i need anwser

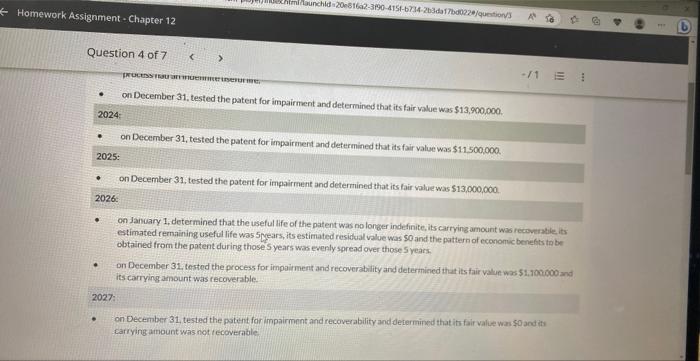

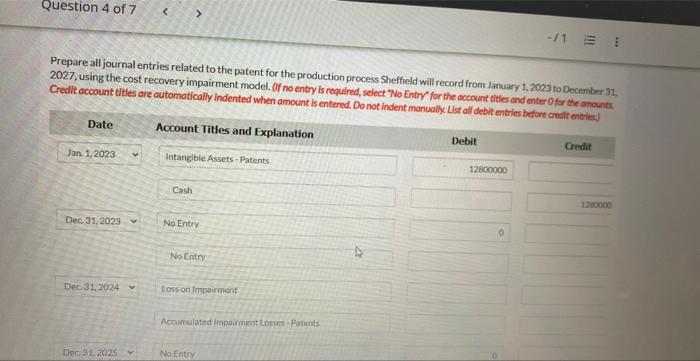

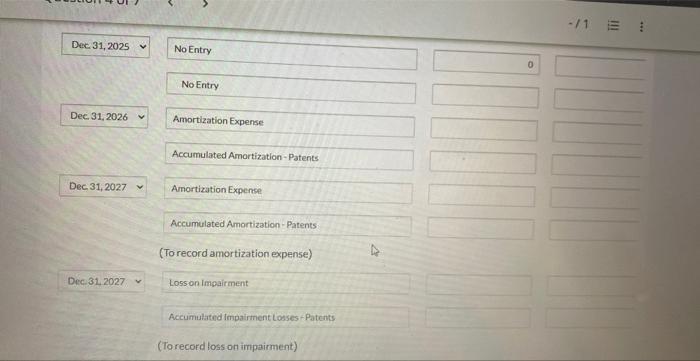

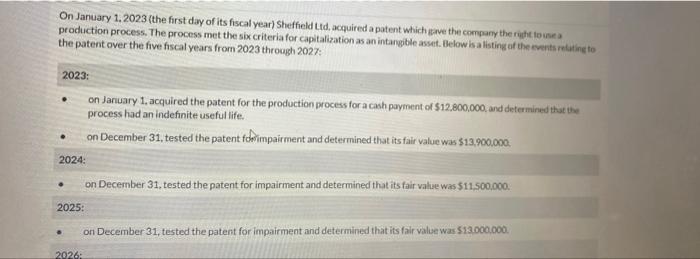

On January 1.2023 (the first day of its fiscal year) Sheifield tid, acquired a patent which gave the company the rupht to use a production process. The process met the sib criteria for capitalization as an intangible asset. Belowis alisting at the events reluting to the patent over the five fiscal years from 2023 throogh 2027 2023 - on Janiuary 1, acquired the patent for the production process for a cash payment of $12,800,000, and determined that the process had an indefinite useful life. - on December 31, tested the patent fonimpairment and determined that its fair value was $13,900,000. 2024: - on December 31, tested the patent for impairment and determined that its fair value was $11.500,000. 2025: - on December 31, tested the patent for impairment and determined that its fair value was $13000.000. 2026: on December 31 , tested the potent for impairment and recoverability and determined that its fair valuewas \$0 and its Carrying amount was not tecoverable Prepare all journal entries related to the patent for the production process Sheffield will record from January 1,2023 to December 31 . 2027, using the cost recovery impairment model. Of no entry is requilred, select "No Entry" for the account titles and enter 0 for the amounts. Credit account tittes are outomatically indented when amount is entered, Do not indent manually. List all debit entries before areelit ansiles is. On January 1.2023 (the first day of its fiscal year) Sheifield tid, acquired a patent which gave the company the rupht to use a production process. The process met the sib criteria for capitalization as an intangible asset. Belowis alisting at the events reluting to the patent over the five fiscal years from 2023 throogh 2027 2023 - on Janiuary 1, acquired the patent for the production process for a cash payment of $12,800,000, and determined that the process had an indefinite useful life. - on December 31, tested the patent fonimpairment and determined that its fair value was $13,900,000. 2024: - on December 31, tested the patent for impairment and determined that its fair value was $11.500,000. 2025: - on December 31, tested the patent for impairment and determined that its fair value was $13000.000. 2026: on December 31 , tested the potent for impairment and recoverability and determined that its fair valuewas \$0 and its Carrying amount was not tecoverable Prepare all journal entries related to the patent for the production process Sheffield will record from January 1,2023 to December 31 . 2027, using the cost recovery impairment model. Of no entry is requilred, select "No Entry" for the account titles and enter 0 for the amounts. Credit account tittes are outomatically indented when amount is entered, Do not indent manually. List all debit entries before areelit ansiles is