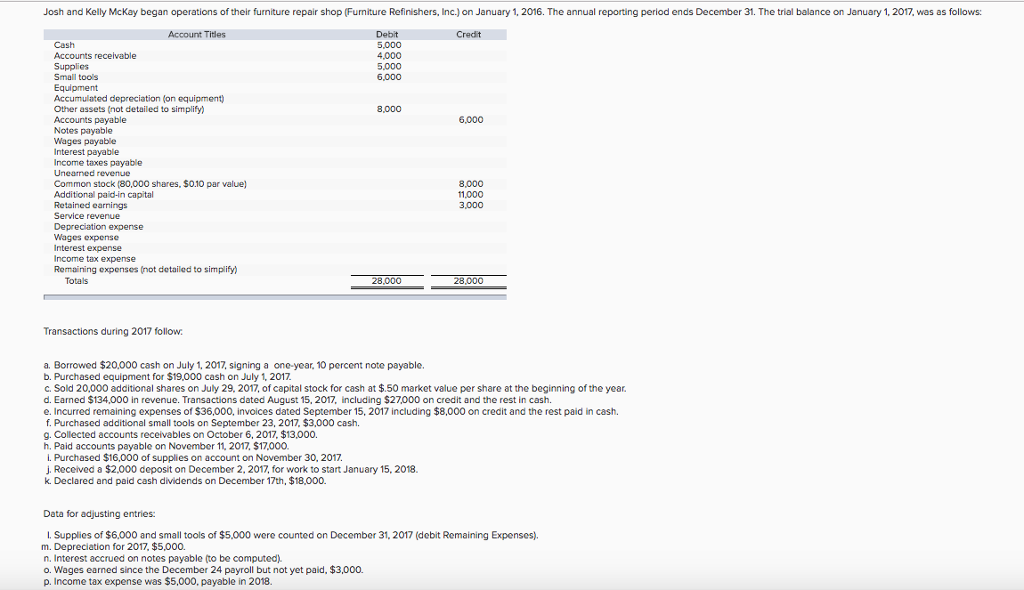

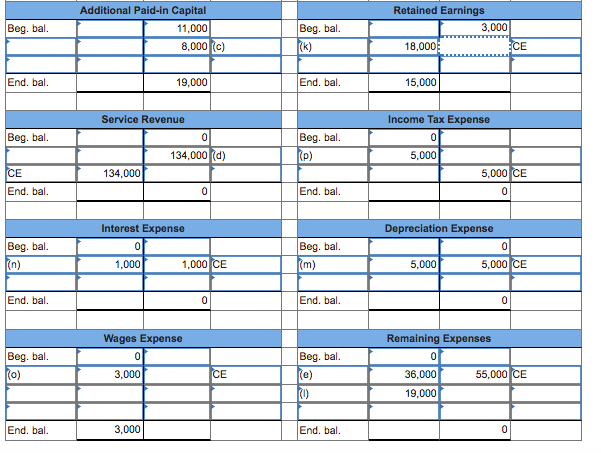

Question

I'm preparing closing entries for the accounts/transactions listed. I have zeroed out all of the closing entries with shown values, but have not been able

I'm preparing closing entries for the accounts/transactions listed. I have zeroed out all of the closing entries with shown values, but have not been able to find the correct CE for retained earnings or wages expense. Whatever the correct answer is, it is not the value that would zero out the account. How do I calculate these entries?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounts And Audit Of Limited Liability Partnerships

Authors: Steve Collings

4th Edition

1847669913, 978-1847669919