Answered step by step

Verified Expert Solution

Question

1 Approved Answer

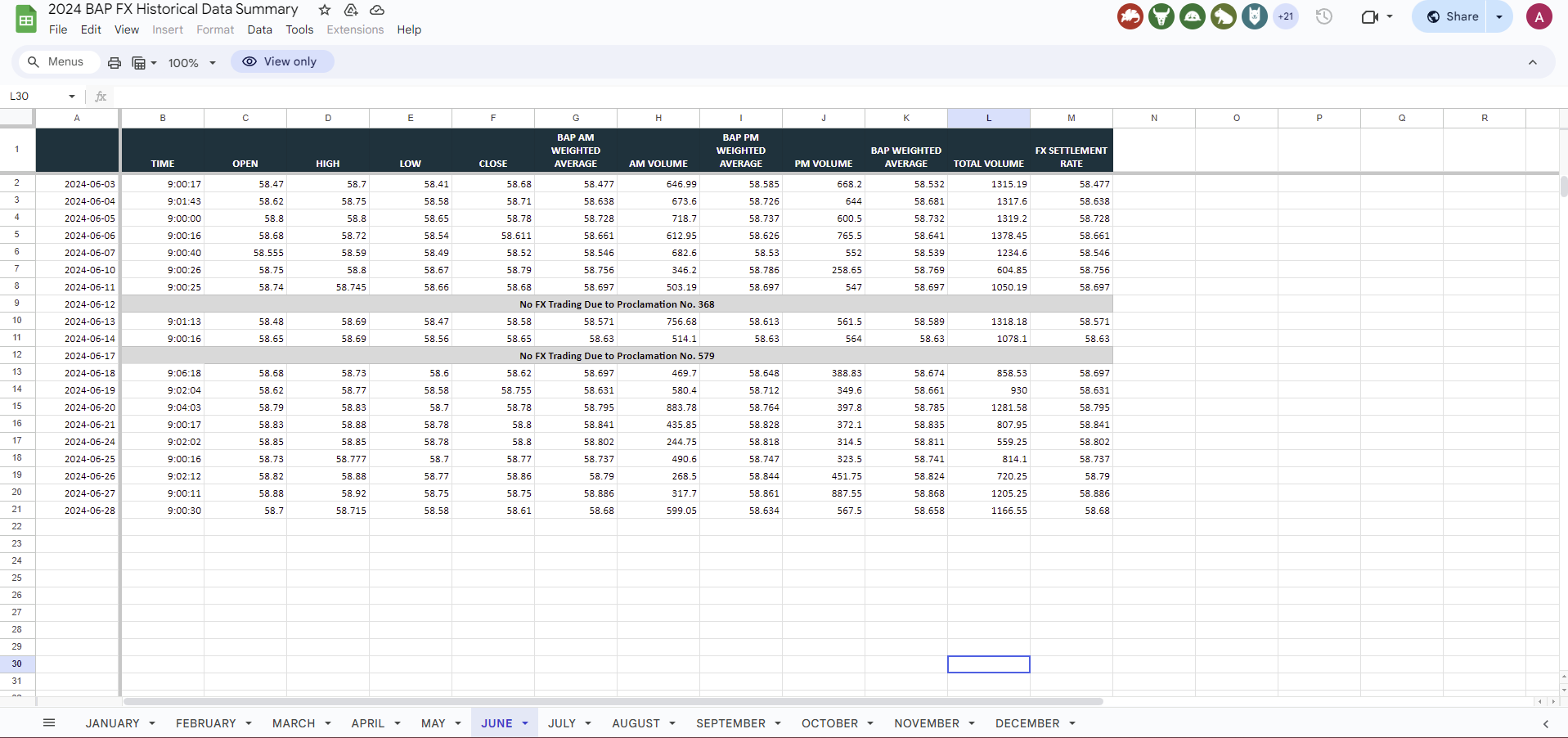

If a portfolio as of 3 0 June 2 0 2 4 includes USD cash of 1 0 , 0 0 0 , 0 0

If a portfolio as of June includes USD cash of at the level of confidence, how much can it possibly lose from a single day?

a If we want to reduce the potential loss to PHP would it be appropriate to reduce the amount of USD holdings? If so what asset class should we move the amount to Hint: recall coherent risk measures specifically translation invariance.

b Will the reduction in USD holdings also potentially reduce the possible upside?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Sustainability Proceedings From The Finance And Sustainability Conference Wroclaw 2017

Authors: Agnieszka Bem, Karolina Daszy?ska-?ygad?o , Ta?ána Hajdíková, Péter Juhász

1st Edition

3319922270,3319922289