Answered step by step

Verified Expert Solution

Question

1 Approved Answer

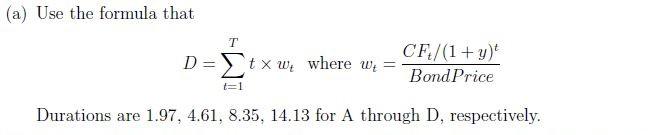

I don't know why answers are 1.97, 4.61, 8.35, 14.13. Please show me how to solve. You have just been given the following bond portfolio:

I don't know why answers are 1.97, 4.61, 8.35, 14.13. Please show me how to solve.

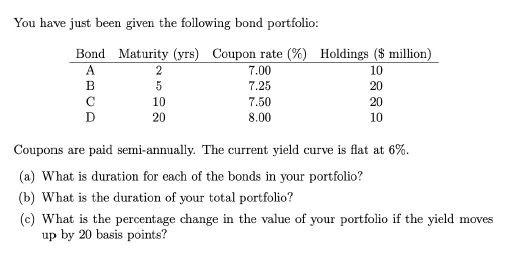

You have just been given the following bond portfolio: Bond Maturity (yrs) Coupon rate (%) Holdings ($ million) A B D 8.00 10 7.00 7.25 2 5 10 20 10 20 20 7.50 Coupons are paid semi-annually. The current yield curve is flat at 6%. (a) What is duration for each of the bonds in your portfolio? (b) What is the duration of your total portfolio? (e) What is the percentage change in the value of your portfolio if the yield moves up by 20 basis points? (a) Use the formula that T D = CF/(1+y) t x w where we = Bond Price t=1 Durations are 1.97, 4.61, 8.35, 14.13 for A through D, respectivelyStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: Jack Kapoor, Les Dlabay, Robert J. Hughes

11th edition

9781259278617, 77861647, 1259278611, 978-0077861643