Answered step by step

Verified Expert Solution

Question

1 Approved Answer

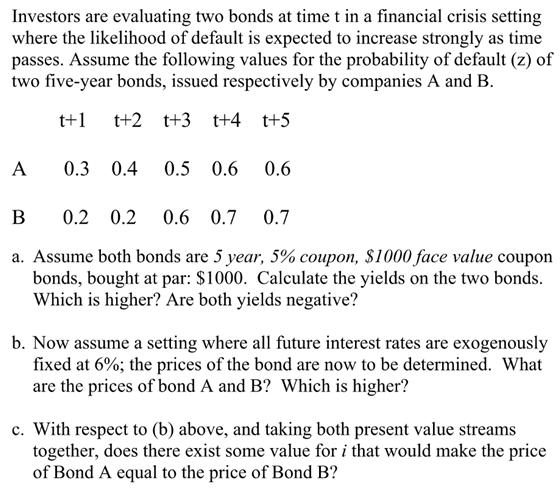

Investors are evaluating two bonds at time t in a financial crisis setting where the likelihood of default is expected to increase strongly as

Investors are evaluating two bonds at time t in a financial crisis setting where the likelihood of default is expected to increase strongly as time passes. Assume the following values for the probability of default (z) of two five-year bonds, issued respectively by companies A and B. t+1 t+2 t+3 t+4 t+5 A 0.3 0.4 0.5 0.6 0.6 0.2 0.2 0.6 0.7 0.7 a. Assume both bonds are 5 year, 5% coupon, $1000 face value coupon bonds, bought at par: $1000. Calculate the yields on the two bonds. Which is higher? Are both yields negative? b. Now assume a setting where all future interest rates are exogenously fixed at 6%; the prices of the bond are now to be determined. What are the prices of bond A and B? Which is higher? c. With respect to (b) above, and taking both present value streams together, does there exist some value for i that would make the price of Bond A equal to the price of Bond B?

Step by Step Solution

★★★★★

3.44 Rating (147 Votes )

There are 3 Steps involved in it

Step: 1

A The Bond Yield is negative after considerig the probability ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Investment Management

Authors: Geoffrey Hirt, Stanley Block

10th edition

0078034620, 978-0078034626