Answered step by step

Verified Expert Solution

Question

1 Approved Answer

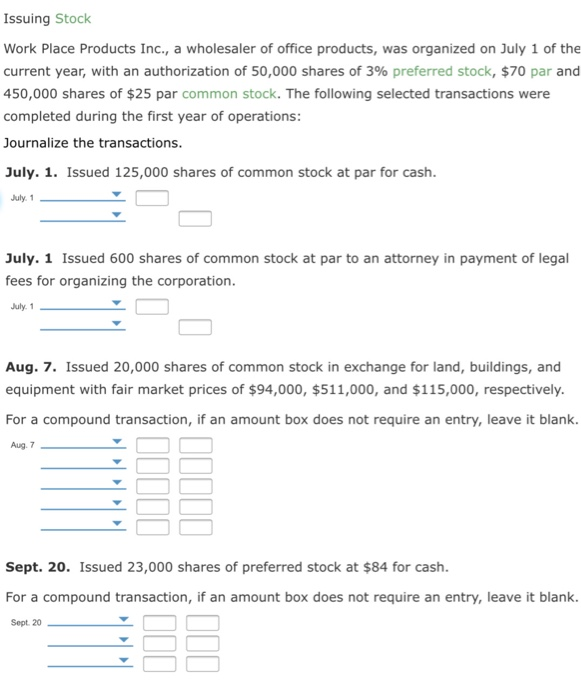

Issuing Stock Work Place Products Inc., a wholesaler of office products, was organized on July 1 of the current year, with an authorization of 50,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Conducting An Institutional Diversity Audit In Higher Education A Practitioners Guide To Systematic Diversity Transformation

Authors: Edna Chun, Alvin Evans, Benjamin D. Reese

1st Edition

1620368196, 978-1620368190