small export transactions. However, requiring payment in advance is the least attractive option for the buyer, because it creates unfavorable cash ow. Foreign buyers are also concerned that the goods may not be sent if payment is made in advance. Thus, exporters who insist on this payment method as their sole manner ofdoing business may lose to competitors who offer more attractive payment terms. Letters of Credit Letters of credit (LCs) are one of the most secure instruments available to international traders. An LC is a commitment by a bank on behalf ofthe buyer that payment will be made to the exporter, provided that the terms and conditions stated in the LC have been met, as verified through the presentation of all required documents. The buyer establishes credit and pays his or her bank to render this service. An LC is useful when reliable credit information about a foreign buyer is difficult to obtain, but the exporter is satised with the creditworthiness of the buyer's foreign bank. An LC also protects the buyer since no payment obligation arises until the goods have been shipped as promised. Documentary Collections A documentary collection (D/C) is a transaction whereby the exporter entrusts the collection ofthe payment for a sale to its bank (remitting bank), which sends the documents that its buyer needs to the importer's bank (collecting bank), with instructions to release the documents to the buyer for payment. Funds are received from the importer and remitted to the exporter through the banks involved in the collection in exchange for those documents. D/Cs involve using a draft that requires the importer to pay the face amount either at sight (document against payment) or on a specied date (document against acceptance). The collection letter gives instructions that specify the documents required for the transfer of title to the goods. Although banks do act as facilitators for their clients, D/Cs offer no verification process and limited recourse in the event of non-payment. D/Cs are generally less expensive than LCs. Open Account An open account transaction is a sale where the goods are shipped and delivered before payment is due, which in international sales is typically in 30, 60 or 90 days. Obviously, this is one of the most advantageous options to the importer in terms of cash flow and cost, but it is consequently one of the highest risk options for an exporter. Because of intense competition in export markets, foreign buyers often press exporters for open account terms since the extension of credit by the seller to the buyer is more common abroad. Therefore, exporters who are reluctant to extend credit may lose a sale to their competitors. Exporters can offer competitive open account terms while substantially mitigating the risk of non-payment by using one or more of the appropriate trade finance techniques covered later in this Guide. When offering open account terms, the exporter can seek extra protection using export credit insurance. reluctant to extend credit may lose a sale to their competitors. Exporters can offer competitive open account terms while substantially mitigating the risk of non-payment by using one or more of the appropriate trade finance techniques covered later in this Guide. When offering open account terms, the exporter can seek extra protection using export credit insurance. Consignment Consignment in international trade is a variation of open account in which payment is sent to the exporter only after the goods have been sold by the foreign distributor to the end customer. An international consignment transaction is based on a contractual arrangement in which the foreign distributor receives, manages, and sells the goods for the exporter who retains title to the goods until they are sold. Clearly, exporting on consignment is very risky as the exporter is no guaranteed any payment and its goods are in a foreign country in the hands of an independent distributor or agent. Consignment helps exporters become more competitive on the basis of better availability and faster delivery of goods. Selling on consignment can also help exporters reduce the direct costs of storing and managing inventory. The key to success in exporting on consignment is to partner with a reputable and trustworthy foreign distributor or a third-party logistics provider. Appropriate insurance should be in place to cover consigned goods in transit or in possession of a foreign distributor as well as to mitigate the risk of non-payment. IV. Generalization International trade presents a spectrum of risk, which causes uncertainty over the timing of payments between the exporter (seller) and importer (foreign buyer). For exporters, any sale is a gift until payment is received. Therefore, exporters want to receive payment as soon as possible, preferably as soon as an order is placed or before the goods are sent to the importer. For importers, any payment is a donation until the goods are received. Therefore, importers want to receive the goods as soon as possible but to delay payment as long as possible, preferably until after the goods are resold to generate enough to pay the exporter. 5/6 . . V. Summative Assessment What conclusions can you make from the following statements? 1. What's a letter of credit? How much does it cost to open one? What are the different kinds of letter of credit? 2. What's the difference between a confirmed letter of credit and one that isn't? What does it mean to say that a letter of credit is "advised" or "negotiated" through a particular bank? 3. What's export credit insurance? Who offers it? How much does it cost? 4. What's open account payment? Is it used internationally? 5. What's a SWIFT payment? Is it swift? 6. How do you deal with currency risk in international transactions? 7. What's the difference between a "standby credit" and a "commercial credit"

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance