Answered step by step

Verified Expert Solution

Question

1 Approved Answer

If Mel decided to sell the vacation property today for the Fair Market Value, what would his gain or loss be? (Value - 10 points)

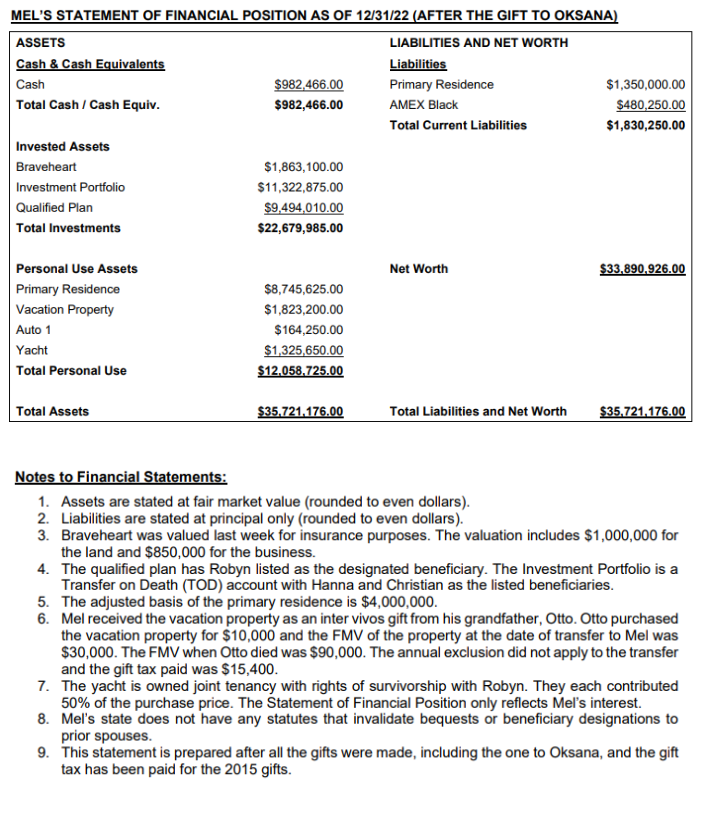

If Mel decided to sell the vacation property today for the Fair Market Value, what would his gain or loss be? (Value - 10 points) Notes to Financial Statements: 1. Assets are stated at fair market value (rounded to even dollars). 2. Liabilities are stated at principal only (rounded to even dollars). 3. Braveheart was valued last week for insurance purposes. The valuation includes $1,000,000 for the land and $850,000 for the business. 4. The qualified plan has Robyn listed as the designated beneficiary. The Investment Portfolio is a Transfer on Death (TOD) account with Hanna and Christian as the listed beneficiaries. 5. The adjusted basis of the primary residence is $4,000,000. 6. Mel received the vacation property as an inter vivos gift from his grandfather, Otto. Otto purchased the vacation property for $10,000 and the FMV of the property at the date of transfer to Mel was $30,000. The FMV when Otto died was $90,000. The annual exclusion did not apply to the transfer and the gift tax paid was $15,400. 7. The yacht is owned joint tenancy with rights of survivorship with Robyn. They each contributed 50% of the purchase price. The Statement of Financial Position only reflects Mel's interest. 8. Mel's state does not have any statutes that invalidate bequests or beneficiary designations to prior spouses. 9. This statement is prepared after all the gifts were made, including the one to Oksana, and the gift tax has been paid for the 2015 gifts. If Mel decided to sell the vacation property today for the Fair Market Value, what would his gain or loss be? (Value - 10 points) Notes to Financial Statements: 1. Assets are stated at fair market value (rounded to even dollars). 2. Liabilities are stated at principal only (rounded to even dollars). 3. Braveheart was valued last week for insurance purposes. The valuation includes $1,000,000 for the land and $850,000 for the business. 4. The qualified plan has Robyn listed as the designated beneficiary. The Investment Portfolio is a Transfer on Death (TOD) account with Hanna and Christian as the listed beneficiaries. 5. The adjusted basis of the primary residence is $4,000,000. 6. Mel received the vacation property as an inter vivos gift from his grandfather, Otto. Otto purchased the vacation property for $10,000 and the FMV of the property at the date of transfer to Mel was $30,000. The FMV when Otto died was $90,000. The annual exclusion did not apply to the transfer and the gift tax paid was $15,400. 7. The yacht is owned joint tenancy with rights of survivorship with Robyn. They each contributed 50% of the purchase price. The Statement of Financial Position only reflects Mel's interest. 8. Mel's state does not have any statutes that invalidate bequests or beneficiary designations to prior spouses. 9. This statement is prepared after all the gifts were made, including the one to Oksana, and the gift tax has been paid for the 2015 gifts

If Mel decided to sell the vacation property today for the Fair Market Value, what would his gain or loss be? (Value - 10 points) Notes to Financial Statements: 1. Assets are stated at fair market value (rounded to even dollars). 2. Liabilities are stated at principal only (rounded to even dollars). 3. Braveheart was valued last week for insurance purposes. The valuation includes $1,000,000 for the land and $850,000 for the business. 4. The qualified plan has Robyn listed as the designated beneficiary. The Investment Portfolio is a Transfer on Death (TOD) account with Hanna and Christian as the listed beneficiaries. 5. The adjusted basis of the primary residence is $4,000,000. 6. Mel received the vacation property as an inter vivos gift from his grandfather, Otto. Otto purchased the vacation property for $10,000 and the FMV of the property at the date of transfer to Mel was $30,000. The FMV when Otto died was $90,000. The annual exclusion did not apply to the transfer and the gift tax paid was $15,400. 7. The yacht is owned joint tenancy with rights of survivorship with Robyn. They each contributed 50% of the purchase price. The Statement of Financial Position only reflects Mel's interest. 8. Mel's state does not have any statutes that invalidate bequests or beneficiary designations to prior spouses. 9. This statement is prepared after all the gifts were made, including the one to Oksana, and the gift tax has been paid for the 2015 gifts. If Mel decided to sell the vacation property today for the Fair Market Value, what would his gain or loss be? (Value - 10 points) Notes to Financial Statements: 1. Assets are stated at fair market value (rounded to even dollars). 2. Liabilities are stated at principal only (rounded to even dollars). 3. Braveheart was valued last week for insurance purposes. The valuation includes $1,000,000 for the land and $850,000 for the business. 4. The qualified plan has Robyn listed as the designated beneficiary. The Investment Portfolio is a Transfer on Death (TOD) account with Hanna and Christian as the listed beneficiaries. 5. The adjusted basis of the primary residence is $4,000,000. 6. Mel received the vacation property as an inter vivos gift from his grandfather, Otto. Otto purchased the vacation property for $10,000 and the FMV of the property at the date of transfer to Mel was $30,000. The FMV when Otto died was $90,000. The annual exclusion did not apply to the transfer and the gift tax paid was $15,400. 7. The yacht is owned joint tenancy with rights of survivorship with Robyn. They each contributed 50% of the purchase price. The Statement of Financial Position only reflects Mel's interest. 8. Mel's state does not have any statutes that invalidate bequests or beneficiary designations to prior spouses. 9. This statement is prepared after all the gifts were made, including the one to Oksana, and the gift tax has been paid for the 2015 gifts Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Victorian Literature And Finance

Authors: Francis O'Gorman

1st Edition

0199281920, 978-0199281923