Answered step by step

Verified Expert Solution

Question

1 Approved Answer

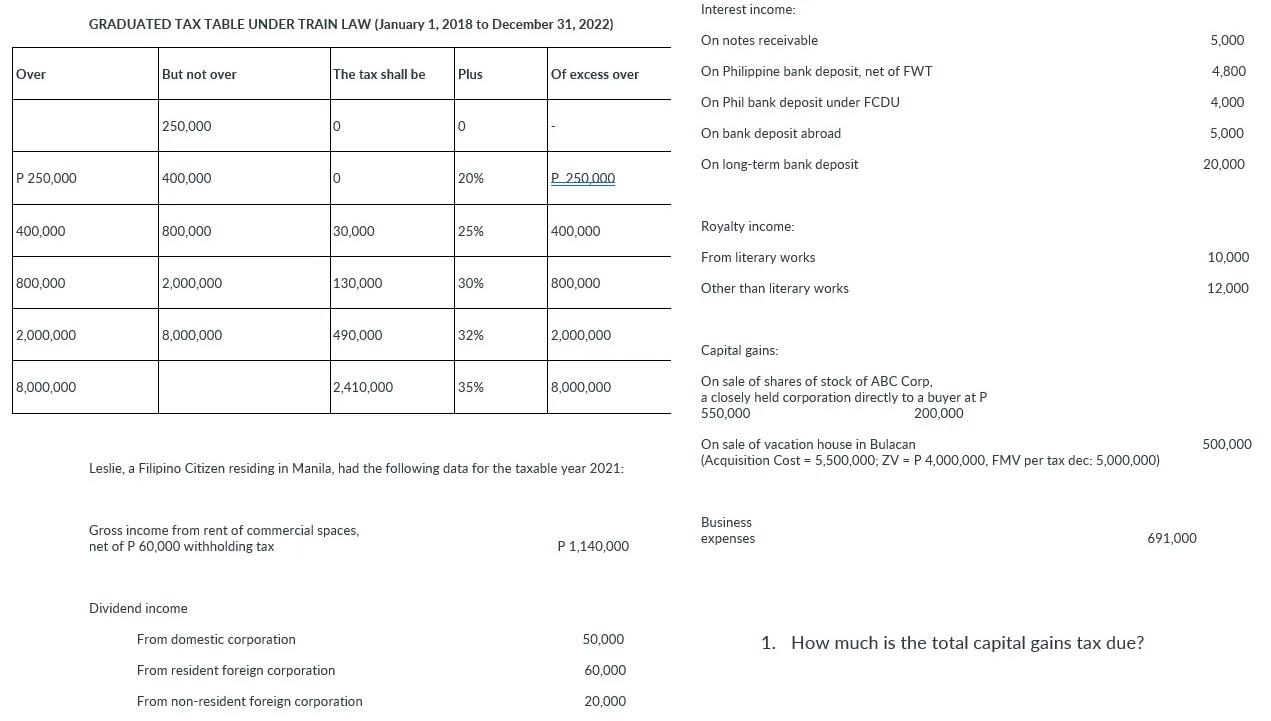

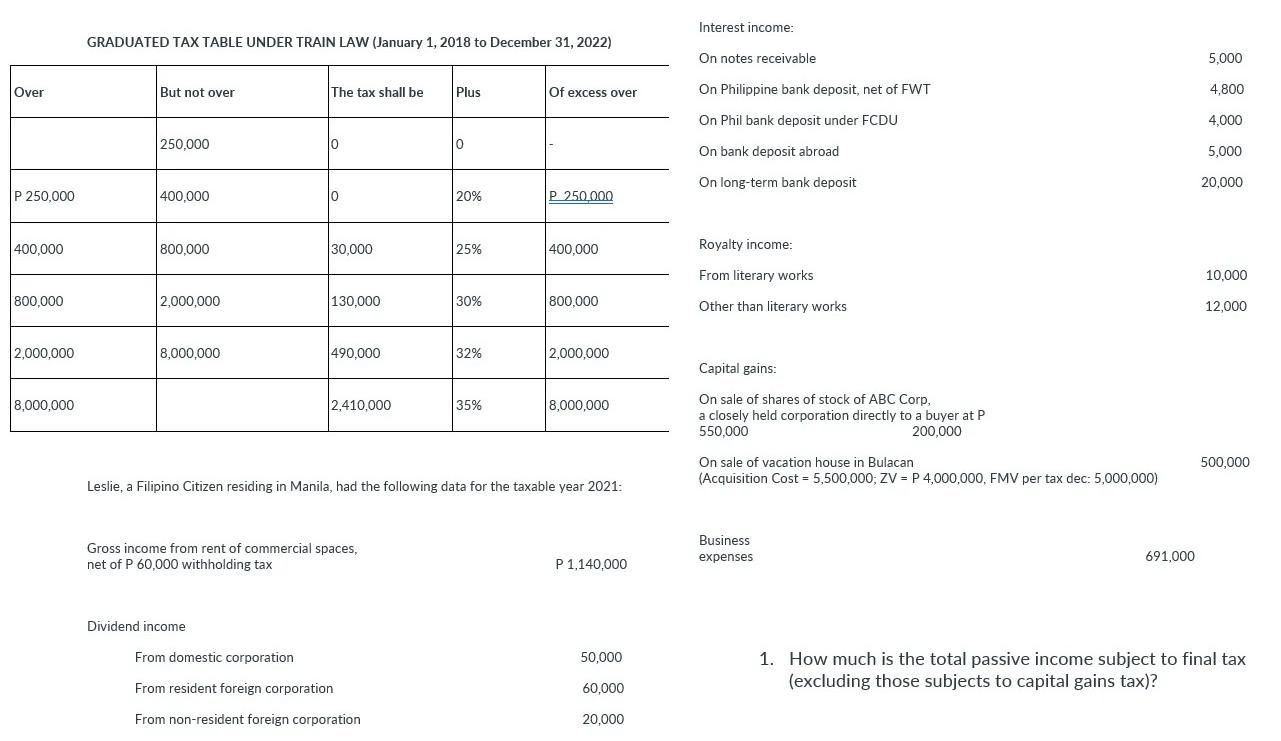

Interest income: GRADUATED TAX TABLE UNDER TRAIN LAW (January 1, 2018 to December 31, 2022) On notes receivable 5,000 Over But not over The tax

Interest income: GRADUATED TAX TABLE UNDER TRAIN LAW (January 1, 2018 to December 31, 2022) On notes receivable 5,000 Over But not over The tax shall be Plus Of excess over On Philippine bank deposit, net of FWT 4,800 4,000 250,000 On Phil bank deposit under FCDU On bank deposit abroad 10 0 5,000 On long-term bank deposit 20,000 P 250.000 400.000 0 0 20% P_250.000 400,000 800,000 30.000 25% 400,000 Royalty income: From literary works 10,000 800,000 2,000,000 130,000 30% 800,000 Other than literary works 12,000 2,000,000 8,000,000 490,000 32% 2,000,000 Capital gains: : 8,000,000 12,410,000 35% 8,000,000 On sale of shares of stock of ABC Corp, a closely held corporation directly to a buyer at P 550,000 200,000 On sale of vacation house in Bulacan (Acquisition Cost = 5,500,000; ZV = P 4,000,000, FMV per tax dec: 5,000,000) 500,000 Leslie, a Filipino Citizen residing in Manila, had the following data for the taxable year 2021: Gross income from rent of commercial spaces, net of P 60,000 withholding tax Business expenses 691,000 P 1,140,000 Dividend income From domestic corporation 50,000 1. How much is the total capital gains tax due? From resident foreign corporation 60,000 From non-resident foreign corporation 20,000 Interest income: GRADUATED TAX TABLE UNDER TRAIN LAW (January 1, 2018 to December 31, 2022) On notes receivable 5,000 Over But not over The tax shall be Plus Of excess over On Philippine bank deposit, net of FWT 4,800 On Phil bank deposit under FCDU 4,000 250,000 O 0 On bank deposit abroad 5,000 On long-term bank deposit 20,000 P 250,000 400.000 10 20% P. 250.000 400,000 800,000 30,000 25% 400,000 Royalty income: From literary works 10,000 800,000 2,000,000 130,000 30% 800,000 Other than literary works 12,000 2,000,000 8,000,000 490,000 32% 2,000,000 Capital gains: 8,000,000 2,410,000 35% 8,000,000 On sale of shares of stock of ABC Corp, a closely held corporation directly to a buyer at P 550,000 200,000 500,000 On sale of vacation house in Bulacan (Acquisition Cost = 5,500,000; ZV = P 4,000,000, FMV per tax dec: 5,000,000) Leslie, a Filipino Citizen residing in Manila, had the following data for the taxable year 2021: a Gross income from rent of commercial spaces, net of P 60,000 withholding tax Business expenses 691,000 P 1,140,000 Dividend income From domestic corporation 50,000 1. How much is the total passive income subject to final tax (excluding those subjects to capital gains tax)? From resident foreign corporation 60,000 From non-resident foreign corporation 20,000 Interest income: GRADUATED TAX TABLE UNDER TRAIN LAW (January 1, 2018 to December 31, 2022) On notes receivable 5,000 Over But not over The tax shall be Plus Of excess over On Philippine bank deposit, net of FWT 4,800 4,000 250,000 On Phil bank deposit under FCDU On bank deposit abroad 10 0 5,000 On long-term bank deposit 20,000 P 250.000 400.000 0 0 20% P_250.000 400,000 800,000 30.000 25% 400,000 Royalty income: From literary works 10,000 800,000 2,000,000 130,000 30% 800,000 Other than literary works 12,000 2,000,000 8,000,000 490,000 32% 2,000,000 Capital gains: : 8,000,000 12,410,000 35% 8,000,000 On sale of shares of stock of ABC Corp, a closely held corporation directly to a buyer at P 550,000 200,000 On sale of vacation house in Bulacan (Acquisition Cost = 5,500,000; ZV = P 4,000,000, FMV per tax dec: 5,000,000) 500,000 Leslie, a Filipino Citizen residing in Manila, had the following data for the taxable year 2021: Gross income from rent of commercial spaces, net of P 60,000 withholding tax Business expenses 691,000 P 1,140,000 Dividend income From domestic corporation 50,000 1. How much is the total capital gains tax due? From resident foreign corporation 60,000 From non-resident foreign corporation 20,000 Interest income: GRADUATED TAX TABLE UNDER TRAIN LAW (January 1, 2018 to December 31, 2022) On notes receivable 5,000 Over But not over The tax shall be Plus Of excess over On Philippine bank deposit, net of FWT 4,800 On Phil bank deposit under FCDU 4,000 250,000 O 0 On bank deposit abroad 5,000 On long-term bank deposit 20,000 P 250,000 400.000 10 20% P. 250.000 400,000 800,000 30,000 25% 400,000 Royalty income: From literary works 10,000 800,000 2,000,000 130,000 30% 800,000 Other than literary works 12,000 2,000,000 8,000,000 490,000 32% 2,000,000 Capital gains: 8,000,000 2,410,000 35% 8,000,000 On sale of shares of stock of ABC Corp, a closely held corporation directly to a buyer at P 550,000 200,000 500,000 On sale of vacation house in Bulacan (Acquisition Cost = 5,500,000; ZV = P 4,000,000, FMV per tax dec: 5,000,000) Leslie, a Filipino Citizen residing in Manila, had the following data for the taxable year 2021: a Gross income from rent of commercial spaces, net of P 60,000 withholding tax Business expenses 691,000 P 1,140,000 Dividend income From domestic corporation 50,000 1. How much is the total passive income subject to final tax (excluding those subjects to capital gains tax)? From resident foreign corporation 60,000 From non-resident foreign corporation 20,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Visual Auditory And Kinesthetic Self Audit Communication And Learning Profiles

Authors: Brian Everard Walsh, Ronald Willard, Astrid Whiting

1st Edition

098666555X, 978-0986665554