Answered step by step

Verified Expert Solution

Question

1 Approved Answer

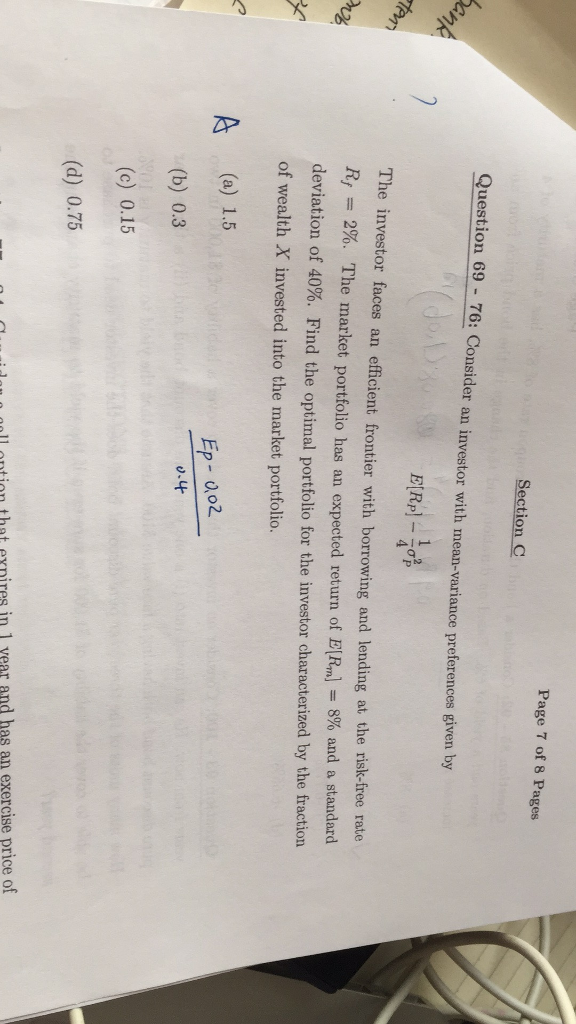

I need calculation step by step. Thank you! Consider an investor with mean-variance preferences given by E [R_P] - 1/4 sigma^2 _P The investor faces

I need calculation step by step. Thank you!

Consider an investor with mean-variance preferences given by E [R_P] - 1/4 sigma^2 _P The investor faces an efficient frontier with borrowing and lending at the risk-free rate R_f = 2%. The market portfolio has an expected return of E[R_m] = 8% and a standard deviation of 40%. Find the optimal portfolio for the investor characterized by the fraction of wealth X invested into the market portfolio. 1.5 0.3 0.15 0.75Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Routledge Handbook Of Integrated Reporting

Authors: Charl De Villiers, Warren Maroun, Pei-Chi Hsiao

1st Edition

0367233851, 978-0367233853